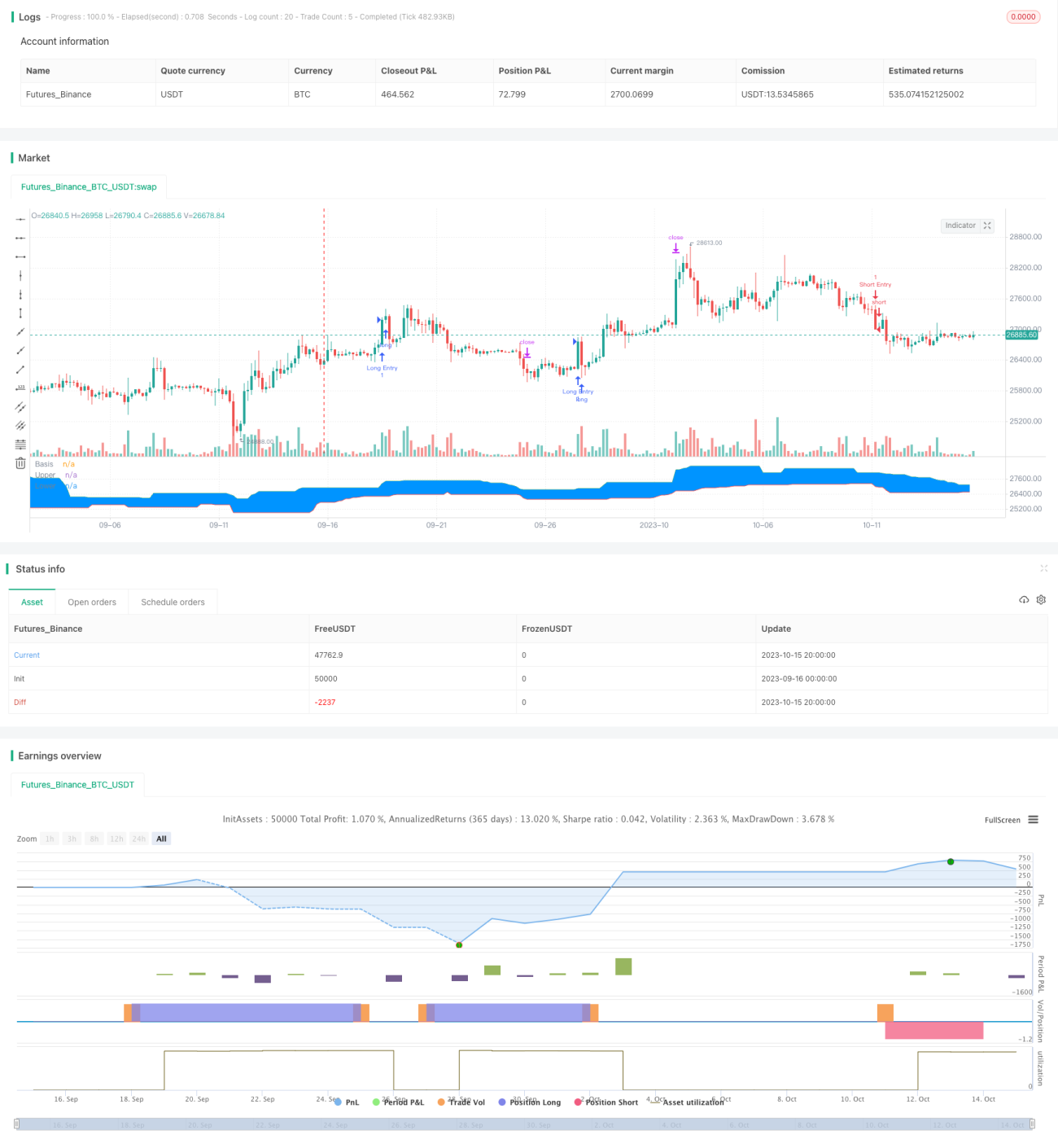

Stratégie de breakout de suivi

Aperçu

Cette stratégie met principalement en œuvre une stratégie de trading de rupture avec suivi via l'indicateur "Canal de Donchian". Elle combine les approches de tendance et de rupture, et sur la base d'un jugement de tendance à long terme, recherche des points de rupture sur des périodes plus courtes pour effectuer des entrées, réalisant ainsi un trading dans le sens de la tendance. En outre, la stratégie fixe des niveaux de stop-loss et de take-profit pour contrôler le ratio risque/rendement de chaque opération. Dans l'ensemble, cette stratégie présente l'avantage de suivre la tendance, permettant de naviguer avec le courant et de saisir les opportunités de tendance à long terme.

