Stratégie de suivi de tendance basée sur QQE et MA

Aperçu

Cette stratégie est une stratégie de suivi de tendance basée sur l'indicateur QQE (Qualitative Quantitative Estimation) et les moyennes mobiles. Elle détermine la direction de la tendance en utilisant le croisement de l'indicateur QQE rapide et le filtrage de la direction des moyennes mobiles, générant des signaux d'achat et de vente.

La stratégie offre trois types de croisements de l'indicateur QQE pour identifier les signaux : (1) croisement de l'indicateur RSI lissé avec l'axe zéro ; (2) croisement de l'indicateur RSI lissé avec la ligne QQE rapide ; (3) sortie de l'indicateur RSI lissé du canal de seuil RSI. Par défaut, le troisième type est utilisé pour ouvrir une position et le deuxième pour la fermer.

Les signaux d'achat et de vente peuvent être filtrés par les moyennes mobiles : le prix de clôture doit être supérieur (inférieur) à la moyenne mobile rapide, et la moyenne mobile rapide doit être supérieure (inférieure) à la moyenne mobile lente pour générer un signal.

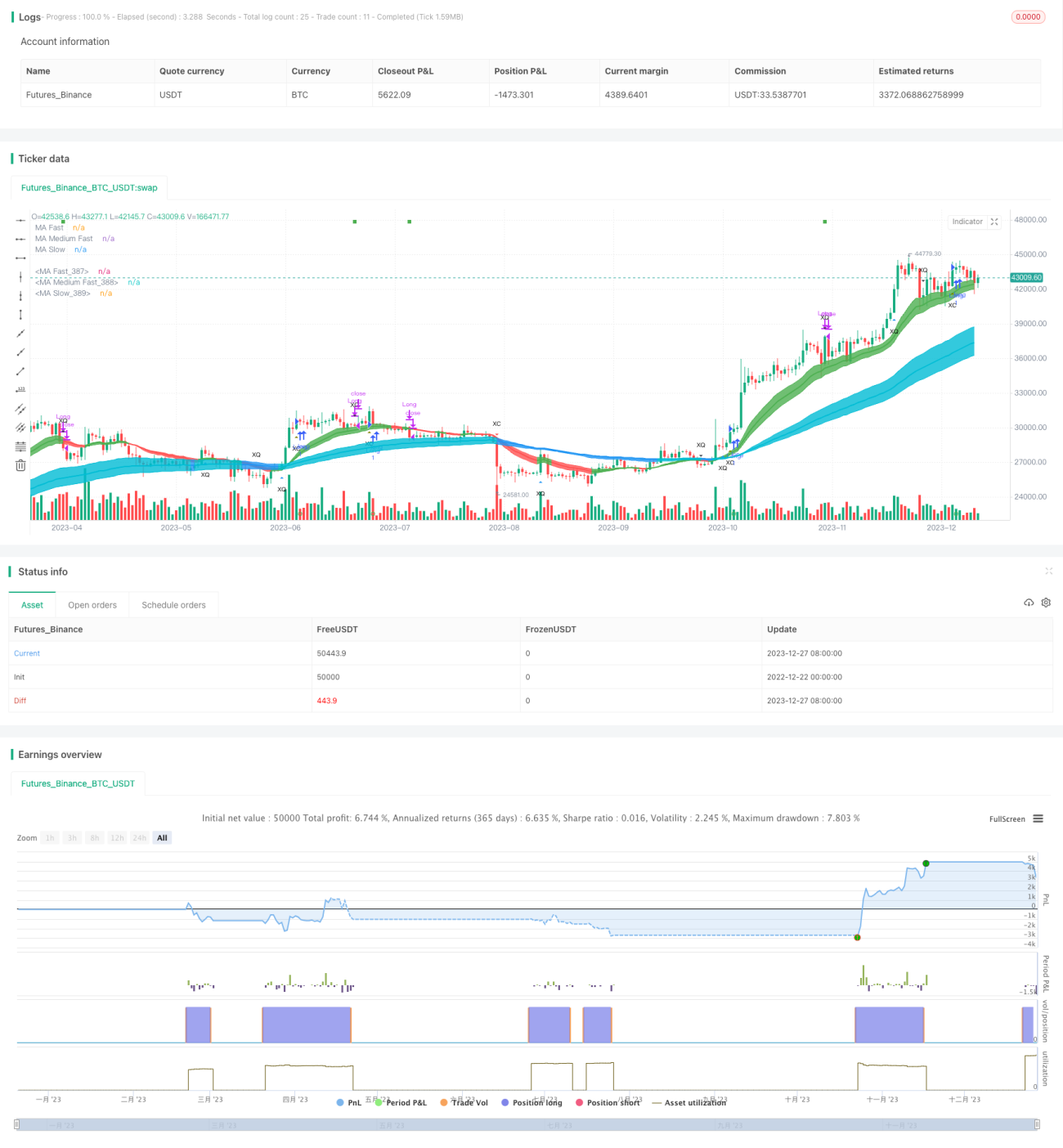

Cette stratégie convient au mode signal-sur-signal des systèmes de trading automatisé.

