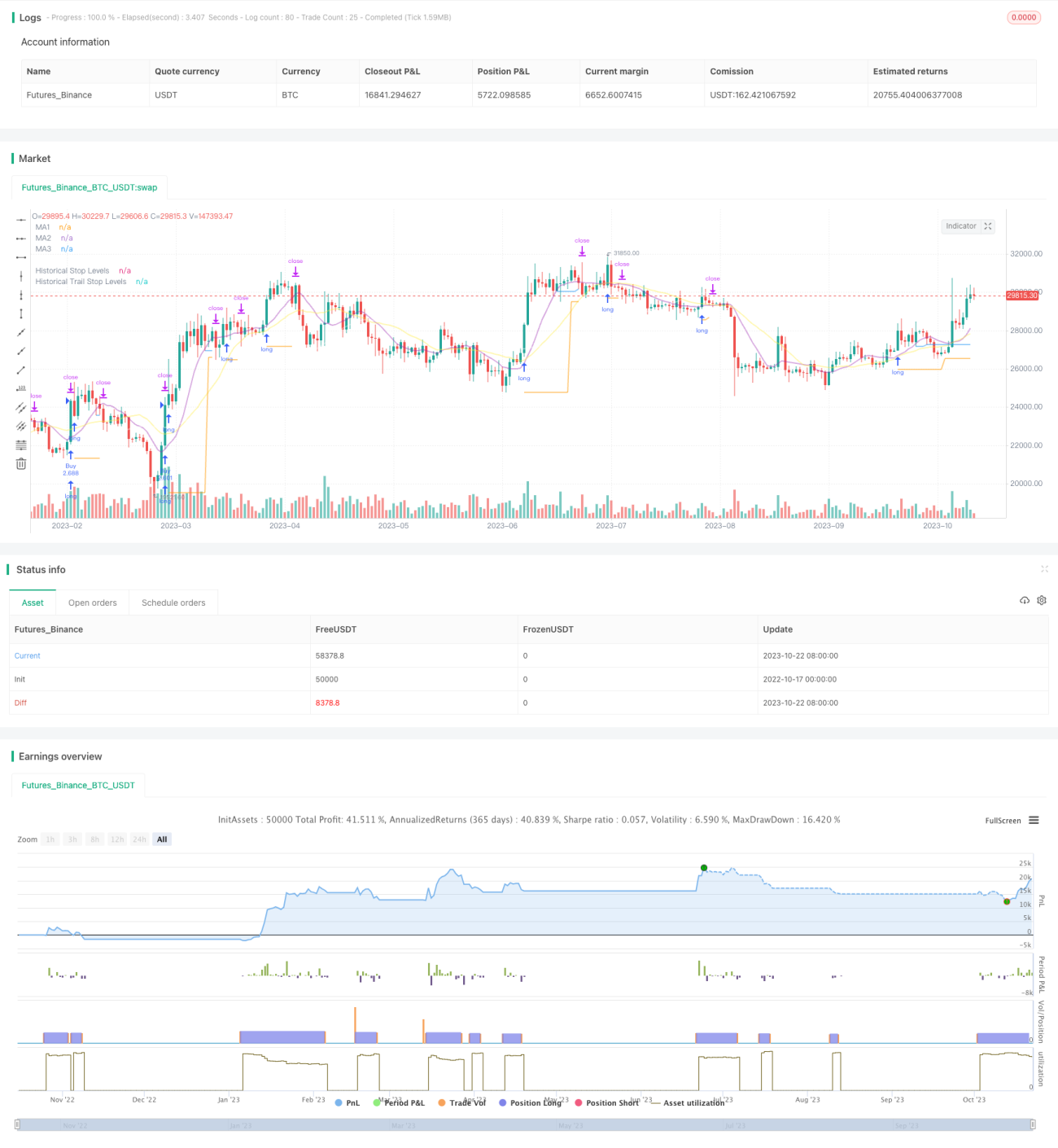

Stratégie de Breakout avec Trailing Stop V2

Aperçu

Cette stratégie combine les avantages d'une stratégie de cassure et d'une stratégie de suivi de tendance avec stop suiveur, visant à capturer les signaux de cassure des supports et résistances sur des horizons longs, tout en utilisant des moyennes mobiles pour un stop suiveur, afin de réaliser des profits dans le sens de la tendance de long terme tout en contrôlant les risques.

