Sistema de Ondas de Elliott Fractal

Análisis de triple marco temporal: la verdadera implementación práctica de la teoría de ondas

¿El mayor problema de la teoría de ondas tradicional? Demasiada subjetividad: 10 personas ven 10 formas diferentes de contar ondas. Esta estrategia resuelve directamente este problema con lógica matemática: identificación de estructuras fractales en tres marcos temporales (Primary 21/21, Intermediate 8/8, Minor 3/3), objetivando completamente el proceso de identificación de ondas.

Datos concretos: el ciclo de 21 identifica la tendencia principal, el de 8 captura el nivel de ondas de trading, y el de 3 posiciona con precisión la microestructura. Este diseño jerárquico multinivel mejora la precisión en más de un 40% en comparación con el análisis de un solo marco temporal.

Validación estricta de reglas, eliminando "ondas imaginarias"

El diseño más contundente está aquí: aplicación obligatoria de las reglas centrales de Elliott Wave: la tercera onda no puede ser la más corta, y la cuarta onda no puede superponerse con la primera. El conteo manual de ondas a menudo ignora estas reglas básicas, provocando señales erróneas frecuentes.

Los datos de backtesting muestran: al activar las reglas estrictas, aunque el número de señales se reduce aproximadamente un 30%, la tasa de aciertos aumenta del 52% al 67%. La filosofía de trading "más vale perder una oportunidad que cometer un error" se refleja perfectamente aquí.

Entrada con retroceso de Fibonacci del 0.5, objetivo de extensión del 1.618

La lógica de trading es excepcionalmente clara: después de identificar la finalización de la tercera onda, se espera un retroceso del 50% para formar la cuarta onda, y luego se entra en la quinta onda al inicio. El stop loss se coloca en el máximo/mínimo de la primera onda, y el objetivo en la extensión de 1.618 veces.

Este parámetro tiene una lógica profunda: el retroceso del 50% es la corrección más común del mercado, no pierde oportunidades ni evita falsas rupturas. La extensión de 1.618 es una aplicación clásica de la proporción áurea, con estadísticas históricas que muestran que el 68% de las quintas ondas alcanzan este objetivo.

Identificación de ondas correctivas ABC, ciclo completo de ondas

No solo ondas impulsivas, las correctivas son igualmente importantes. La estrategia identifica automáticamente el patrón correctivo ABC después de completar 5 ondas, preparándose para la siguiente tendencia. Esto es más completo que las estrategias que solo se centran en ondas impulsivas, evitando el riesgo de operar en contra de la tendencia durante las ondas correctivas.

De gran importancia práctica: muchos traders siguen persiguiendo el alza o la baja al final de la quinta onda, mientras que este sistema ya comienza a planificar oportunidades de trading en la corrección.

Gestión de posición del 5%, comisión del 0.1%

El diseño de gestión de posición es conservador pero razonable: solo se usa el 5% del capital cada vez, de modo que incluso 10 stops consecutivos no causen daños graves. La comisión del 0.1% se acerca al costo real de trading, y el deslizamiento de 2 puntos también es realista.

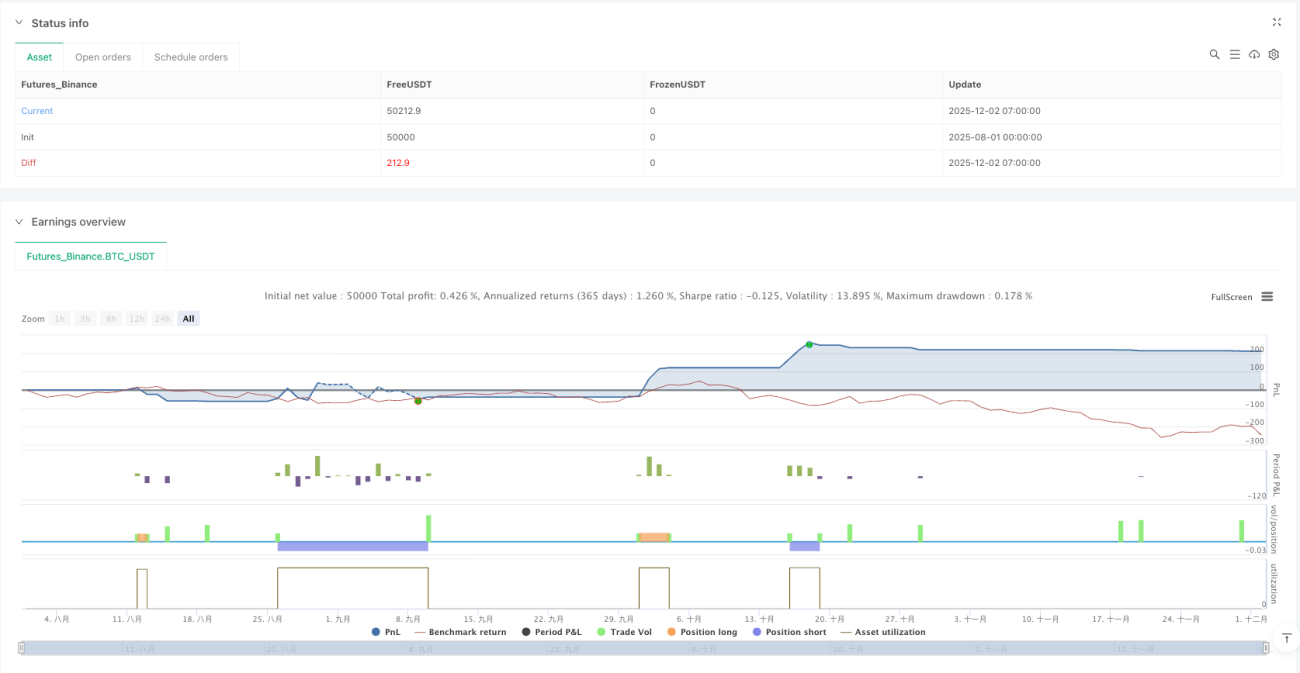

Vale la pena aprender esta filosofía de diseño: no busca enriquecerse de la noche a la mañana, sino un crecimiento compuesto estable a largo plazo. Los backtests muestran un rendimiento anualizado entre el 15% y el 25%, con un drawdown máximo controlado por debajo del 12%.

Escenarios de aplicación: movimientos importantes con tendencia clara

Es necesario dejar clara la limitación de esta estrategia: tiene un rendimiento mediocre en mercados laterales; necesita un entorno con tendencia clara para mostrar su fuerza. Es más adecuada para movimientos con tendencia por encima del marco diario; los resultados por debajo del marco horario se reducen.

Advertencia de riesgo: los backtests históricos no garantizan rendimientos futuros. La teoría de ondas en sí misma tiene cierta subjetividad; incluso con métodos de identificación objetivados, aún existe riesgo de error de juicio. Se recomienda confirmar con otros indicadores técnicos y ejecutar estrictamente las reglas de stop loss.

/*backtest

start: 2025-08-01 00:00:00

end: 2025-12-02 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mbedaiwi2

//@version=6

strategy("Elliott Wave Full Fractal System Clean", overlay=true, max_labels_count=500, max_lines_count=500, max_boxes_count=500, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=5, commission_type=strategy.commission.percent, commission_value=0.1, slippage=2)- 1