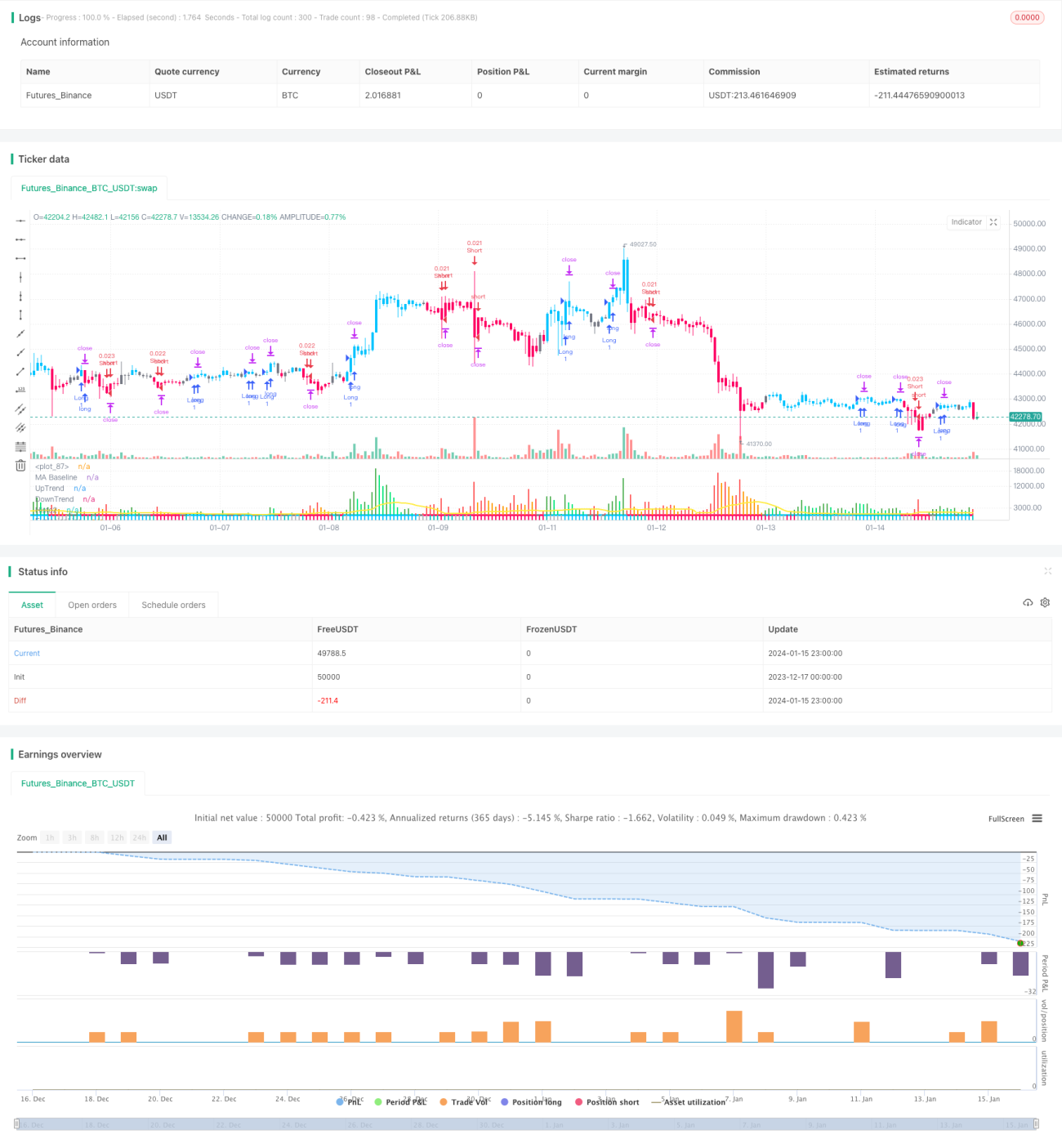

Stratégie de breakout pilotée par le sentiment et intégrant de multiples indicateurs

Aperçu

Cette stratégie intègre trois indicateurs de sentiment : l'indicateur QQE amélioré, l'indicateur hybride SSL et l'indicateur d'explosion Waddah Attar, pour générer des signaux de trading. Il s'agit d'une stratégie de breakout basée sur le sentiment, pilotée par plusieurs indicateurs. Elle est capable d'évaluer le sentiment du marché avant un breakout et d'éviter les faux signaux, ce qui en fait une stratégie de breakout de qualité supérieure.