Principe de la stratégie

-

La stratégie calcule d'abord plusieurs groupes de moyennes mobiles avec différents paramètres, utilisées respectivement pour le jugement de tendance, les supports/résistances et le stop suiveur.

-

Ensuite, elle identifie les plus hauts et les plus bas sur une période donnée pour former les zones de support et résistance d'entrée. Lorsque le prix franchit ces niveaux, un signal est généré.

-

La stratégie prend une position longue lorsque le prix dépasse le plus haut, et une position courte lorsqu'il casse le plus bas.

-

Après l'entrée, la position est maintenue avec un stop loss fixé au niveau du plus bas cassé (pour les longs) ou du plus haut cassé (pour les shorts).

-

Lorsque la position devient bénéficiaire, le stop loss est converti en un stop suiveur basé sur une moyenne mobile. Lorsque le prix casse la moyenne mobile, le stop est placé au plus bas de la bougie.

-

Cela permet de verrouiller les profits tout en laissant suffisamment d'espace à la position pour suivre la tendance.

-

La stratégie intègre également l'Average True Range (ATR) pour s'assurer que l'entrée en cassure se fait dans une fourchette appropriée, évitant les cassures excessives.

Analyse des avantages de la stratégie

-

Combine les avantages d'une stratégie de cassure et d'une stratégie de stop suiveur de tendance.

-

Permet d'acheter les cassures dans le sens de la tendance de long terme, augmentant la probabilité de profit.

-

La stratégie de stop loss protège la position tout en lui donnant suffisamment d'espace pour évoluer.

-

Ajoute un filtre de volatilité pour éviter les cassures défavorables et excessives.

-

Automatisée, adaptée au suivi partiel des transactions.

-

Permet de personnaliser les moyennes mobiles sur différentes périodes.

-

Possibilité d'ajuster flexiblement la méthode de stop suiveur.

Analyse des risques de la stratégie

-

Les stratégies de cassure sont sujettes aux faux signaux. Il est possible d'assouplir la confirmation de cassure.

-

Un mouvement suffisant est nécessaire pour générer un signal de cassure ; la stratégie peut être inefficace dans des marchés agités.

-

Certaines cassures peuvent être trop brèves pour être capturées. On peut réduire l'échelle de temps pour trouver plus d'opportunités.

-

Le stop suiveur peut entraîner des arrêts trop fréquents dans un marché en range. On peut élargir la distance du stop.

-

Le filtre de volatilité peut faire manquer certaines opportunités. On peut réduire le paramètre de filtre.

Pistes d'optimisation de la stratégie

-

Tester différentes combinaisons de paramètres de moyennes mobiles pour trouver les meilleurs paramètres.

-

Tester différents mécanismes de confirmation de cassure, comme les canaux, les configurations de bougies, etc.

-

Essayer différentes méthodes de stop suiveur pour trouver le meilleur stop.

-

Optimiser la gestion du capital, comme le position scoring.

-

Ajouter des indicateurs techniques statistiques pour améliorer la précision du filtrage.

-

Tester l'efficacité de la stratégie sur différents instruments.

-

Intégrer des algorithmes d'apprentissage automatique pour améliorer les performances.

Conclusion

Cette stratégie combine les idées de cassure et de stop suiveur de tendance. Si l'orientation de long terme est correcte, elle permet d'optimiser l'espace de profit. La clé est de trouver la meilleure combinaison de paramètres et de l'accompagner d'une bonne gestion du capital pour saisir les opportunités de long terme tout en maîtrisant les risques. Cette stratégie a le potentiel de devenir une stratégie de tendance de long terme fiable après optimisation supplémentaire.

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1