Stratégie de tendance à court terme basée sur des indicateurs multidimensionnels pour la décision

Aperçu

Cette stratégie combine trois indicateurs techniques de dimensions différentes – les niveaux de support et résistance, le système de moyennes mobiles et un indicateur de surachat/survente – pour déterminer la direction des tendances à court terme en fonction de leurs signaux synthétiques, afin d'obtenir un taux de réussite élevé.

Principe de la stratégie

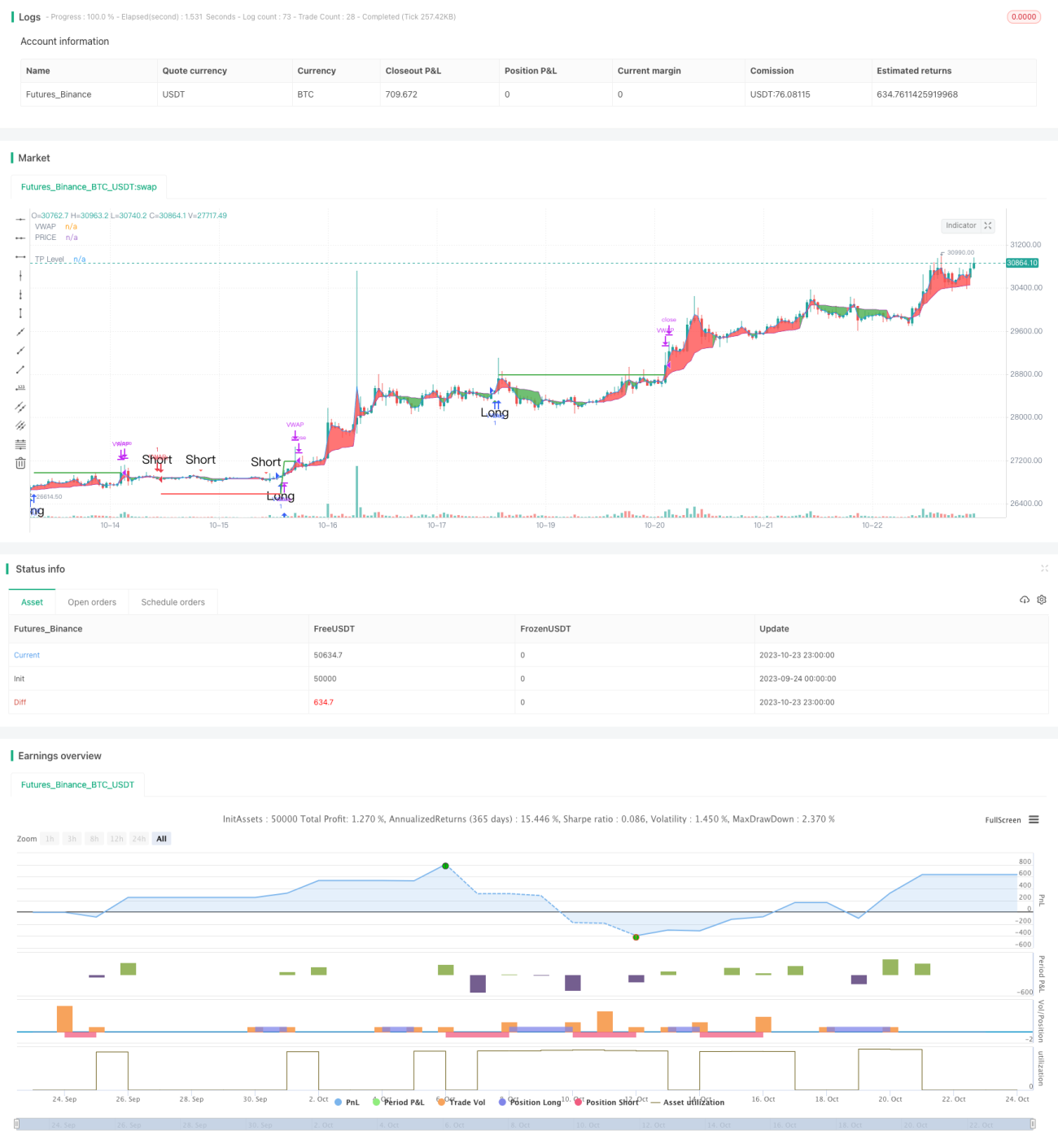

Le code calcule d'abord les niveaux de support et résistance du prix, y compris l'axe d'oscillation standard et les niveaux de support/résistance de Fibonacci, et les trace sur le graphique. Lorsque le prix franchit ces niveaux clés, cela est considéré comme un signal de tendance important.