Principe de la stratégie

- Paramétrer l'indicateur "Canal de Donchian", avec une période par défaut de 20.

- Paramétrer une moyenne mobile exponentielle (EMA) lissée, avec une période par défaut de 200.

- Paramétrer le ratio risque/rendement, avec une valeur par défaut de 1,5.

- Paramétrer le retracement de rupture, respectivement pour les positions longues et courtes.

- Enregistrer si la dernière rupture était un plus haut ou un plus bas.

- Signal long : si la dernière rupture était un plus bas, que le prix est supérieur à la bande supérieure de Donchian et supérieur à la moyenne EMA, alors générer un signal long.

- Signal court : si la dernière rupture était un plus haut, que le prix est inférieur à la bande inférieure de Donchian et inférieur à la moyenne EMA, alors générer un signal court.

- Après être entré en position longue, placer un stop-loss à la bande inférieure de Donchian avec un retrait de 5 points, et un take-profit égal au ratio risque/rendement multiplié par la distance du stop-loss.

- Après être entré en position courte, placer un stop-loss à la bande supérieure de Donchian avec un retrait de 5 points, et un take-profit égal au ratio risque/rendement multiplié par la distance du stop-loss.

De cette manière, la stratégie combine le jugement de tendance et les opérations de rupture, ce qui permet de suivre la tendance et de saisir les opportunités sur des périodes plus courtes dans le cadre d'une tendance à long terme. En même temps, le réglage du stop-loss et du take-profit permet de contrôler le rapport risque/rendement de chaque transaction.

Analyse des avantages

- Suit la tendance à long terme, agit dans le sens de la tendance, évite les transactions à contre-tendance.

- Le canal de Donchian, en tant qu'indicateur de long terme, combiné au filtre de la moyenne EMA, permet de bien juger la direction de la tendance.

- Le mécanisme de stop-loss et de take-profit contrôle le risque de chaque opération, limitant les pertes potentielles.

- L'optimisation du ratio risque/rendement permet d'augmenter le rapport gain/perte, visant des rendements excédentaires.

- Les paramètres de backtest sont flexibles, permettant d'ajuster la meilleure combinaison de paramètres pour différents marchés.

Analyse des risques

- Le canal de Donchian et la moyenne EMA utilisés comme filtres peuvent générer des signaux erronés.

- Les transactions de rupture risquent d'être piégées ; il est nécessaire d'identifier clairement le contexte de tendance.

- Les distances de stop-loss et de take-profit sont fixes, ne pouvant être ajustées en fonction de la volatilité du marché.

- L'espace d'optimisation des paramètres est limité, ce qui rend difficile la garantie des performances en trading réel.

- Le système de trading ne résiste pas à trop d'événements aléatoires ; un événement cygne noir peut entraîner des pertes importantes.

Axes d'optimisation

- On peut envisager d'ajouter davantage d'indicateurs pour filtrer, par exemple des oscillateurs, afin d'améliorer la qualité des signaux.

- On peut mettre en place un stop-loss et un take-profit intelligents, ajustant dynamiquement les niveaux de profit et de perte en fonction de la volatilité du marché et de l'indicateur ATR.

- On peut utiliser des méthodes comme l'apprentissage automatique pour tester et optimiser les paramètres, afin de les rendre plus proches du marché réel.

- On peut optimiser la logique d'entrée en ajoutant des indicateurs de volume ou de volatilité comme conditions auxiliaires, pour éviter les pièges.

- On peut envisager de combiner avec des stratégies de suivi de tendance ou d'apprentissage automatique pour former une stratégie hybride, améliorant ainsi la stabilité.

Conclusion

Cette stratégie, en tant que stratégie de rupture avec suivi, repose sur l'idée centrale de, après avoir identifié une tendance à long terme, effectuer des opérations dans le sens de la tendance en utilisant la rupture comme signal, et de fixer un stop-loss et un take-profit pour contrôler le risque de chaque transaction. Cette stratégie présente certains avantages, mais aussi des axes d'amélioration potentiels. Dans l'ensemble, si l'on parvient à bien gérer les réglages des paramètres, le timing d'entrée et d'autres questions, et à la renforcer avec d'autres techniques, cette stratégie peut devenir une stratégie de suivi de tendance pratique. Cependant, les investisseurs doivent garder à l'esprit qu'aucun système de trading ne peut totalement éviter les risques de marché, et qu'une gestion des risques appropriée est nécessaire.

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1