Stratégie de croisement de doubles moyennes mobiles pondérées par la dynamique

Aperçu

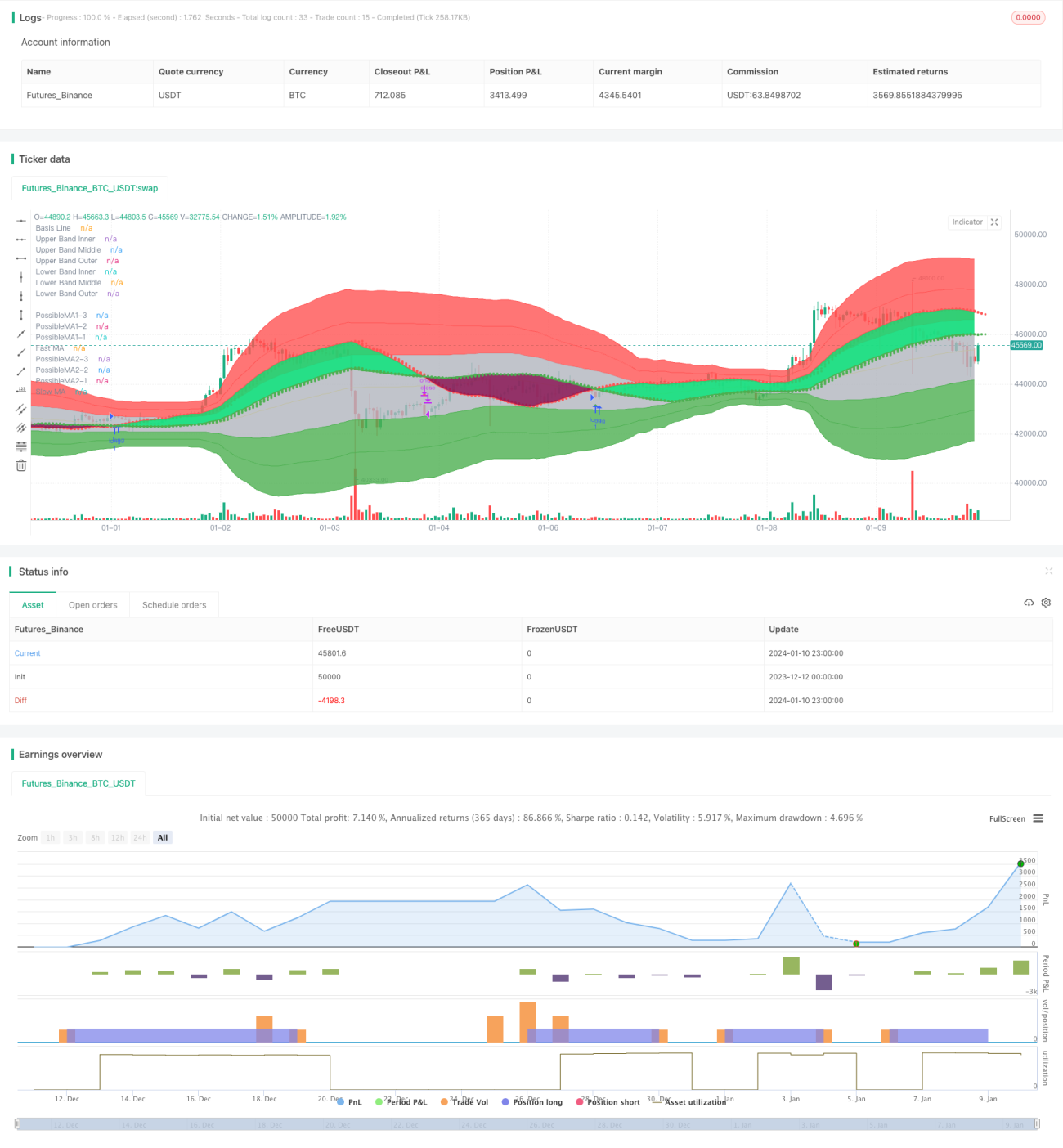

Cette stratégie génère des signaux d'achat et de vente lors du croisement de deux moyennes mobiles exponentielles pondérées par la dynamique (MAEMA) de périodes différentes. La ligne courte sert à juger les tendances du marché et les signaux de retournement à court terme, tandis que la ligne longue détermine la direction principale de la tendance.

Principe

- Calculer la MAEMA de la ligne rapide (80 périodes) et de la ligne lente (144 périodes).

- La ligne rapide reflète les tendances courtes et les points de retournement. La ligne lente indique la direction principale de la tendance.

- Lorsque la ligne rapide croise au-dessus de la ligne lente, un signal d'achat est généré. Lorsqu'elle croise en dessous, un signal de vente est produit.

- La stratégie trace également trois points de prédiction pour estimer les valeurs possibles de la période suivante, permettant de juger les tendances futures du croisement.

- Elle exploite pleinement la nature dynamique et la capacité prédictive de l'indicateur MAEMA.

Analyse des avantages

- La MAEMA intègre un facteur de dynamique, permettant de capter plus rapidement les changements de tendance.

- Stratégie à double moyenne mobile, évaluant la direction des tendances sur différentes périodes.

- La combinaison du croisement des lignes rapide/lente avec les points de prédiction de la MAEMA rend les signaux d'achat/vente plus fiables.

- Affichage graphique complet, reflétant intuitivement les fluctuations du marché.

Analyse des risques

- En cas de volatilité anormale, la sensibilité de la MAEMA peut être trop élevée et générer de faux signaux. Il est possible d'élargir le stop-loss.

- Le système de moyennes mobiles peut produire de faux signaux en période de range. L'ajout d'autres filtres est recommandé.

- Les paramètres de période pour les lignes rapide et lente doivent être optimisés selon les différents actifs.

Pistes d'optimisation

- Optimiser les paramètres de période des lignes rapide et lente de la MAEMA pour trouver la meilleure combinaison.

- Ajouter des conditions de filtrage pour éviter d'ouvrir des positions en période de consolidation, par exemple en intégrant le DMI, le MACD, etc. pour juger de la tendance.

- Ajuster les coefficients ATR et les points de stop-loss suiveur en fonction des résultats de backtest pour réduire les faux positifs et contrôler le risque.

Résumé

Cette stratégie utilise le croisement de deux moyennes mobiles exponentielles pondérées par la dynamique pour déterminer les changements de tendance du marché. Son principe de base est clair et simple. Grâce à la dynamique et à la fonction prédictive de la MAEMA, elle identifie efficacement les signaux de retournement. Il est nécessaire d'optimiser les paramètres et de renforcer les filtres pour améliorer la stabilité.

- 1