Ensuite, on calcule la moyenne mobile pondérée en volume (VWAP) et la moyenne des prix, et on détecte leurs signaux de croisement doré (golden cross) et croisement mortel (death cross). Cela relève du jugement de tendance à moyen/long terme.

Enfin, on calcule l'indicateur Stochastic RSI et on détecte ses signaux de croisement doré et mortel, ce qui est un indicateur de surachat/survente.

En combinant ces trois dimensions, si les niveaux de support/résistance, le VWAP et le Stochastic RSI émettent simultanément un signal d'achat, on ouvre une position longue ; si les trois émettent simultanément un signal de vente, on ouvre une position courte.

Analyse des avantages

Le principal atout de cette stratégie est qu'elle combine trois indicateurs de dimensions différentes, rendant le jugement plus complet et précis, avec un taux de réussite élevé. Premièrement, les niveaux de support/résistance jugent la tendance générale ; deuxièmement, le VWAP juge la tendance à moyen/long terme ; enfin, le Stochastic RSI juge les conditions de surachat/survente. Lorsque les trois dimensions envoient des signaux simultanément, cela permet de filtrer considérablement les faux signaux et d'augmenter le taux de réussite des entrées.

De plus, la stratégie intègre une fonction de prise de bénéfices, permettant de verrouiller une partie des gains, ce qui est bénéfique pour la gestion du capital.

Analyse des risques

Le principal risque de cette stratégie réside dans le fait que les décisions long/short dépendent de la synchronisation des signaux entre les indicateurs. Si certains indicateurs émettent des signaux erronés, cela peut conduire à une décision incorrecte. Par exemple, si le Stochastic RSI émet un signal de surachat alors que le VWAP et les supports/résistances restent haussiers, on peut manquer un point d'achat et ne pas entrer en position.

De plus, un paramétrage inapproprié des indicateurs peut également entraîner des signaux erronés, d'où la nécessité de trouver les paramètres optimaux par des backtests répétés.

Par ailleurs, les marchés boursiers connaissent souvent des événements cygnes noirs à court terme, pouvant entraîner l'inefficacité des indicateurs. Pour se prémunir contre ce risque, on peut ajouter une stratégie de stop-loss afin d'éviter des pertes unitaires trop importantes.

Pistes d'optimisation

La stratégie peut être optimisée dans les directions suivantes :

- Ajouter davantage de signaux d'indicateurs, comme les indicateurs de volume, pour juger la force de la tendance et améliorer la précision des décisions.

- Intégrer un modèle d'apprentissage automatique pour entraîner les indicateurs multidimensionnels et trouver automatiquement la stratégie de trading optimale.

- Optimiser les paramètres en fonction des différents instruments, en mettant en place des paramètres adaptatifs.

- Ajouter une stratégie de stop-loss et contrôler la taille des positions en fonction du drawdown, pour mieux maîtriser le risque.

- Réaliser une optimisation de portefeuille en trouvant des instruments faiblement corrélés à combiner, afin de réduire le drawdown global.

Conclusion

Globalement, cette stratégie est très adaptée au trading de tendance à court terme. Elle utilise des indicateurs multidimensionnels pour prendre des décisions, ce qui permet de filtrer une grande partie du bruit et d'obtenir un taux de réussite élevé. Il faut néanmoins rester vigilant face au risque de signaux erronés ; avec une optimisation continue, cette stratégie a le potentiel de devenir une stratégie de court terme efficace et stable.

- 1