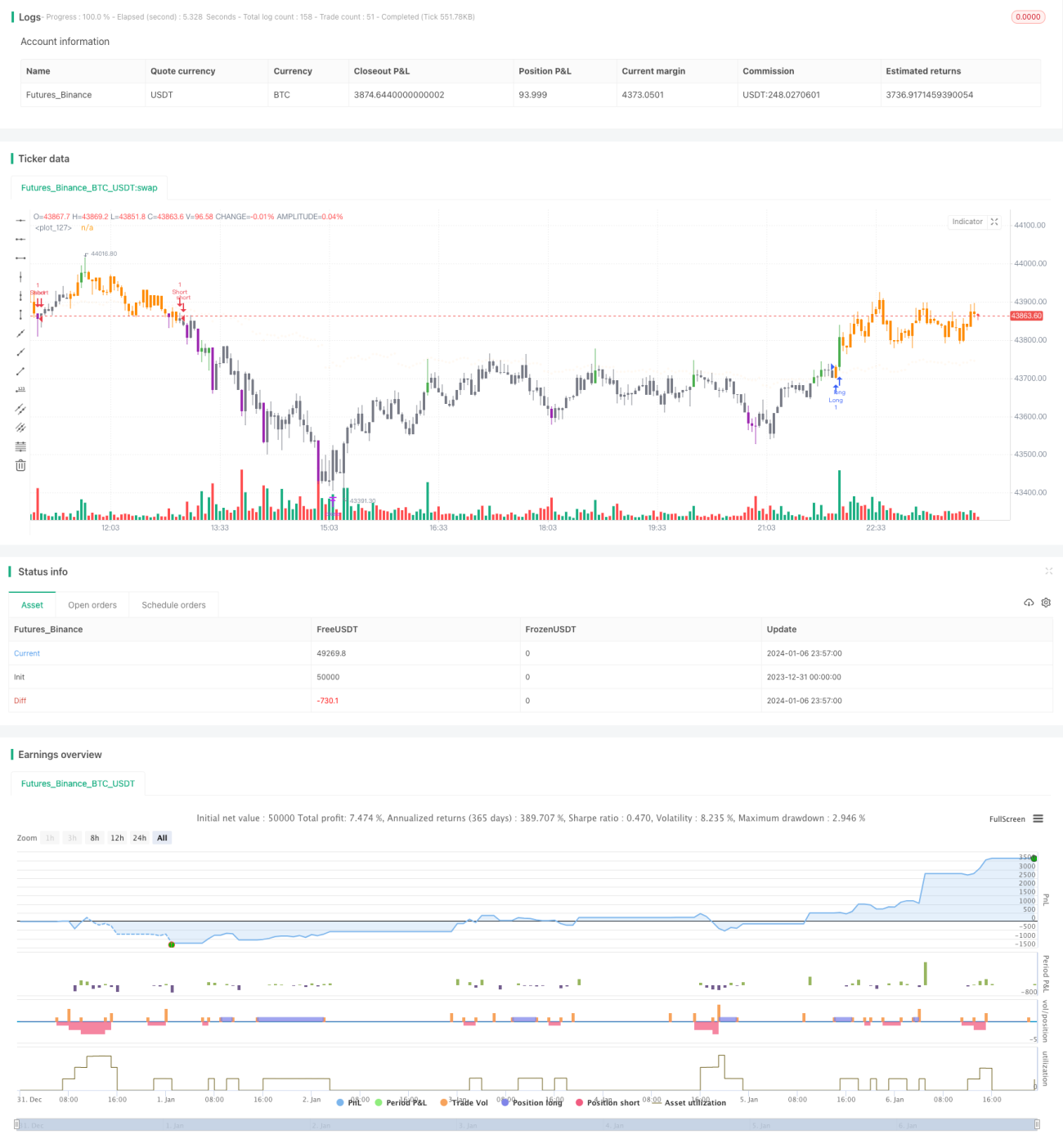

Stratégie de trading oscillant basée sur deux moyennes mobiles

Aperçu

Cette stratégie est une stratégie de trading basée sur deux moyennes mobiles pour les marchés à tendance latérale (oscillations). Elle utilise les croisements d'une moyenne mobile rapide et d'une moyenne mobile lente comme signaux d'achat et de vente. Un signal d'achat est généré lorsque la moyenne mobile rapide croise la moyenne mobile lente par le bas, et un signal de vente est généré lorsque la moyenne mobile rapide croise la moyenne mobile lente par le haut. Cette stratégie est adaptée aux marchés en range, permettant de capter les fluctuations à court terme pour réaliser des bénéfices.

Principe de la stratégie

La stratégie utilise une RMA (Relative Moving Average) de période 6 comme moyenne mobile rapide, et une HMA (Hull Moving Average) de période 4 comme moyenne mobile lente. Elle détermine la tendance des prix et génère des signaux de trading via les croisements des deux lignes.

Lorsque la ligne rapide croise la ligne lente par le bas, cela indique que le prix passe d'une baisse à une hausse à court terme, représentant un moment de transfert de positions, et la stratégie génère alors un signal d'achat. Lorsque la ligne rapide croise la ligne lente par le haut, cela indique que le prix passe d'une hausse à une baisse à court terme, représentant également un moment de transfert de positions, et la stratégie génère alors un signal de vente.

De plus, la stratégie vérifie également le jugement de la tendance à long terme pour éviter les transactions à contre-tendance. Ce n'est que lorsque le jugement de la tendance à long terme est également en faveur du signal que les signaux d'achat et de vente réels sont générés.

Avantages de la stratégie

Cette stratégie présente les avantages suivants :

- L'utilisation des croisements de deux moyennes mobiles permet d'identifier efficacement les points de retournement des prix à court terme.

- Les périodes des lignes rapides et lentes sont bien assorties, produisant des signaux de trading relativement précis.

- La combinaison du jugement des tendances à court et à long terme permet de filtrer la plupart des signaux bruyants.

