Stratégie de trading basée sur la tendance des vagues

Aperçu

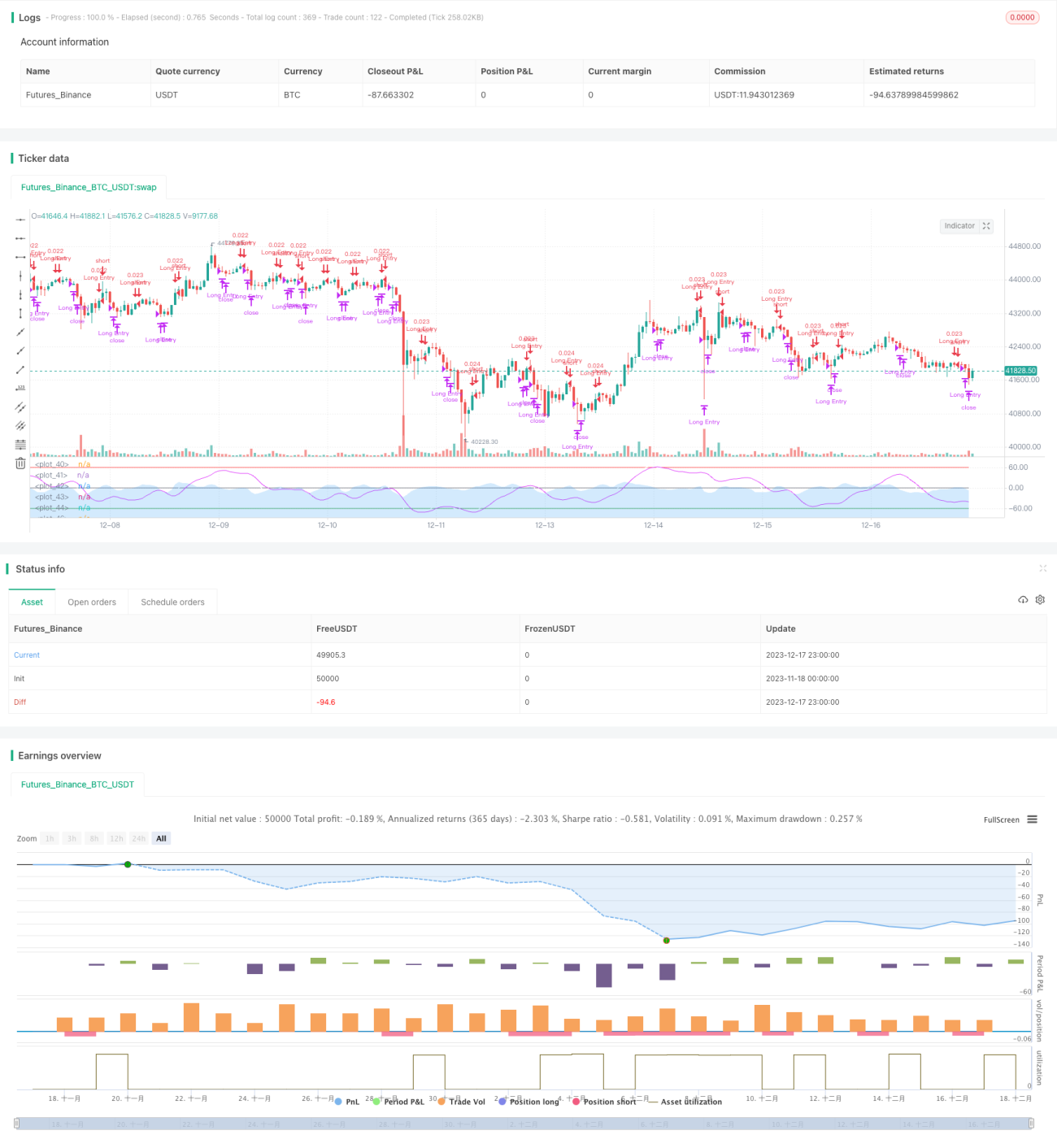

Il s'agit d'une stratégie de trading basée sur l'indicateur de tendance ondulatoire de LazyBear. Cette stratégie évalue les conditions de surachat et de survente du marché en calculant la tendance ondulatoire des fluctuations de prix, afin d'effectuer des opérations longues et courtes.