Principe de la stratégie

La logique centrale de cette stratégie repose sur trois indicateurs pour prendre des décisions de trading :

Indicateur QQE amélioré : Cet indicateur améliore le RSI pour le rendre plus sensible, permettant d'évaluer les niveaux de sentiment du marché. La stratégie utilise cet indicateur pour détecter les signaux de retournement haussier et baissier.

Indicateur hybride SSL : Cet indicateur combine les franchissements de plusieurs moyennes mobiles pour déterminer les tendances du marché. La stratégie l'utilise pour identifier les configurations de sortie de canal.

Indicateur d'explosion Waddah Attar : Cet indicateur mesure la force de l'impulsion des prix à l'intérieur du canal. La stratégie l'utilise pour confirmer que la dynamique est suffisante lors du breakout.

Lorsque l'indicateur QQE émet un signal de retournement haussier, que l'indicateur SSL montre un franchissement de la borne supérieure du canal, et que l'indicateur Waddah Attar confirme une impulsion de momentum, la stratégie génère un signal d'achat. Lorsque les trois indicateurs émettent simultanément des signaux opposés, un signal de vente est déclenché.

La stratégie intègre également des niveaux de stop-loss et de take-profit précis pour verrouiller les gains au maximum, ce qui en fait une stratégie de breakout de haute qualité pilotée par le sentiment.

Analyse des avantages

Cette stratégie présente les avantages suivants :

- Combinaison de multiples indicateurs pour évaluer le sentiment du marché, réduisant le risque de faux breakouts.

- Prise en compte simultanée des indicateurs de retournement, de canal et de momentum, garantissant une confirmation élevée du marché lors du breakout.

- Utilisation d'un stop-loss suiveur de haute précision pour limiter les risques et verrouiller les gains.

- Paramètres optimisés après de nombreux tests, offrant une bonne stabilité adaptée aux positions de moyen à long terme.

- Possibilité de configurer les paramètres des indicateurs pour ajuster le style de la stratégie en fonction des conditions de marché.

Analyse des risques

Les principaux risques de cette stratégie sont les suivants :

- En cas de marché baissier persistant, elle peut générer un nombre important de petites transactions perdantes.

- La dépendance à plusieurs indicateurs peut entraîner des défaillances anormales dans certains marchés.

- Les multiples indicateurs comme le QQE présentent un risque de suroptimisation des paramètres, nécessitant une configuration prudente.

- Le stop-loss suiveur peut être moins efficace dans des conditions de marché particulières.

Pour atténuer ces risques, il est recommandé d'ajuster les paramètres des indicateurs pour les rendre plus stables, et d'allonger la période de détention pour améliorer le taux de profit.

Pistes d'optimisation

Cette stratégie peut être optimisée selon les axes suivants :

- Ajuster les paramètres de chaque indicateur pour les rendre plus stables ou plus réactifs.

- Ajouter un module d'optimisation de la taille des positions basé sur la volatilité.

- Intégrer un module de gestion des risques basé sur l'apprentissage automatique pour évaluer les conditions du marché en temps réel.

- Utiliser des modèles d'apprentissage profond pour prédire les configurations des indicateurs, améliorant ainsi la précision des décisions.

- Introduire une analyse multi-périodes pour réduire la probabilité de faux breakouts.

Conclusion

Cette stratégie combine efficacement les atouts de plusieurs indicateurs de sentiment courants pour construire une stratégie de breakout pilotée par le sentiment, performante et efficace. Elle évite de nombreux risques liés aux breakouts de faible qualité, tout en offrant un concept de stop-loss de haute précision pour verrouiller les gains. Il s'agit d'un ensemble de stratégies de breakout mature et fiable, digne d'être étudié et appliqué. Avec une optimisation continue des paramètres et l'introduction de modèles prédictifs, cette stratégie est susceptible de générer des rendements excédentaires plus durables et stables.

- 1