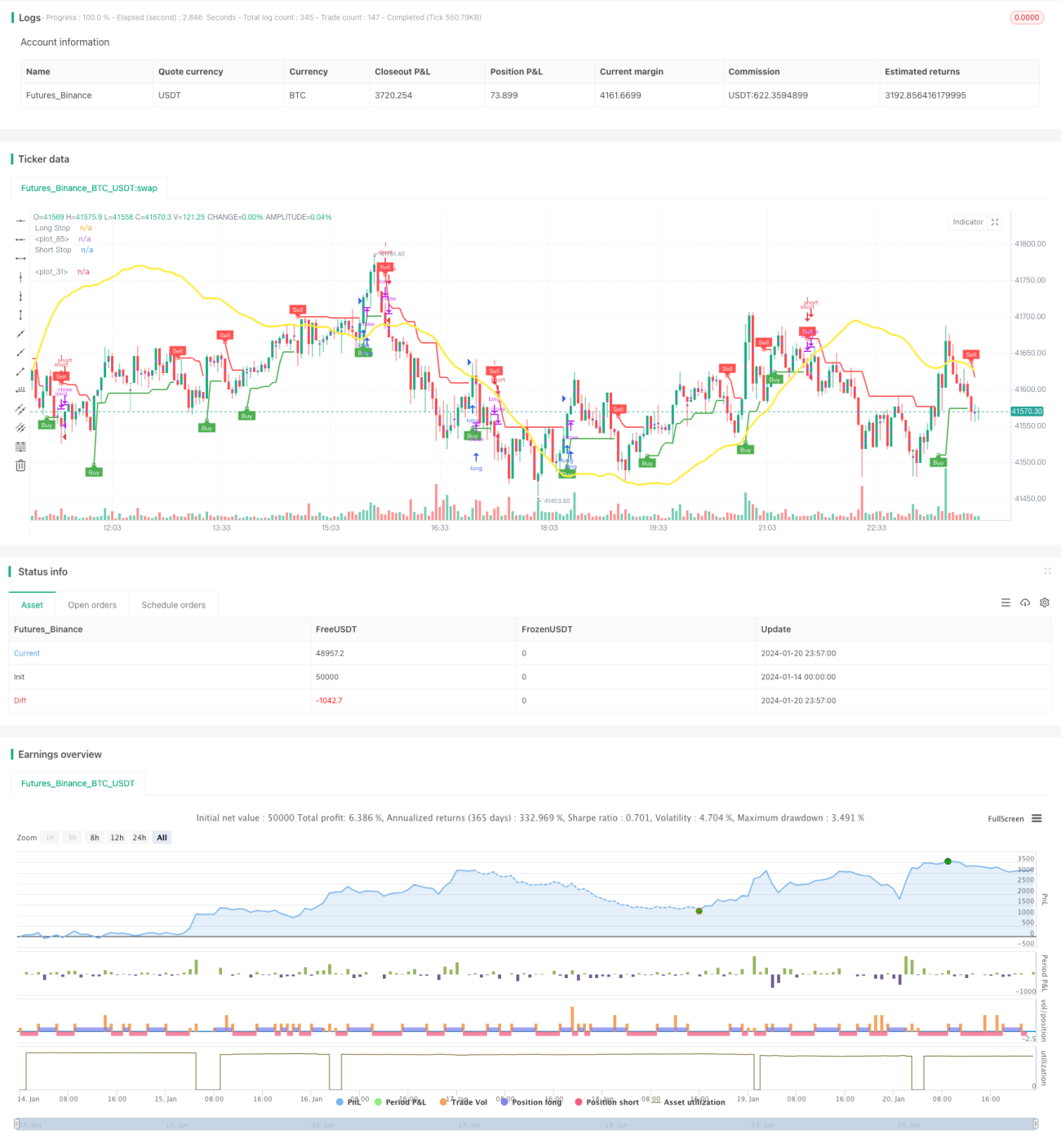

Stratégie de trading de sortie sur ligne cantilever combinée à une moyenne mobile superposée à zéro décalage

Aperçu

L'idée principale de cette stratégie consiste à combiner l'indicateur de moyenne mobile superposée à décalage nul (ZLSMA) pour déterminer la direction de la tendance, et l'indicateur de sortie en porte-à-faux (CE) pour identifier des points d'entrée et de sortie plus précis. Le ZLSMA est un indicateur de tendance qui permet de détecter précocement les changements de tendance. Le CE utilise le calcul de l'ATR pour ajuster dynamiquement les points de sortie, ce qui permet un contrôle efficace des pertes. Cette stratégie convient principalement aux opérations à court et moyen terme.

Principe de la stratégie

-

Partie ZLSMA :

- Utilisation de la méthode de régression linéaire pour calculer respectivement les lignes LMA sur une période de 130.

- Superposition des deux lignes LMA pour obtenir la différence affectée à eq.

- Enfin, ajout de la différence eq à la ligne LMA d'origine pour constituer la moyenne mobile superposée à décalage nul (ZLSMA).

-

Partie CE :

- Calcul de l'indicateur ATR, multiplié par un coefficient (par défaut 2) pour déterminer la distance dynamique par rapport au plus haut ou au plus bas récent.

- Lorsque le cours de clôture dépasse la ligne stop long ou stop short la plus récente, ajustement en conséquence de cette ligne.

- Détermination de la direction haussière ou baissière en fonction de la position du cours de clôture par rapport à la ligne de stop.

-

Moment d'entrée :

- Le ZLSMA détermine la direction de la tendance, et l'entrée se fait lorsque le CE émet un signal.

-

Sortie et stop :

- Pour les positions longues, un stop-loss fixe et un take-profit sont définis.

- Pour les positions courtes, le stop-loss fixe est remplacé par la sortie dynamique du CE.

Analyse des avantages

- Le ZLSMA permet de détecter les tendances précocement, évitant les faux signaux.

- Le CE ajuste les points de sortie de manière flexible en fonction de la volatilité du marché.

- Le ratio risque/rendement de la stratégie est personnalisable.

- L'utilisation de méthodes de stop-loss et take-profit différentes pour les positions longues et courtes permet de contrôler les risques simultanément.

Analyse des risques

- Un paramétrage inadéquat peut augmenter le taux de pertes ou élargir la plage de stop-loss.

- En cas de retournement rapide du marché, le stop-loss risque d'être franchi.

Pistes d'optimisation

- Il est possible de tester l'optimisation des paramètres sur différents marchés et périodes.

- On peut envisager d'ajuster les paramètres de take-profit et stop-loss en fonction de la volatilité ou d'un cycle spécifique.

- La combinaison avec d'autres indicateurs ou modèles peut améliorer le taux de profit.

Conclusion

Cette stratégie utilise principalement la moyenne mobile superposée à décalage nul pour déterminer la direction de la tendance, combinée à l'indicateur de sortie en porte-à-faux pour identifier des points d'entrée et de sortie plus précis. L'avantage de la stratégie réside dans la personnalisation des ratios stop-loss et take-profit, ainsi que dans l'ajustement dynamique de la sortie en porte-à-faux qui permet de contrôler le risque en fonction des conditions du marché. Les prochaines étapes pourront consister en une optimisation des paramètres et une combinaison de stratégies pour améliorer encore la stabilité et le taux de profit.

- 1