Stratégie de trading multi-timeframe basée sur le RSI et les moyennes mobiles

Aperçu

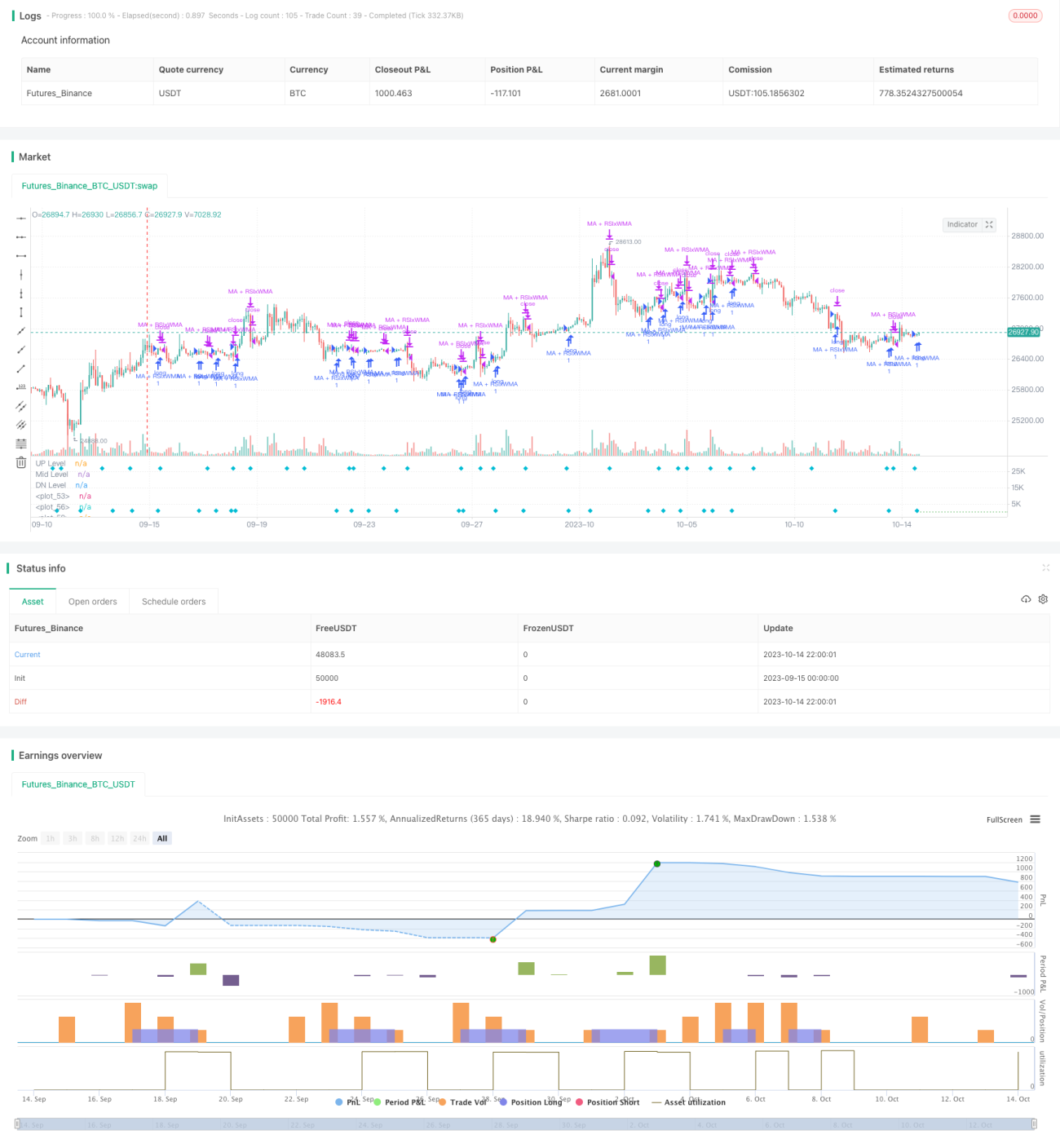

L'idée centrale de cette stratégie est d'utiliser simultanément le Relative Strength Index (RSI) et des moyennes mobiles de différentes périodes pour identifier les points de retournement de tendance, afin de capter les tendances à moyen et long terme tout en réalisant des transactions à court terme. Cette stratégie combine plusieurs signaux de trading dans le but d'améliorer le taux de réussite.