- Implémente une logique de stop loss et de take profit pour éviter activement les risques.

- Facile à comprendre et à mettre en œuvre, adapté aux débutants en trading quantitatif.

Risques et solutions

Cette stratégie comporte également certains risques :

-

Les stratégies à double moyenne mobile ont tendance à générer de nombreux petits gains mais peuvent subir une perte importante unique. Solution : ajuster correctement les niveaux de take profit et de stop loss.

-

En marchés en range, les signaux de trading peuvent être fréquents, entraînant un excès de transactions. Solution : assouplir raisonnablement les conditions de trading pour réduire le nombre de transactions.

-

Les paramètres de la stratégie sont facilement suroptimisés, ce qui peut nuire à sa performance en conditions réelles. Solution : effectuer des tests de robustesse des paramètres.

-

La stratégie est peu performante en marchés en tendance. Solution : ajouter un module de jugement de tendance ou la combiner avec des stratégies de suivi de tendance.

Axes d'optimisation

La stratégie peut être optimisée dans les directions suivantes :

- Mettre à jour les indicateurs de moyenne mobile en utilisant des filtres adaptatifs comme le filtre de Kalman.

- Ajouter un module d'apprentissage automatique pour utiliser l'IA afin d'identifier les points d'achat et de vente.

- Ajouter un module de gestion du capital pour automatiser davantage le contrôle des risques.

- Combiner avec des facteurs haute fréquence pour obtenir des signaux de trading plus forts.

- Arbitrage inter-marchés sur plusieurs instruments.

Résumé

Cette stratégie de trading en range basée sur deux moyennes mobiles est, dans l'ensemble, une stratégie de trading quantitatif typique et pratique. Elle possède une forte adaptabilité et les débutants peuvent y apprendre beaucoup de choses sur le développement de stratégies. Parallèlement, elle offre une grande marge d'amélioration, pouvant être optimisée en intégrant davantage de techniques quantitatives pour obtenir de meilleurs résultats.

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © dc_analytics

// https://datacryptoanalytics.com/

- 1