Stratégie de suivi de tendance avec double EMA et indicateur Williams

Aperçu

Cette stratégie combine deux indicateurs EMA et l'indicateur Williams pour identifier la direction de la tendance, en suivant celle-ci lorsqu'elle est suffisamment forte. Son principe de base est le suivant :

- Utiliser une combinaison de deux EMA pour filtrer les tendances les plus robustes.

- L'indicateur Williams confirme que le marché se trouve en zone de surachat ou de survente.

- Associer l'indicateur RSI pour éviter d'acheter au sommet ou de vendre au creux.

Principe

La stratégie utilise les EMA court terme et long terme parmi les deux EMA. Lorsque l'EMA court terme croise l'EMA long terme à la hausse, un signal d'achat est généré ; à l'inverse, lorsque l'EMA court terme croise l'EMA long terme à la baisse, un signal de vente est émis. Les deux EMA permettent de capter la tendance à moyen et long terme.

De plus, la stratégie intègre l'indicateur Williams pour identifier les retournements. L'indicateur Williams détermine si le prix est en situation de surachat ou de survente en repérant les plus hauts et plus bas de la période. Quand Williams indique un surachat, un signal de vente est généré ; quand il indique une survente, un signal d'achat apparaît.

La logique spécifique dans le code est la suivante :

Entrée long : l'EMA court terme croise à la hausse les EMA moyen terme et long terme, l'indicateur Williams montre une zone de survente, et un plus bas se forme dans cette zone de survente, ce qui signale une opportunité de retournement, générant un signal d'achat.

Entrée short : l'EMA court terme croise à la baisse les EMA moyen terme et long terme, l'indicateur Williams montre une zone de surachat, et un plus haut se forme dans cette zone de surachat, ce qui signale une opportunité de retournement, générant un signal de vente.

En outre, l'indicateur RSI est introduit pour confirmer davantage les signaux de trading et éviter de courir après les hausses ou les baisses aveuglément.

Avantages

Le principal avantage de cette stratégie est d'utiliser les deux EMA pour filtrer un grand nombre de tendances inefficaces, en ne sélectionnant que les tendances les plus fortes à moyen et long terme, permettant ainsi de réduire le bruit et d'éviter les transactions inutiles.

L'introduction de l'indicateur Williams est également très bénéfique. D'une part, elle permet d'identifier les opportunités de retournement et donc de clôturer les positions à temps ; d'autre part, elle confirme la validité des signaux de tendance.

La combinaison des deux EMA et de Williams permet à la stratégie d'obtenir un bon suivi des profits sur les actifs à moyen et long terme, tout en identifiant les retournements et en limitant les pertes.

Risques

Le principal risque de cette stratégie réside dans la difficulté à repérer les points de retournement de tendance. Bien que l'indicateur Williams et le RSI soient utilisés pour assurer l'efficacité des transactions de retournement, ces dernières restent complexes et ne permettent pas d'éliminer complètement le risque d'acheter au sommet ou de vendre au creux.

De plus, la combinaison des deux EMA présente elle-même un certain décalage. Lorsque la tendance à court terme se dissocie des tendances à moyen et long terme, la stratégie peut rencontrer des difficultés d'identification.

Optimisation

La stratégie peut être optimisée selon les axes suivants :

- Tester davantage de combinaisons de périodes EMA pour trouver les meilleurs paramètres.

- Ajouter un mécanisme de sortie adaptatif, en utilisant des indicateurs comme l'ATR ou l'indice de volatilité pour détecter les retournements de tendance.

- Intégrer des éléments de machine learning, par exemple avec LSTM, pour la prédiction des tendances et des retournements.

- Améliorer les règles de trading de retournement à l'aide de méthodes comme la théorie des vagues.

- Introduire une gestion de position adaptative, en ajustant la taille des positions en fonction des conditions de marché.

Résumé

Cette stratégie combine avec succès les deux EMA et l'indicateur Williams pour capter les tendances à moyen et long terme, permettant d'obtenir des rendements plus élevés dans les grandes tendances. Parallèlement, l'introduction de Williams permet à la stratégie d'identifier les retournements et de limiter les pertes en temps voulu. La prochaine étape consistera à optimiser la stabilité de la stratégie en y ajoutant davantage d'indicateurs et de modèles.

