Stratégie d'absorption sur baisse en forme de correction

Aperçu

Cette stratégie combine l'indicateur RSI et une moyenne mobile des prix pour détecter des opportunités de surachat lorsque le cours de l'action passe sous la moyenne mobile, puis ouvrir une position longue. À mesure que le prix baisse davantage, la stratégie ajoute progressivement des positions par paliers prédéfinis, dans le but de lisser le coût moyen de détention. Lorsque le profit de la position atteint le pourcentage de take profit configuré, la stratégie choisit de clôturer la position. Par ailleurs, la stratégie introduit un mécanisme de take profit progressif : en fonction des profits déjà réalisés sur chaque lot, elle ajuste dynamiquement le prix de take profit de l'ensemble de la position. Cela permet de réduire efficacement le risque de perte et de sortir progressivement.

Principe de la stratégie

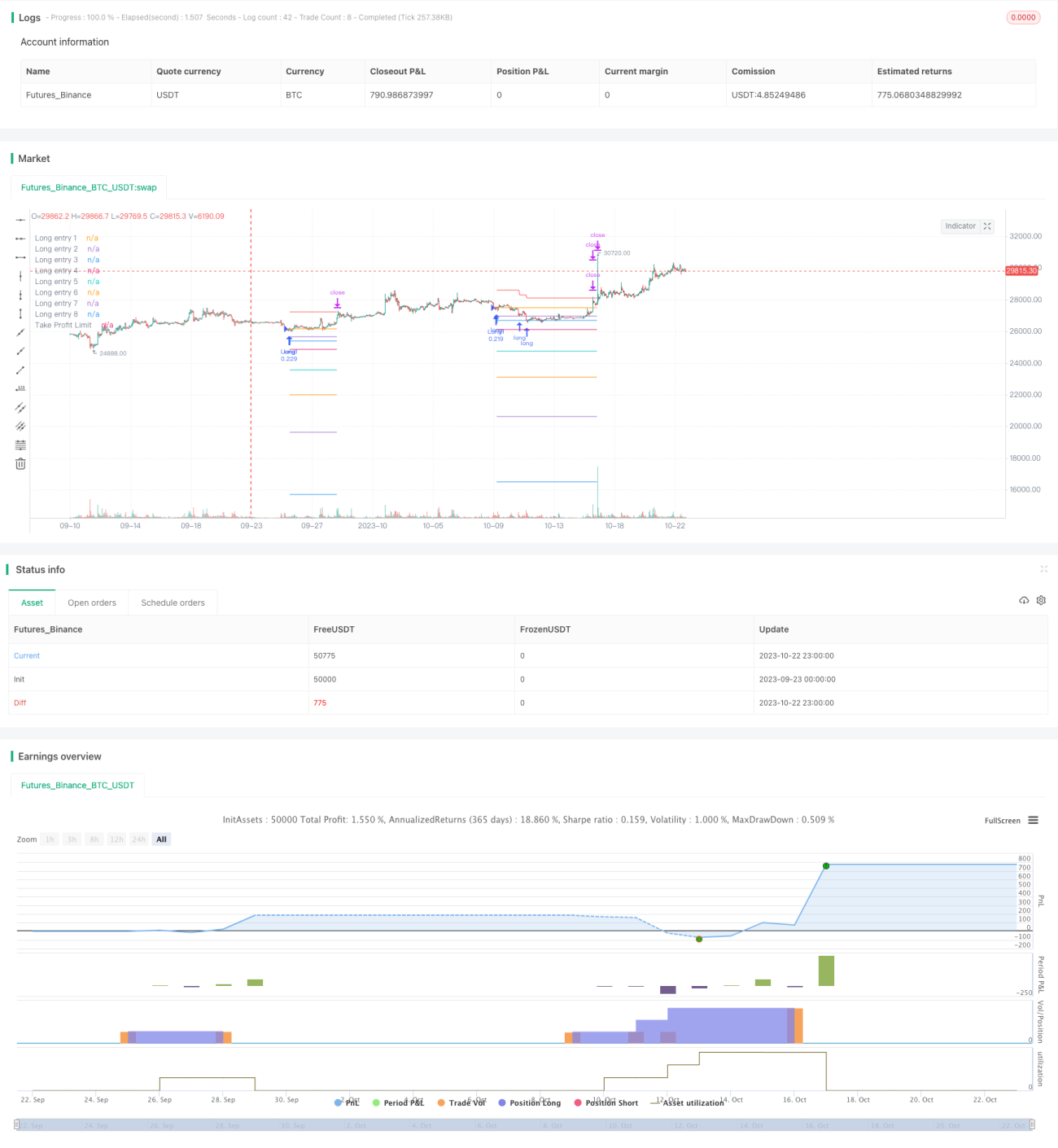

- Lorsque l'indicateur RSI est inférieur au seuil de surachat de 29 et que le cours de clôture est inférieur à la moyenne mobile, la stratégie ouvre la première position longue.

- Lorsque le cours baisse de 2 % par rapport à la première position, la stratégie ajoute une position ; lorsqu'il baisse de 3 %, elle ajoute une troisième position, et ainsi de suite jusqu'à un maximum de 8 ajouts. Cela permet un effet d'achat par tranches.

- Chaque ouverture de position enregistre le prix d'ouverture correspondant. Ces prix servent de références d'entrée et sont tracés sous forme de lignes sur le graphique.

- Après l'ouverture, le prix moyen de la position est calculé. Un take profit de 3 % de ce prix moyen est défini pour chaque lot, et de 4 % pour l'ensemble de la position.

- Lorsque le prix dépasse le take profit d'un lot, ce lot est clôturé.

- Calcul du take profit progressif : à chaque clôture d'un lot, le profit réalisé sur ce lot est déduit du prix de take profit global. Cela fait descendre lentement la ligne de take profit – tous les lots ne sont clôturés que lorsque le total des profits réalisés compense la perte maximale possible.

- Lorsque le prix atteint la ligne de take profit progressif, l'ensemble de la position est clôturé.

Analyse des avantages

- L'indicateur RSI permet d'identifier assez précisément les zones de surachat, favorisant la détection des retournements.

- L'ajout progressif par tranches permet de lisser le coût d'entrée à des niveaux bas.