Principe de la stratégie

- Calculer l'indicateur RSI ainsi que la moyenne mobile exponentielle rapide (EMA) et la moyenne mobile linéaire pondérée lente (WMA).

- Lorsque la ligne RSI franchit la moyenne mobile WMA, un signal d'achat/vente est généré.

- Lorsque la moyenne mobile rapide EMA franchit la moyenne mobile lente WMA, un signal d'achat/vente est généré.

- Lorsque le RSI et l'EMA franchissent simultanément la WMA, un signal d'achat/vente fort est produit.

- De plus, lorsque le prix franchit une moyenne mobile auxiliaire, le signal principal peut être renforcé.

- Définir des conditions de stop-loss et de take-profit.

Cette stratégie intègre les signaux de franchissement de plusieurs indicateurs techniques et utilise des moyennes mobiles configurées avec différents paramètres pour identifier les tendances de cycles variés, augmentant ainsi sa fiabilité. Le RSI évalue les conditions de surachat/survente, l'EMA rapide identifie la tendance à court terme, la WMA lente la tendance à moyen terme, tandis que le franchissement du prix par rapport à la moyenne auxiliaire confirme la tendance. La combinaison de multiples signaux améliore l'efficacité de la stratégie.

Analyse des avantages

- L'utilisation des caractéristiques de retournement du RSI permet de saisir les opportunités de retournement dans les zones de surachat/survente.

- La moyenne mobile auxiliaire sert de filtre de tendance pour éviter les faux franchissements.

- La combinaison de plusieurs périodes temporelles permet à la fois de suivre les tendances à long terme et de capter les opportunités à court terme.

- La combinaison de plusieurs signaux d'indicateurs peut améliorer le taux de réussite des transactions.

- La mise en place de stratégies de stop-loss et de take-profit permet un contrôle actif des risques.

Analyse des risques

- L'indicateur RSI est sujet aux faux signaux, nécessitant le filtrage par une moyenne mobile auxiliaire.

- Les rebonds dans une tendance à long terme peuvent déclencher des signaux de trading contraires, nécessitant une prudence.

- Il est nécessaire d'optimiser les paramètres, tels que la période du RSI et les périodes des moyennes mobiles.

- Les niveaux de stop-loss doivent être définis avec soin pour éviter d'être piégé.

Les risques peuvent être atténués par l'optimisation des paramètres, une stricte gestion des stop-loss et la prise en compte de la tendance à long terme.

Axes d'optimisation

- Optimiser les paramètres du RSI pour trouver la période optimale.

- Tester différentes combinaisons de types de moyennes mobiles.

- Ajouter un indicateur de volatilité tel que l'ATR pour ajuster dynamiquement les niveaux de stop-loss et de take-profit.

- Ajouter un module de gestion de la taille des positions.

- Utiliser des techniques d'apprentissage automatique pour l'optimisation des paramètres et l'évaluation de la qualité des signaux.

Résumé

Cette stratégie intègre les approches de suivi de tendance et de trading de retournement aux extrêmes, en ajoutant une analyse multi-temporelle et l'utilisation combinée de plusieurs indicateurs, dans le but d'augmenter le taux de réussite des transactions. L'essentiel est de bien contrôler les risques, d'optimiser les paramètres et de prendre en compte l'impact de la tendance à long terme sur les transactions. Dans l'ensemble, cette stratégie offre une bonne praticabilité et adaptabilité. Par la suite, des techniques plus avancées pourront être utilisées pour améliorer encore la qualité de la stratégie.

- 1