Stratégie de robot évolutive personnalisée avec MACD et MFI non-repeignants sur HTF

Vue d'ensemble

Cette stratégie est une combinaison hautement personnalisable des indicateurs MACD et MFI non-redessinés, adaptée aux robots de trading algorithmique. Elle combine un indicateur de tendance et un indicateur de momentum pour générer des signaux de trading via plusieurs filtres.

Principe de la stratégie

La stratégie utilise l'indicateur MACD pour déterminer la direction de la tendance du marché. Le MACD est un indicateur de momentum suiveur de tendance, qui soustrait une moyenne mobile rapide d'une moyenne mobile lente pour obtenir l'histogramme MACD, puis utilise une moyenne mobile exponentielle du MACD pour obtenir la ligne de signal. Lorsque la ligne rapide croise la ligne lente à la hausse, c'est un signal d'achat ; à la baisse, c'est un signal de vente.

De plus, la stratégie utilise l'indicateur MFI pour évaluer les conditions de surachat et de survente du marché. L'indicateur MFI combine les prix et les volumes, avec des valeurs fluctuant entre 0 et 100. Un MFI inférieur à 20 indique une zone de survente, tandis qu'un MFI supérieur à 80 indique une zone de surachat.

Pour filtrer les signaux erronés, la stratégie intègre également un filtre de tendance et un filtre RSI. Un signal d'achat est généré lorsque le prix est dans une tendance haussière et que le RSI est inférieur à un seuil défini.

Avantages de la stratégie

- Combine plusieurs indicateurs pour évaluer globalement l'état du marché, améliorant ainsi le taux de réussite

- Intègre des mécanismes de filtrage pour éviter les signaux erronés et réduire les trades inutiles

- Paramètres et filtres entièrement personnalisables pour s'adapter à différents instruments et préférences de trading

- Peut être utilisée pour le trading manuel ou connectée à un robot algorithmique pour un trading programmé

Risques de la stratégie et solutions

-

Un réglage inapproprié des paramètres de l'indicateur peut générer des signaux erronés

-

Possibilité de tester différents paramètres pour sélectionner la combinaison optimale

-

Les paramètres ne sont pas universels d'un instrument à l'autre ; des tests et optimisations séparés sont nécessaires

-

La fréquence de trading peut être trop élevée, augmentant les coûts de transaction et le risque de glissement

-

Possibilité d'ajuster les filtres pour réduire la fréquence des trades

-

En trading réel, veiller au contrôle des coûts

Pistes d'optimisation de la stratégie

- Tester des périodes de données plus longues pour évaluer la stabilité des paramètres

- Essayer différentes combinaisons de paramètres d'indicateurs

- Optimiser les poids des indicateurs pour améliorer la stabilité de la stratégie

- Ajouter davantage de filtres pour réduire les trades inutiles

Résumé

Cette stratégie est une stratégie de suivi de tendance hautement personnalisable, qui combine des indicateurs de tendance et de momentum pour juger de l'état du marché, et utilise efficacement des mécanismes de filtrage pour contrôler les risques. Elle peut être utilisée en trading manuel ou connectée à un robot algorithmique pour un trading automatisé à un niveau très élevé. C'est un système de stratégie qui mérite d'être suivi et optimisé sur le long terme.

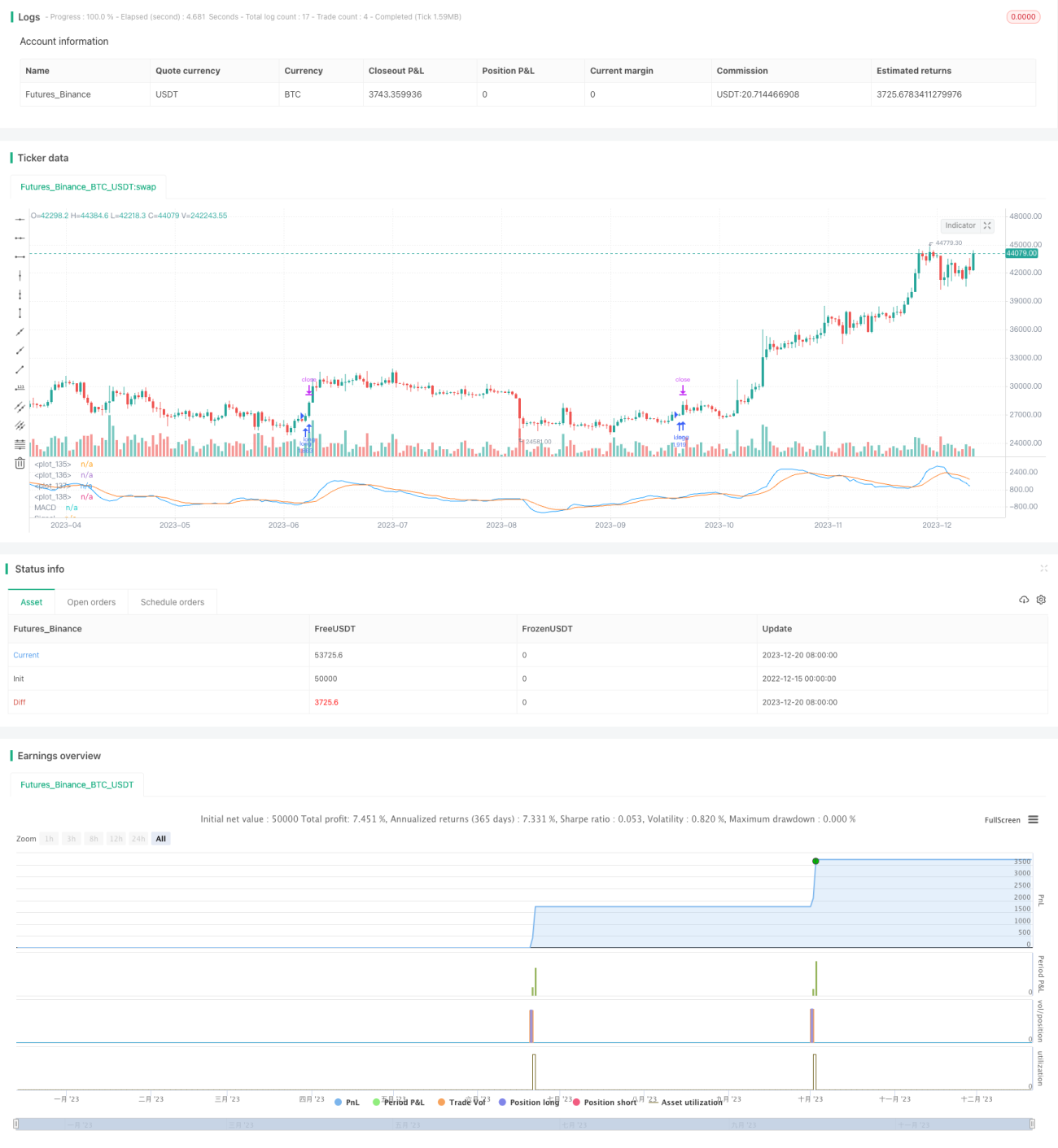

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1