Principe de la stratégie

La stratégie repose principalement sur l'indicateur de tendance ondulatoire de LazyBear. On calcule d'abord le prix moyen (AP), puis la moyenne mobile exponentielle (ESA) de l'AP et la moyenne mobile exponentielle de la variation absolue du prix (D). À partir de là, on calcule l'indice de volatilité (CI), puis sa moyenne mobile exponentielle pour obtenir la ligne de tendance ondulatoire (WT). La WT est ensuite lissée par une moyenne mobile simple pour générer WT1 et WT2. Lorsque WT1 passe au-dessus de WT2, il s'agit d'un croisement doré (Golden Cross) qui signale une position longue ; lorsque WT1 passe en dessous de WT2, c'est un croisement mortel (Death Cross) qui signale une position courte.

Analyse des avantages

Il s'agit d'une stratégie de suivi de tendance très simple mais très pratique. Ses principaux avantages sont les suivants :

- Basée sur l'indicateur de tendance ondulatoire, elle permet d'identifier clairement la tendance des prix et le sentiment du marché.

- En utilisant les croisements dorés et mortels de la WT, les points d'entrée et de sortie sont faciles à déterminer.

- Les paramètres peuvent être personnalisés pour ajuster la sensibilité de la ligne WT, adaptée à différentes périodes.

- Des conditions supplémentaires peuvent être ajoutées pour filtrer les signaux, par exemple en limitant la fenêtre de trading.

Analyse des risques

Cette stratégie comporte également certains risques :

- En tant que stratégie de suivi de tendance, elle génère de nombreux faux signaux dans les marchés en range.

- La ligne WT présente un certain retard, ce qui peut entraîner des signaux manqués lors des retournements rapides.

- Les paramètres par défaut peuvent ne pas convenir à tous les actifs et à toutes les périodes ; une optimisation est nécessaire.

- Il n'y a pas de mécanisme de stop-loss, ce qui peut entraîner des positions unidirectionnelles trop longues.

Les principales solutions sont les suivantes :

- Optimiser les paramètres pour ajuster la sensibilité de la ligne WT.

- Ajouter d'autres indicateurs pour confirmer les signaux et éviter les faux signaux.

- Mettre en place un stop-loss et un take-profit.

- Limiter le nombre de transactions par jour ou la taille des positions.

Pistes d'optimisation

Cette stratégie peut encore être améliorée :

- Optimiser les paramètres de la WT pour la rendre plus réactive ou plus stable.

- Utiliser différentes combinaisons de paramètres selon la période.

- Ajouter des indicateurs de volume et de volatilité comme signaux de confirmation.

- Intégrer une logique de stop-loss et de take-profit.

- Enrichir les méthodes de positionnement, par exemple l'ajout pyramidal, le trading en grille, etc.

- Combiner des approches d'apprentissage automatique pour trouver de meilleures caractéristiques et règles de trading.

Résumé

Cette stratégie est une approche très simple et pratique de suivi de tendance ondulatoire. En calculant la tendance des fluctuations de prix, elle identifie les conditions de surachat et de survente du marché et utilise les croisements dorés et mortels de la ligne WT pour générer des signaux de trading. La stratégie est simple à mettre en œuvre. Cependant, en tant que stratégie de tendance, sa sensibilité et sa stabilité aux prix doivent être optimisées, et elle doit être combinée avec d'autres indicateurs et logiques pour éviter les faux signaux. Dans l'ensemble, il s'agit d'un modèle de stratégie très pratique offrant un large potentiel d'optimisation.

- 1