Stratégie de franchissement par croisement doré des doubles EMA

Aperçu

Cette stratégie est une stratégie de suivi de tendance basée sur les croisements dorés et les croisements de la mort des moyennes mobiles exponentielles (EMA) sur 5 et 34 minutes. Lorsque la ligne rapide traverse la ligne lente par le bas, une position longue est ouverte ; lorsqu'elle traverse par le haut, une position courte est ouverte. Des take profit et stop loss sont également mis en place pour contrôler le risque.

Principe de la stratégie

- La ligne rapide EMA5 et la ligne lente EMA34 génèrent les signaux de trading. L'EMA5 réagit aux variations récentes du prix, tandis que l'EMA34 reflète les variations à moyen terme du prix.

- Lorsque la ligne rapide traverse la ligne lente par le bas, il s'agit d'un croisement doré, indiquant que la tendance à court terme est meilleure que la tendance à moyen terme ; on détient une position longue.

- Lorsque la ligne rapide traverse la ligne lente par le haut, il s'agit d'un croisement de la mort, indiquant que la tendance à court terme est moins bonne que la tendance à moyen terme ; on détient une position courte.

- Des take profit et stop loss sont définis pour verrouiller les profits et contrôler les risques.

Analyse des atouts

- L'utilisation de deux EMA permet de filtrer les faux dépassements et d'éviter d'être piégé.

- Le suivi de la tendance à moyen terme améliore les opportunités de profit.

- La mise en place de take profit et stop loss contrôle efficacement le risque.

Analyse des risques

- La double EMA présente un retard, ce qui peut faire manquer des opportunités de trading à court terme.

- Si le stop loss est trop large, le risque de perte augmente.

- Si le take profit est trop serré, on risque de ne pas maximiser les gains.

Pistes d'optimisation

- Optimiser les paramètres des EMA pour trouver la meilleure combinaison.

- Optimiser les niveaux de take profit et stop loss pour verrouiller des profits plus importants.

- Ajouter d'autres indicateurs de filtrage, comme le MACD, le KDJ, etc., pour améliorer la précision des signaux.

Conclusion

Cette stratégie génère des signaux de trading via les croisements dorés et les croisements de la mort de deux EMA, et utilise des take profit et stop loss pour contrôler les risques. C'est une stratégie simple et efficace de suivi de tendance à moyen terme. L'optimisation des paramètres de take profit/stop loss et l'introduction d'autres indicateurs de filtrage peuvent renforcer encore la rentabilité stable de la stratégie.

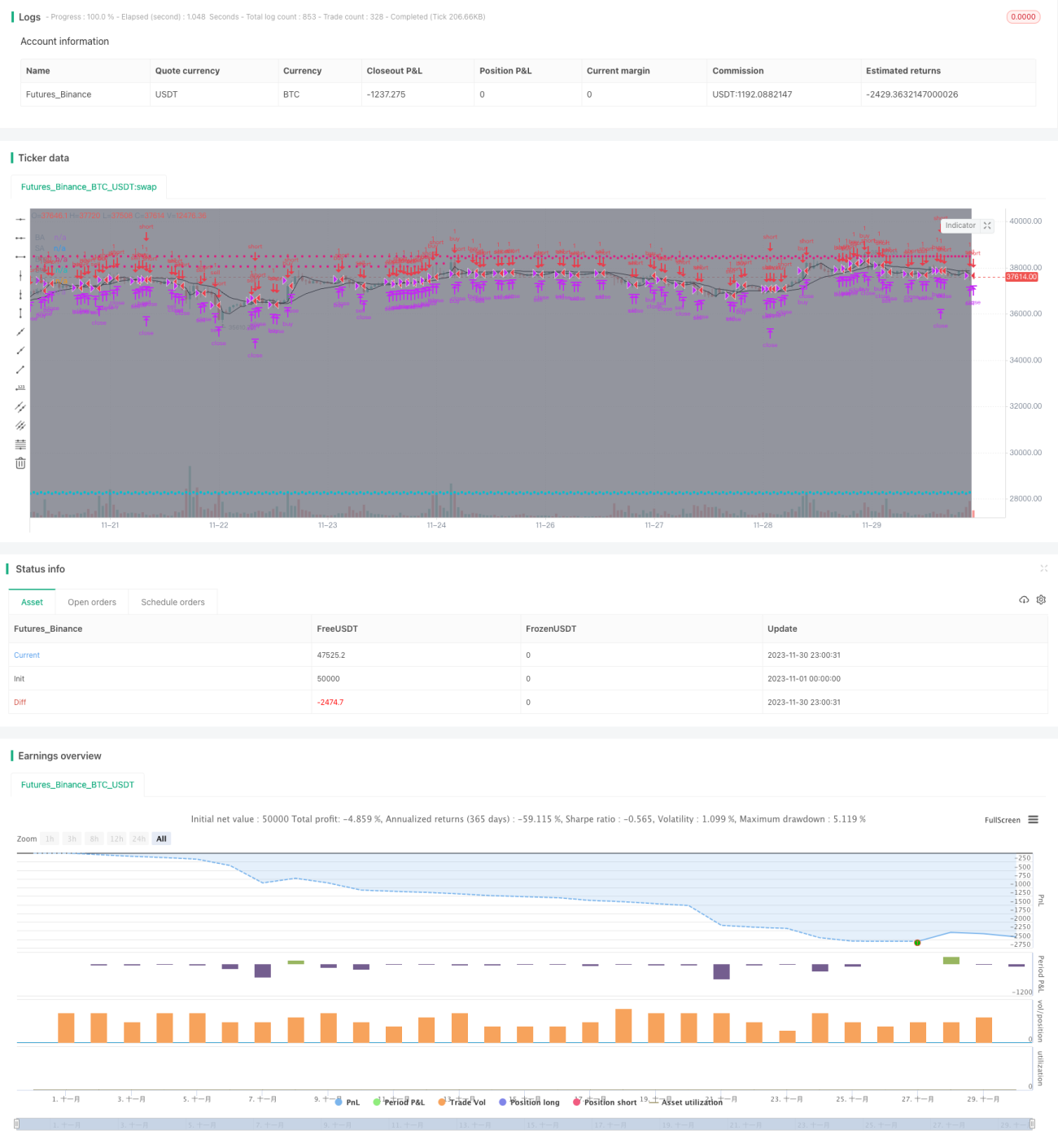

/*backtest

start: 2023-11-01 00:00:00

end: 2023-11-30 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title='[STRATEGY][RS]MicuRobert EMA cross V2', shorttitle='S', overlay=true, pyramiding=0, initial_capital=100000)

USE_TRADESESSION = input(title='Use Trading Session?', type=bool, defval=true)

USE_TRAILINGSTOP = input(title='Use Trailing Stop?', type=bool, defval=true)- 1