Stratégie intraday de suivi de tendance avec arrêts multiples intégrés

Aperçu

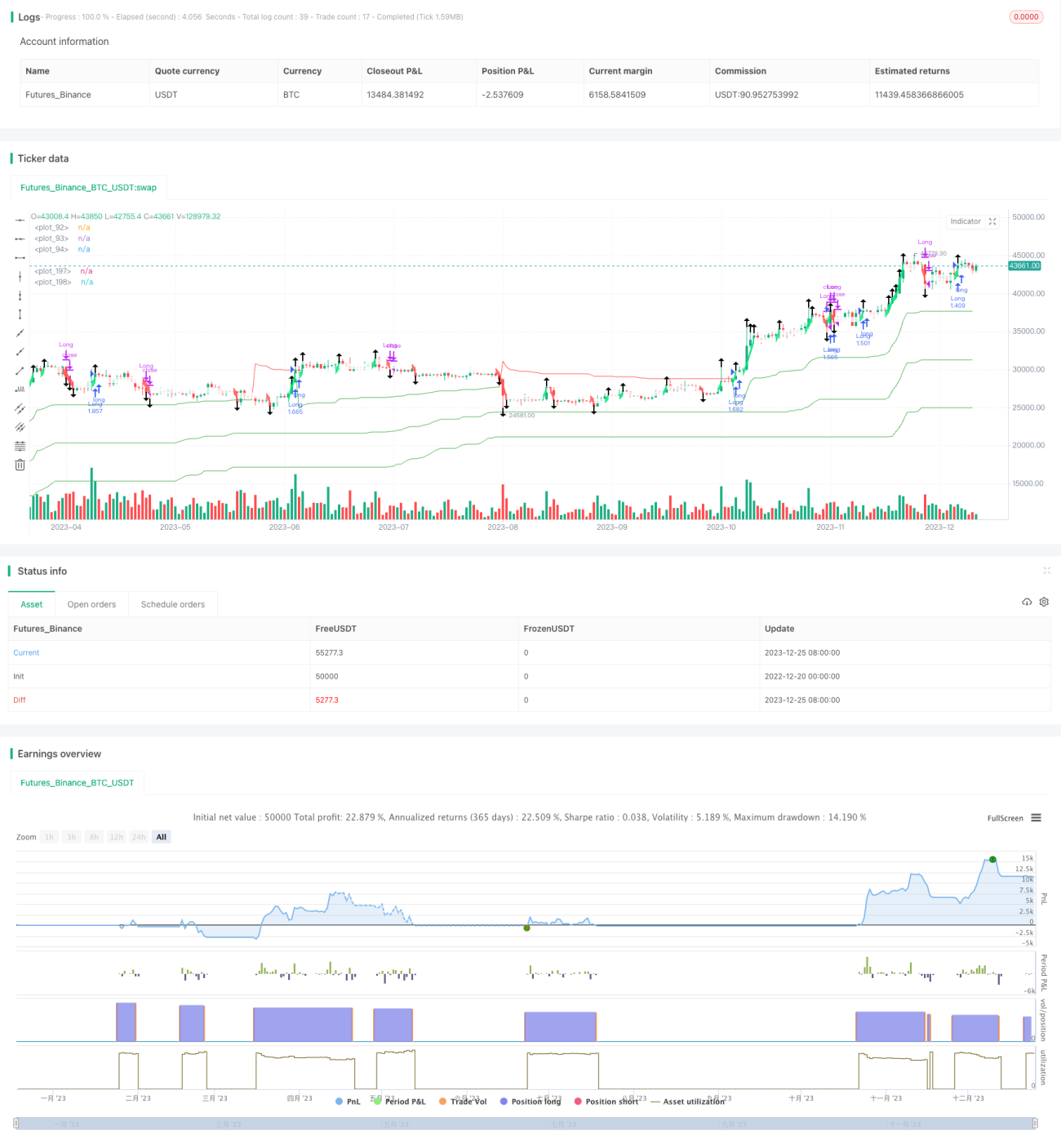

Cette stratégie intègre plusieurs stop-loss dynamiques basées sur l'ATR et des briques Renko améliorées, dans le but de capturer les tendances intraday. Elle combine des indicateurs de tendance et des indicateurs de briques pour réaliser une analyse multi-périodes, permettant d'identifier efficacement la direction de la tendance et de stopper les pertes à temps.

Principe de la stratégie

Le cœur de cette stratégie réside dans le mécanisme de stop-loss multiple basé sur l'ATR. Elle met en place 3 groupes de stop-loss dynamiques ATR, avec des paramètres respectifs de 5 fois l'ATR, 10 fois l'ATR et 15 fois l'ATR. Lorsque le prix franchit ces trois lignes de stop-loss à la baisse, cela indique un changement de tendance, et la position est fermée. Ce réglage de stop-loss multiples permet de filtrer efficacement les faux signaux dus aux fluctuations à court terme.

L'autre composante essentielle est la brique Renko améliorée. Celle-ci divise les incréments en fonction de la valeur de l'ATR et utilise l'indicateur SMA pour déterminer la direction de la tendance. Elle est plus sensible qu'une brique Renko classique et peut confirmer plus tôt les changements de tendance. Lorsque la couleur de la brique change, cela signale un retournement de tendance et peut servir de signal de stop-loss.

La condition d'entrée est : lorsque le prix franchit les trois stop-loss ATR à la hausse, on prend une position longue ; lorsqu'il les franchit à la baisse, on prend une position courte. La condition de sortie est : lorsque le prix déclenche l'un des stop-loss ATR ou que la couleur des briques Renko change, on ferme la position.

Avantages de la stratégie

- Stop-loss multi-ATR, contrôle efficace des risques.

- Briques Renko améliorées, plus sensibles, permettant un stop-loss anticipé.

- Combinaison d'indicateurs de tendance et de briques, assurant la capture des tendances.

- Analyse multi-périodes, plus fiable pour déterminer la direction de la tendance.

- Paramètres ajustables pour s'adapter à différents environnements de marché.

Risques et optimisation de la stratégie

Le principal risque de cette stratégie réside dans le fait que le stop-loss peut être dépassé, entraînant une perte plus importante. Les optimisations suivantes sont possibles :

- Ajuster le multiple du stop-loss ATR : l'assouplir dans les marchés fortement tendanciels, le resserrer dans les marchés faibles.

- Ajuster les paramètres de la période ATR des briques Renko pour équilibrer sensibilité et stabilité.

- Ajouter d'autres indicateurs de stop-loss, comme le canal de Donchian, pour garantir une fiabilité accrue du stop-loss.

- Ajouter un filtre pour éviter les transactions fréquentes en période de consolidation.

Résumé

Dans l'ensemble, cette stratégie convient aux fortes tendances intraday. Ses caractéristiques sont un réglage scientifique du stop-loss et la capacité des briques à identifier à l'avance les retournements de tendance. Grâce à l'ajustement des paramètres, elle peut s'adapter à différents environnements de marché. C'est une stratégie de suivi de tendance digne d'être testée en conditions réelles.

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Lancelot vstop intraday strategy", overlay=true, currency=currency.NONE, initial_capital = 100, commission_type=strategy.commission.percent,

commission_value=0.075, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

- 1