Stratégie de suivi de tendance basée sur les moyennes mobiles SSL

Aperçu

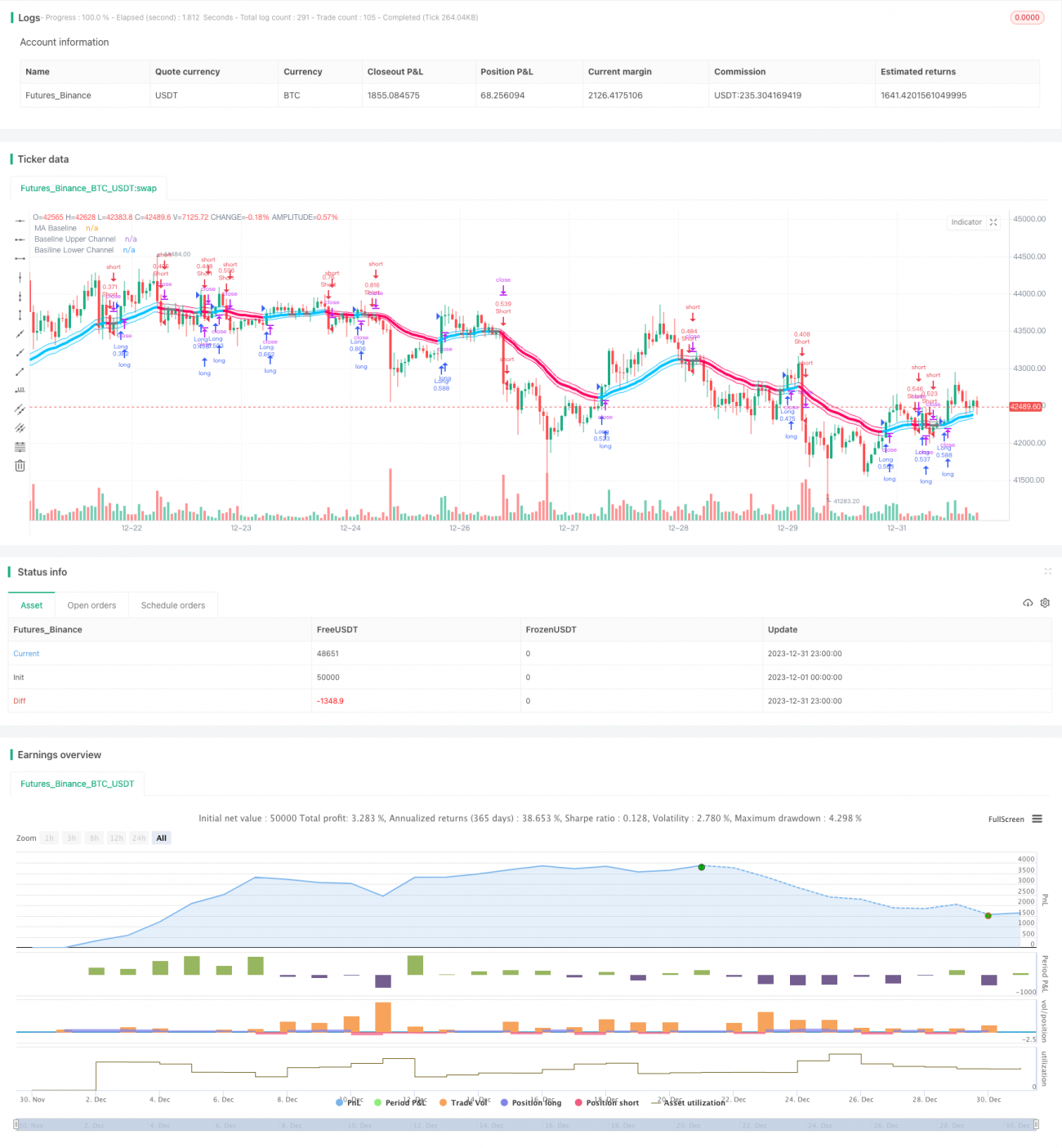

Cette stratégie utilise l'indicateur de canal SSL pour juger la tendance du marché et suit la tendance en se basant sur une moyenne mobile. Elle convient aux graphiques en 4 heures et quotidiens pour le moyen et long terme.

Principe de la stratégie

-

Le canal SSL est composé de la moyenne mobile de Keltner et de l'amplitude réelle. Il permet de déterminer la direction de la tendance du marché. Lorsque le prix franchit la bande supérieure, il s'agit d'un signal haussier ; lorsqu'il franchit la bande inférieure, c'est un signal baissier.

-

La stratégie utilise des indicateurs de moyenne mobile tels que l'EMA pour calculer une moyenne de base. Cette moyenne permet de filtrer une partie des faux signaux de rupture.

-

La stratégie prend une position longue lorsque le prix franchit la bande supérieure du canal SSL, et une position courte lorsqu'il franchit la bande inférieure. En tendance haussière, on achète sur les points hauts et vend sur les points bas ; en tendance baissière, on achète sur les points bas (ramasser le couteau).

-

Les méthodes de stop-loss incluent le stop-loss en pourcentage, le stop-loss basé sur l'ATR et le stop-loss basé sur le plus bas/haut des périodes précédentes. Le take-profit correspond à un multiple du stop-loss. Les paramètres spécifiques sont déterminés par l'utilisateur.

Analyse des avantages

-

Le canal SSL détermine la direction de la tendance avec précision, réduisant les faux signaux. Combiné à la moyenne mobile comme base d'entrée, il évite d'acheter au sommet ou de vendre au creux.

-

Possibilité de choisir différents types de moyennes mobiles, s'adaptant à une large gamme de conditions de marché.

-

Méthodes de stop-loss flexibles et variées, permettant un contrôle du risque. Le multiple de take-profit peut également être ajusté selon les préférences.

-

Possibilité d'ouvrir à la fois des positions longues et courtes, exploitant pleinement les opportunités bidirectionnelles du marché.

Analyse des risques

-

Les indicateurs de moyenne mobile présentent tous un décalage (lag), ce qui peut entraîner une accumulation de pertes.

-

En période de consolidation, dès que le prix franchit les bandes, un retournement peut se produire, exposant à un risque de piège.

-

Les stop-loss basés sur l'ATR et les plus bas/hauts peuvent être trop larges en cas de cassure exceptionnelle, augmentant les pertes.

Mesures de gestion des risques :

- Ajuster les paramètres de la moyenne mobile ou choisir un autre type de moyenne.

- Élargir la marge de stop-loss et appliquer le stop-loss rapidement.

- Ajouter un facteur multiplicateur à l'ATR ou ajuster la période de rétrospective.

Pistes d'optimisation

- Tester davantage de types d'indicateurs de moyenne mobile pour trouver les paramètres optimaux.

- Optimiser la période de l'ATR pour le stop-loss.

- Tester différents paramètres de multiple de stop-loss.

- Tester différents coefficients de risque pour le take-profit.

Résumé

Cette stratégie combine le canal SSL pour juger la tendance et les indicateurs de moyenne mobile pour confirmer les entrées, permettant un suivi de tendance efficace. Elle offre des méthodes flexibles de stop-loss et de take-profit, permettant de mieux contrôler les risques tout en maximisant les gains. Grâce à des tests et optimisations continus des paramètres, il est possible d'obtenir de meilleures performances de trading. C'est une stratégie efficace qui mérite d'être suivie et utilisée à long terme.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1