Stratégie d'oscillation de bande basée sur le nombre d'or

Aperçu

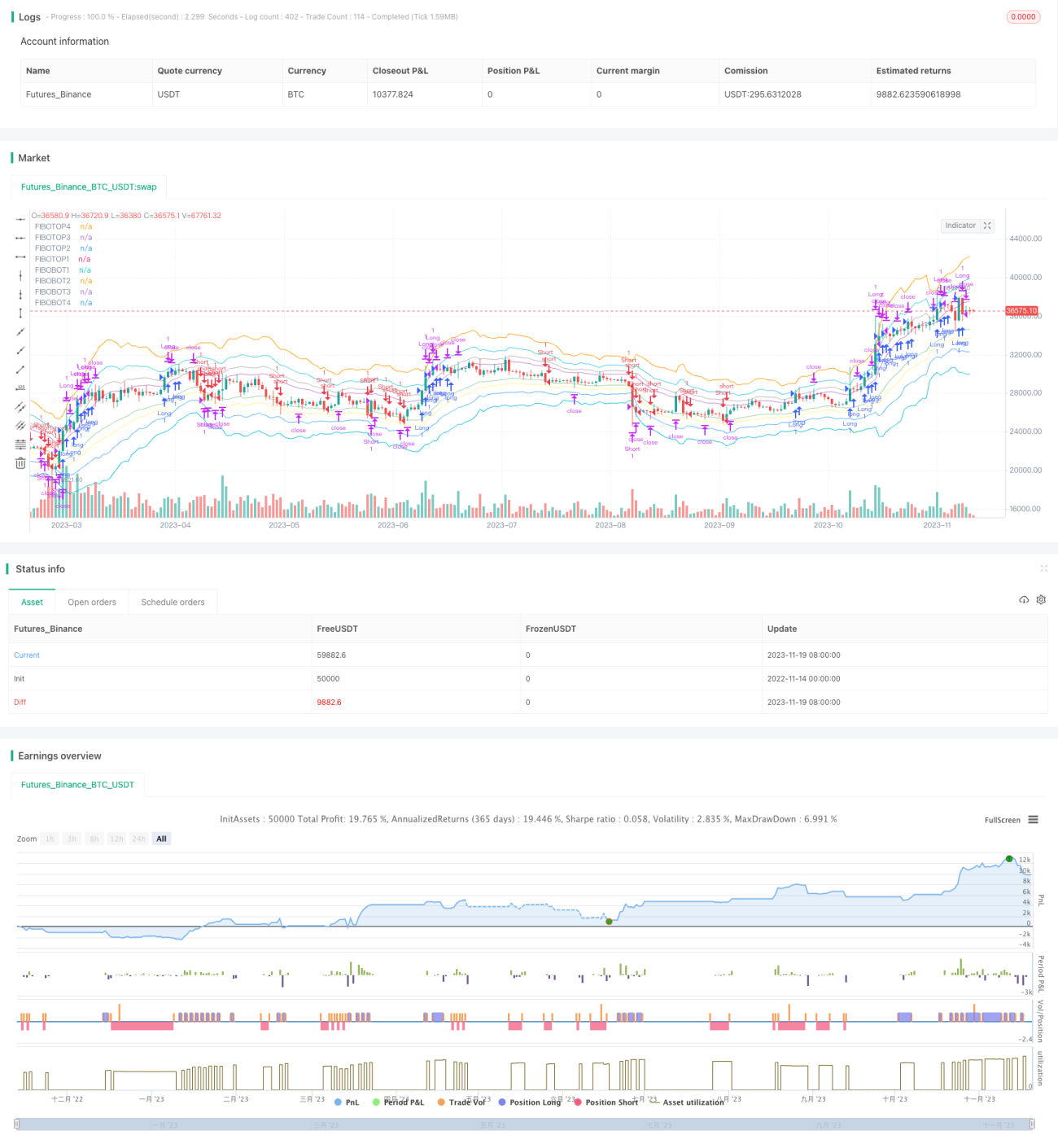

La stratégie de range oscillatoire basée sur les retracements de Fibonacci est une stratégie quantitative conçue autour de la théorie des retracements de Fibonacci. Elle utilise principalement les ratios de Fibonacci pour calculer plusieurs bandes de prix, formant des ranges hauts et bas. Lorsque le prix franchit une bande, un signal de trading est généré, permettant de profiter des oscillations du prix entre ces bandes.

Principe de la stratégie

Le cœur du code repose sur le calcul des bandes de retracement de Fibonacci en tant que points clés. Les principales étapes sont :

- Calculer la moyenne mobile exponentielle (EMA) sur 14 périodes comme axe central.

- Calculer 4 bandes supérieures et inférieures à partir de l'ATR et des ratios de Fibonacci.

- Lorsque le prix franchit une bande baissière à la hausse ou une bande haussière à la baisse, un signal de trading est généré.

- Définir un stop loss et un take profit pour capturer les gains lors des oscillations de prix.

Cette approche de franchissement de points clés permet de capturer efficacement les oscillations à court terme du marché et de trader entre les bandes pour réaliser des profits.

Avantages de la stratégie

Le principal avantage de cette stratégie est l'utilisation des retracements de Fibonacci, un indicateur théorique important, pour localiser les points de prix clés, augmentant ainsi la probabilité de gains. Les avantages spécifiques incluent :

- Les bandes de Fibonacci sont claires, facilitant l'identification des points de rupture.

- Les fourchettes de bandes sont appropriées, ni trop serrées ni trop larges.

- Plusieurs bandes sont disponibles, permettant à la fois des transactions agressives et conservatrices.

- Les oscillations entre bandes sont marquées, ce qui rend la stratégie efficace pour le trading à court terme.

Risques de la stratégie

Étant donné que cette stratégie vise des profits à court terme, certains risques doivent être pris en compte :

- Incapacité à générer des profits dans une tendance à long terme.

- Risque de stop loss plus élevé en cas de volatilité extrême des prix.

- De nombreux signaux de franchissement, nécessitant une sélection prudente.

- Inefficacité lorsque les oscillations entre bandes disparaissent.

Ces risques peuvent être maîtrisés en ajustant correctement les paramètres, en sélectionnant les bandes appropriées et en adoptant une gestion de capital adaptée.

Optimisation de la stratégie

Cette stratégie offre encore des possibilités d'optimisation :

- Intégrer des indicateurs de tendance pour filtrer les signaux en fonction de la direction de la tendance.

- Désactiver la stratégie avant et après des événements importants ou à des périodes spécifiques.

- Ajuster dynamiquement la largeur du stop loss pour s'adapter à la fréquence des fluctuations du marché.

- Optimiser les paramètres en choisissant différentes périodes d'EMA comme ligne de base centrale.

Résumé

La stratégie de range oscillatoire basée sur les retracements de Fibonacci est globalement une stratégie de trading à court terme très pratique. Elle utilise la théorie de Fibonacci pour définir des points de prix clés, et lorsque le prix oscille autour de ces points, elle peut générer des profits substantiels. Cette méthode de franchissement de ranges convient aux marchés présentant une certaine volatilité et des caractéristiques claires. Elle peut être utilisée seule ou combinée à d'autres stratégies. Grâce à l'optimisation des paramètres et à une gestion de capital appropriée, cette stratégie peut fonctionner de manière stable à long terme.

- 1