Principe

L'indicateur central de cette stratégie est le QQE, dont la formule de calcul est la suivante :

Wilders_Period = RSILen * 2 - 1

Rsi = rsi(close,RSILen)

RSIndex = ema(Rsi, SF)

AtrRsi = abs(RSIndex - RSIndex[1])

MaAtrRsi = ema(AtrRsi, Wilders_Period)

DeltaFastAtrRsi = ema(MaAtrRsi,Wilders_Period) * QQEfactor

newshortband = RSIndex + DeltaFastAtrRsi

newlongband = RSIndex - DeltaFastAtrRsi

Où RSILen est la longueur de la période du RSI et SF est le facteur de lissage du RSI. Le QQE est essentiellement un RSI lissé. Il calcule des canaux supérieur et inférieur à l'aide d'un ATR rapide. Lorsque le prix dépasse le canal, cela est interprété comme une opportunité d'achat ou de vente.

Cette stratégie utilise trois types de croisements du QQE pour identifier les signaux de trading :

- Croisement de l'indicateur RSI lissé avec l'axe zéro (XZ)

QQEzlong = RSIndex >= 50 ? QQEzlong + 1 : 0

QQEzshort = RSIndex < 50 ? QQEzshort + 1 : 0

- Croisement de l'indicateur RSI lissé avec l'indicateur QQE rapide (XQ), similaire à un signal de retournement anticipé

QQExlong = FastAtrRsiTL < RSIndex ? QQExlong + 1 : 0

QQExshort = FastAtrRsiTL > RSIndex ? QQExshort + 1 : 0

- Sortie de l'indicateur RSI lissé du canal de seuil (XC), similaire à un signal de retournement confirmé

threshhold = 10

QQEclong = RSIndex > (50 + threshhold) ? QQEclong + 1 : 0

QQEcshort = RSIndex < (50 - threshhold) ? QQEcshort + 1 : 0

On peut choisir un ou plusieurs de ces trois types de croisements pour identifier les signaux d'achat/vente et de clôture.

Les signaux d'achat et de vente peuvent être filtrés par les moyennes mobiles :

// Conditions de filtrage

QQEflong = close > ma_medium et

ma_medium > ma_slow et

ma_fast > ma_medium

QQEfshort = close < ma_medium et

ma_medium < ma_slow et

ma_fast < ma_medium

Cela permet d'éviter les faux signaux en période de range.

Cette stratégie convient au trading automatisé, en utilisant différents croisements QQE pour ouvrir et fermer les positions :

Signal d'ouverture = XC ou XQ ou XZ

Signal de clôture = XQ ou XZ

Avantages

Cette stratégie présente les avantages suivants :

-

Utilisation de l'indicateur QQE pour déterminer la tendance et les signaux de croisement. Le QQE, de par sa nature lissée, réduit les faux signaux.

-

Combinaison avec le filtrage par moyennes mobiles, ce qui évite davantage les faux signaux en période de range et améliore la qualité des signaux.

-

Possibilité de choisir différents croisements QQE pour ouvrir et fermer des positions, permettant un trading automatisé.

-

En raison du décalage inhérent à l'indicateur RSI lissé, les signaux d'achat et de vente ne subissent pas de redessin.

-

Possibilité d'optimisation sur différentes périodes de temps pour trouver la meilleure combinaison de paramètres.

Risques

Cette stratégie comporte également certains risques :

-

En cas de retournement de tendance, des signaux erronés peuvent apparaître ; il est nécessaire de définir un stop loss pour contrôler le risque.

-

Un réglage inadéquat des paramètres peut affecter les performances de la stratégie. Il est nécessaire de tester et d'optimiser à plusieurs reprises pour trouver les meilleurs paramètres.

-

Les paramètres doivent être testés et optimisés séparément pour différents instruments et périodes de temps.

-

Le trading mécanisé comporte un risque de drawdown et de pertes consécutives, nécessitant une gestion rigoureuse du capital.

Les solutions correspondantes sont les suivantes :

-

Définir un stop loss pour sortir de la position lorsque la perte atteint un certain seuil.

-

Tester minutieusement différentes combinaisons de paramètres pour trouver les paramètres optimaux.

-

Ajuster les paramètres en fonction des caractéristiques de l'instrument et de la période.

-

Mettre en place une gestion rigoureuse du capital, ouvrir des positions par tranches et contrôler la taille de chaque position.

Axes d'optimisation

Cette stratégie peut être optimisée selon les axes suivants :

-

Optimiser les paramètres du QQE, notamment la longueur du RSI, la longueur de lissage du RSI, la longueur du fast ATR, etc., afin de trouver la combinaison optimale.

-

Optimiser les paramètres des moyennes mobiles, en ajustant la période et le type, pour obtenir la meilleure adéquation avec l'indicateur QQE.

-

Tester différents croisements QQE pour l'ouverture et la fermeture des positions, afin de trouver la combinaison la plus stable.

-

Affiner les paramètres en fonction des différents instruments et périodes de trading. Le trading intraday peut réduire les périodes pour améliorer la réactivité.

-

Ajouter un mécanisme de stop loss. Arrêter la position lorsque la perte atteint un certain pourcentage.

-

Réduire la taille des positions de manière appropriée et tester différentes méthodes de gestion des positions.

Résumé

Cette stratégie intègre l'indicateur QQE pour déterminer la tendance et les signaux de croisement, ainsi que des moyennes mobiles pour filtrer et générer des signaux de trading. En pratique, il est possible de régler les paramètres pour améliorer la qualité des signaux, et de combiner une gestion rigoureuse du capital pour contrôler le risque. Cette stratégie convient au mode signal-sur-signal du trading automatisé, et peut également servir d'aide à la décision dans le trading discrétionnaire. Grâce à l'optimisation des paramètres et des règles, elle peut s'adapter à un plus grand nombre de conditions de marché.

- 1