Stratégie de trading Bitcoin basée sur des indicateurs quantitatifs

Aperçu

Cette stratégie utilise plusieurs indicateurs quantitatifs pour déterminer les moments d'achat et de vente du Bitcoin, permettant un trading automatisé. Elle inclut principalement l'indicateur Hull, le Relative Strength Index (RSI), les bandes de Bollinger (BB) et l'oscillateur de volume (VO).

Principe de la stratégie

-

Utilise une moyenne mobile Hull modifiée pour déterminer la tendance principale du marché, combinée aux bandes de Bollinger pour aider à identifier les points de rupture d'achat/vente.

-

L'indicateur RSI, associé à une plage de fluctuation adaptative, identifie les zones de surachat/survente et génère des signaux de trading. Deux ensembles de paramètres sont également configurés pour la validation des signaux en double (Duplicate).

-

L'oscillateur de volume évalue la force des pressions acheteuses et vendeuses, évitant ainsi les fausses cassures.

-

Des niveaux de stop-loss et de take-profit sont prédéfinis en fonction du rapport de paramètres stop-loss/take-profit, assurant une gestion des risques.

Analyse des avantages

-

La courbe Hull détecte plus rapidement les changements de tendance, et l'assistance des bandes de Bollinger réduit les faux signaux.

-

Les paramètres optimisés du RSI et la validation des signaux en double augmentent la fiabilité.

-

L'oscillateur de volume, combiné aux signaux de tendance et d'indicateurs, évite les transactions imprécises.

-

La méthode de stop-loss/take-profit prédéfinie contrôle automatiquement les pertes et gains unitaires, limitant efficacement le risque global.

Analyse des risques

-

Un réglage inapproprié des paramètres peut entraîner une fréquence de trading trop élevée ou une détérioration de l'efficacité des signaux.

-

En cas d'événements imprévus provoquant une volatilité extrême du marché, le stop-loss peut être franchi, entraînant des pertes importantes.

-

Lors du changement de paire de trading pour une autre crypto-monnaie, les paramètres doivent être retestés et optimisés.

-

En l'absence de données de volume, l'oscillateur de volume devient inefficace.

Pistes d'optimisation

-

Effectuer davantage de tests de combinaisons de paramètres du RSI pour trouver les réglages optimaux.

-

Essayer d'autres indicateurs comme le MACD ou le KD en combinaison avec le RSI pour améliorer la précision des signaux.

-

Ajouter un module de prédiction basé sur l'apprentissage automatique pour déterminer la direction du marché.

-

Tester l'efficacité des paramètres en remplaçant la paire de trading par d'autres actifs.

-

Optimiser l'algorithme de stop-loss/take-profit pour maximiser les profits.

Conclusion

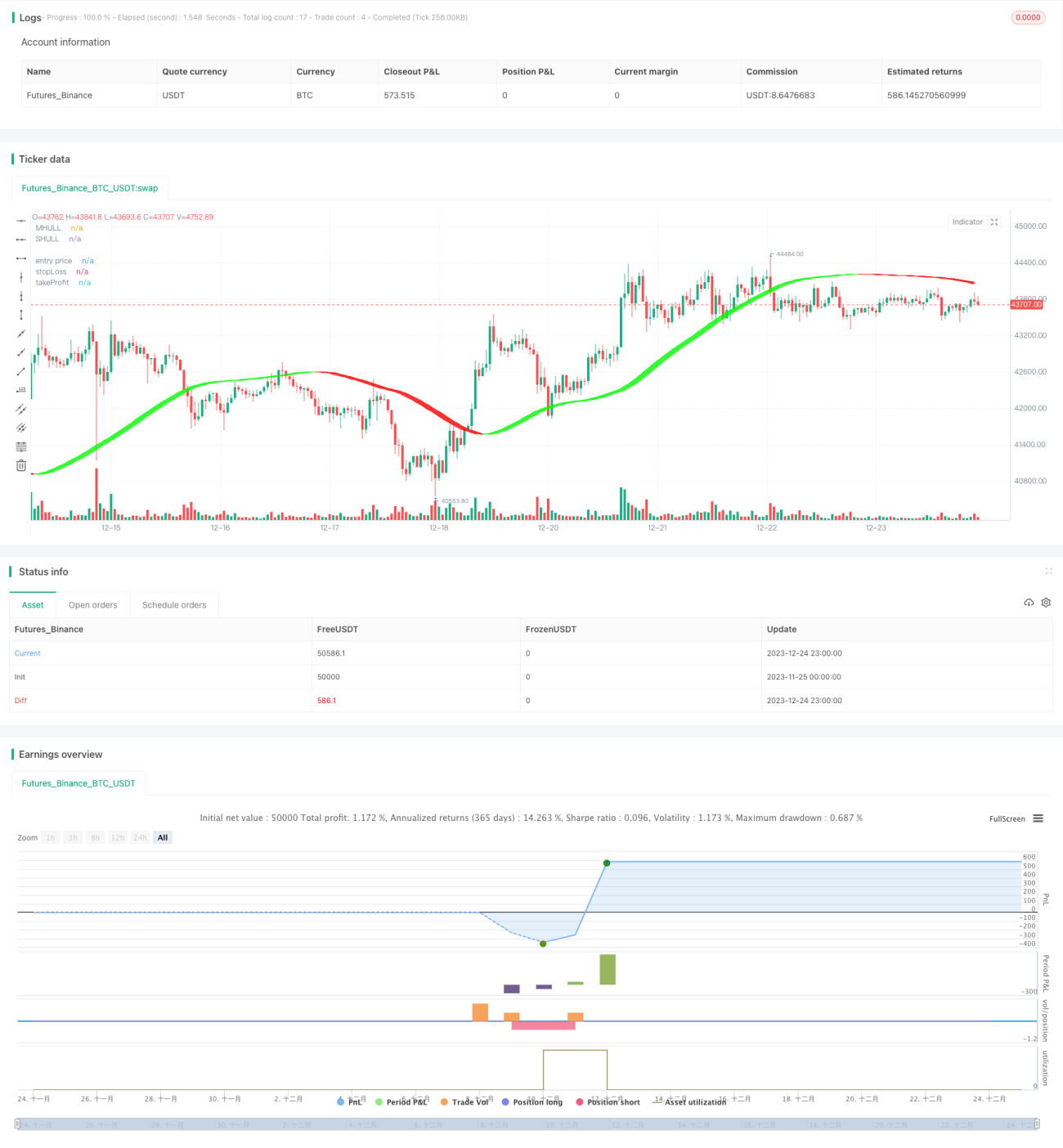

Cette stratégie combine plusieurs indicateurs techniques quantitatifs pour déterminer les moments de trading. Grâce à l'optimisation des paramètres et aux méthodes de contrôle des risques, elle permet un trading automatisé du Bitcoin. Les résultats sont satisfaisants, mais des tests et optimisations continus sont nécessaires pour s'adapter aux évolutions du marché. Elle peut servir de référence aux investisseurs pour les aider dans leurs décisions de trading.

- 1