Stratégie quantitative de suivi de tendance basée sur le SAR

Aperçu

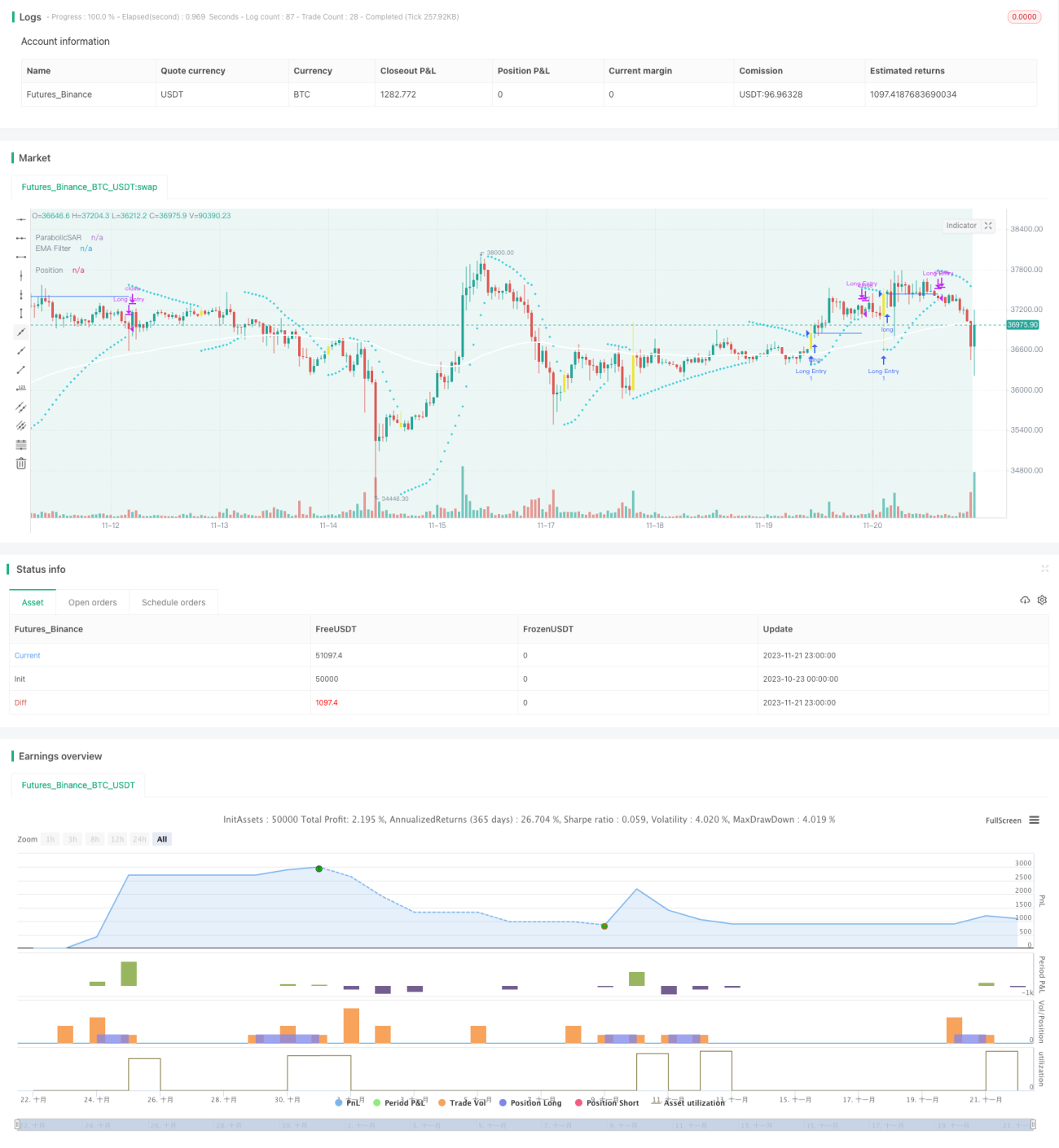

La stratégie de l'écart spéculatif est une stratégie de trading quantitatif de suivi de tendance qui utilise la courbe lissée SAR comme signal de trading principal, complétée par plusieurs filtres tels que l'EMA, la dynamique de compression et l'oscillateur de volatilité. En configurant les paramètres SAR, elle identifie les points de retournement de tendance pour réaliser un suivi de tendance à faible risque. C'est une stratégie idéale pour les investissements à moyen et long terme.