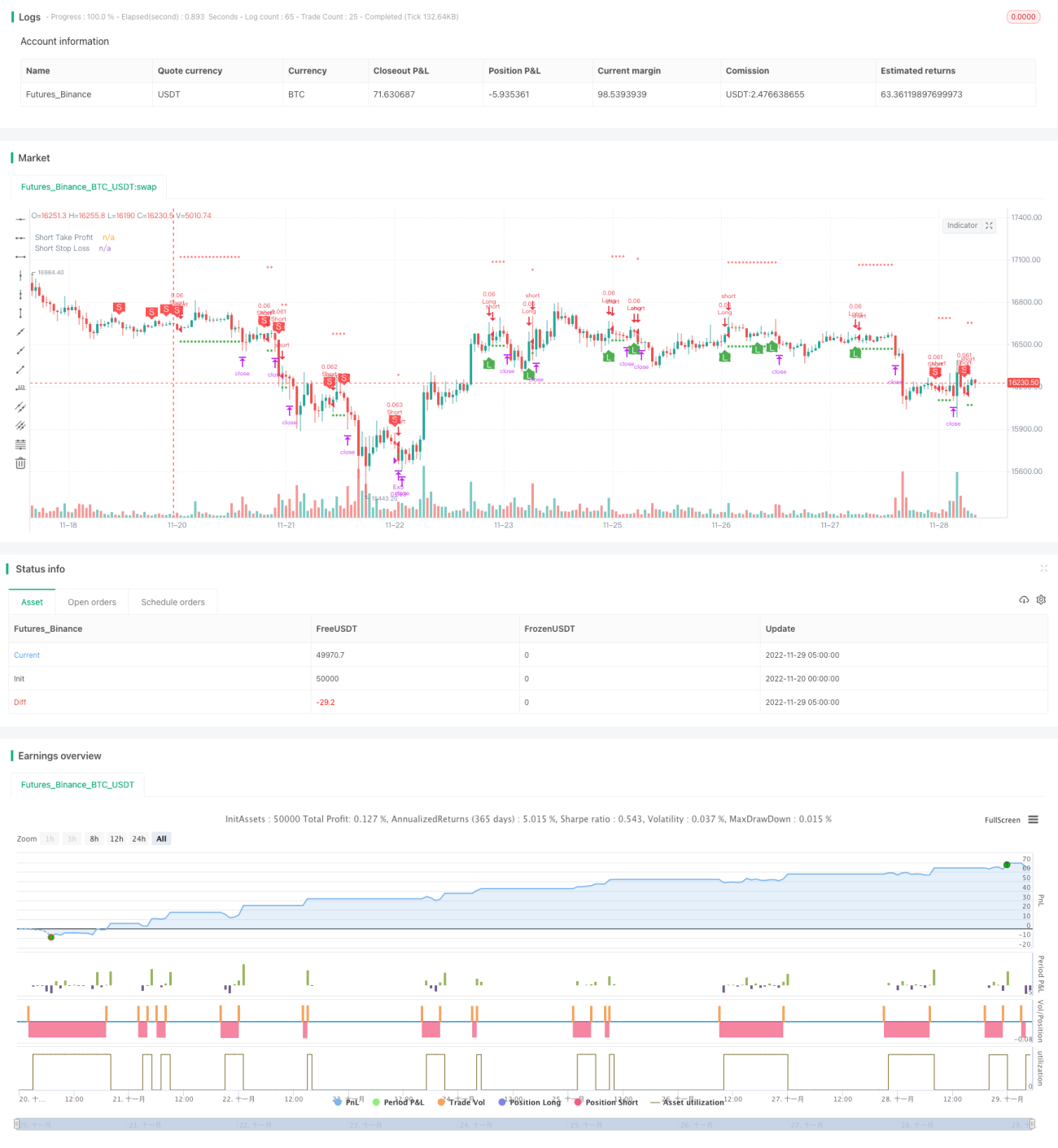

/*backtest

start: 2022-11-20 00:00:00

end: 2022-11-29 05:20:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1