- Le take profit progressif réduit le risque de perte et permet une sortie graduée. Même en cas de perte, celle-ci reste limitée.

- Les ratios de take profit et d'ajout de positions sont configurables, ce qui permet d'adapter la stratégie au marché.

- Le tracé des lignes de référence d'ouverture et de take profit sur le graphique offre une visualisation claire de la répartition des positions.

Analyse des risques

- Dans un marché rangeant, la stratégie peut déclencher de nombreuses ouvertures et clôtures, entraînant des pertes dues au slippage. Il est possible d'assouplir les paramètres du RSI pour réduire le nombre de transactions.

- Un mauvais réglage du nombre d'ajouts et des ratios peut conduire à un sur-échange ; il convient de les paramétrer prudemment en fonction du capital.

- Si le marché continue de baisser après les ajouts, un risque de perte « sans fond » existe. Il faut fixer une limite maximale d'ajouts et un ratio conservateur pour le dernier palier.

- Si le ratio de take profit est trop faible, la stratégie peut sortir trop tôt. Il est recommandé de déterminer un ratio approprié à partir de backtests historiques.

Pistes d'optimisation

- On peut introduire des indicateurs comme le MACD pour filtrer les signaux du RSI et réduire les transactions non pertinentes.

- Un stop loss basé sur l'ATR peut être ajouté pour éviter des pertes massives lors de mouvements extrêmes.

- On peut optimiser le nombre d'ajouts, les ratios et le take profit pour les adapter à différents actifs.

- On peut ajuster dynamiquement le take profit en fonction de la volatilité, en l'assouplissant lorsque la volatilité est élevée.

Conclusion

Cette stratégie exploite pleinement l'indicateur RSI pour identifier les zones de surachat, combiné à une moyenne mobile pour effectuer des transactions de retournement. Grâce à un mécanisme d'ajout intelligent et de take profit progressif, elle parvient à une stratégie longue efficace tout en maîtrisant le risque. En optimisant les paramètres des indicateurs et le mécanisme de take profit, la stratégie peut devenir plus stable et plus efficace. Elle peut être largement appliquée aux contrats à terme sur indices, aux cryptomonnaies et à d'autres instruments financiers présentant des caractéristiques de retournement de tendance, ce qui lui confère une réelle valeur d'investissement.

- 1