Principe de la stratégie

Cette stratégie utilise le SAR parabolique comme indicateur de signal de trading principal. Le SAR permet de déterminer efficacement les points de retournement de la tendance des prix. Lorsque le signe du SAR change, cela indique un renversement de tendance. En général, la stratégie émet un signal d'achat ou de vente lors du retournement du SAR.

De plus, la stratégie propose une option de franchissement du SAR. C'est-à-dire que, avant que le SAR ne se retourne complètement, le prix a déjà franchi la dernière valeur SAR, générant ainsi un signal. Cela permet d'améliorer la sensibilité de la stratégie.

Pour filtrer les faux signaux, la stratégie intègre trois filtres auxiliaires : EMA, dynamique de compression et oscillateur de volatilité. Ils peuvent être utilisés seuls ou en combinaison pour confirmer la fiabilité de la tendance des prix et des signaux de trading.

Enfin, la stratégie propose trois méthodes de stop-loss et take-profit : stop-loss fixe, take-profit fixe et stop-loss basé sur le ratio risque-récompense. Cela permet à la stratégie de s'adapter de manière flexible aux caractéristiques de différents types d'instruments de trading.

Analyse des avantages

-

Le SAR peut déterminer avec précision les retournements de tendance des prix et capturer rapidement de nouvelles tendances, ce qui le rend adapté au suivi de tendance à moyen et long terme.

-

La configuration de multiples filtres réduit la probabilité de faux franchissements et améliore la fiabilité des signaux.

-

La configuration est simple et flexible, avec des paramètres personnalisables pour s'adapter à différents instruments de trading.

-

Plusieurs méthodes de take-profit et stop-loss permettent de rechercher un équilibre entre risque et récompense.

-

Peut être directement connecté à un robot de trading pour une automatisation des transactions.

Analyse des risques

-

Sur un marché non directionnel (sans tendance), on peut observer une augmentation des faux signaux et des transactions inefficaces.

-

Un réglage inapproprié des paramètres SAR peut également affecter la précision de la détection des signaux.

-

En tant que stratégie de suivi de tendance, elle risque d'atteindre facilement le niveau de stop-loss dans les marchés fortement volatils.

Face à ces risques, il est possible d'ajuster les paramètres SAR ou les paramètres des filtres pour réduire la probabilité de transactions inefficaces. On peut également assouplir les limites de stop-loss pour supporter des fluctuations de marché plus importantes.

Axes d'optimisation

-

Optimisation des paramètres SAR. On peut optimiser le pas et l'incrément du SAR via des backtests historiques pour obtenir une stratégie plus stable et efficace.

-

Introduire des indicateurs de jugement de tendance. Ajouter des indicateurs auxiliaires comme le MACD, le DMI pour améliorer la capacité à juger la tendance.

-

Optimiser le ratio risque-récompense. Ajuster les pourcentages de take-profit et stop-loss fixes ainsi que le ratio risque-récompense pour accepter un risque plus élevé en vue d'obtenir un rendement plus important.

-

Ajouter des instruments de change. Actuellement, la stratégie ne prend en charge que les crypto-monnaies ; on peut l'étendre aux marchés des devises, des matières premières et des titres.

Résumé

L'écart spéculatif est une stratégie quantitative de suivi de tendance très pratique. Elle est réactive, ses signaux sont fiables, et grâce à une gestion des stop-loss et take-profit, elle peut générer des rendements stables à long terme. Une optimisation appropriée des paramètres et des règles peut encore améliorer son efficacité. C'est une stratégie quantitative efficace qui mérite d'être utilisée sur le long terme.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1