Stratégie de trading de divergence anormale du RSI

Nom de la stratégie

RSI Bullish/Bearish Divergence Trading Strategy

Aperçu

Cette stratégie utilise l'indicateur RSI pour identifier les signaux de divergence haussière et baissière, classiques et cachées, et décide de passer une position longue ou courte en fonction du signal de divergence anormal.

Principe de la stratégie

Lorsque le prix atteint un nouveau sommet mais que le RSI n'atteint pas un nouveau sommet correspondant, cela constitue une divergence haussière anormale et est considéré comme un signal de vente. À l'inverse, lorsque le prix atteint un nouveau creux mais que le RSI n'atteint pas un nouveau creux correspondant, cela constitue une divergence baissière anormale et est considéré comme un signal d'achat. La divergence classique est une divergence évidente entre le prix et le RSI, tandis que la divergence cachée est une divergence plus subtile. Les décisions d'achat ou de vente sont prises en fonction des signaux de divergence haussière et baissière, classiques et cachées.

Analyse des avantages

- Les signaux de divergence anormale ont une fiabilité élevée, avec un taux de réussite (win rate) supérieur.

- Identifie à la fois les divergences haussières et baissières classiques et cachées, couvrant un large éventail de cas.

- Les paramètres du RSI sont ajustables, ce qui permet de s'adapter à différents environnements de marché.

Analyse des risques

- Les signaux de divergence cachée présentent un risque plus élevé de fausse détection.

- Nécessite une revue manuelle pour filtrer les signaux erronés.

- L'efficacité dépend du réglage des paramètres du RSI.

Pistes d'optimisation

- Optimiser les paramètres du RSI pour trouver la meilleure combinaison.

- Ajouter des algorithmes d'apprentissage automatique pour identifier automatiquement les vrais signaux.

- Combiner davantage d'indicateurs pour valider la fiabilité des signaux.

Résumé

Cette stratégie identifie les signaux de trading de divergence anormale du RSI et décide de prendre une position longue ou courte en fonction des divergences haussières et baissières classiques et cachées, avec un taux de réussite élevé. En optimisant les paramètres du RSI et en ajoutant d'autres indicateurs de validation, l'efficacité de la stratégie peut être encore améliorée.

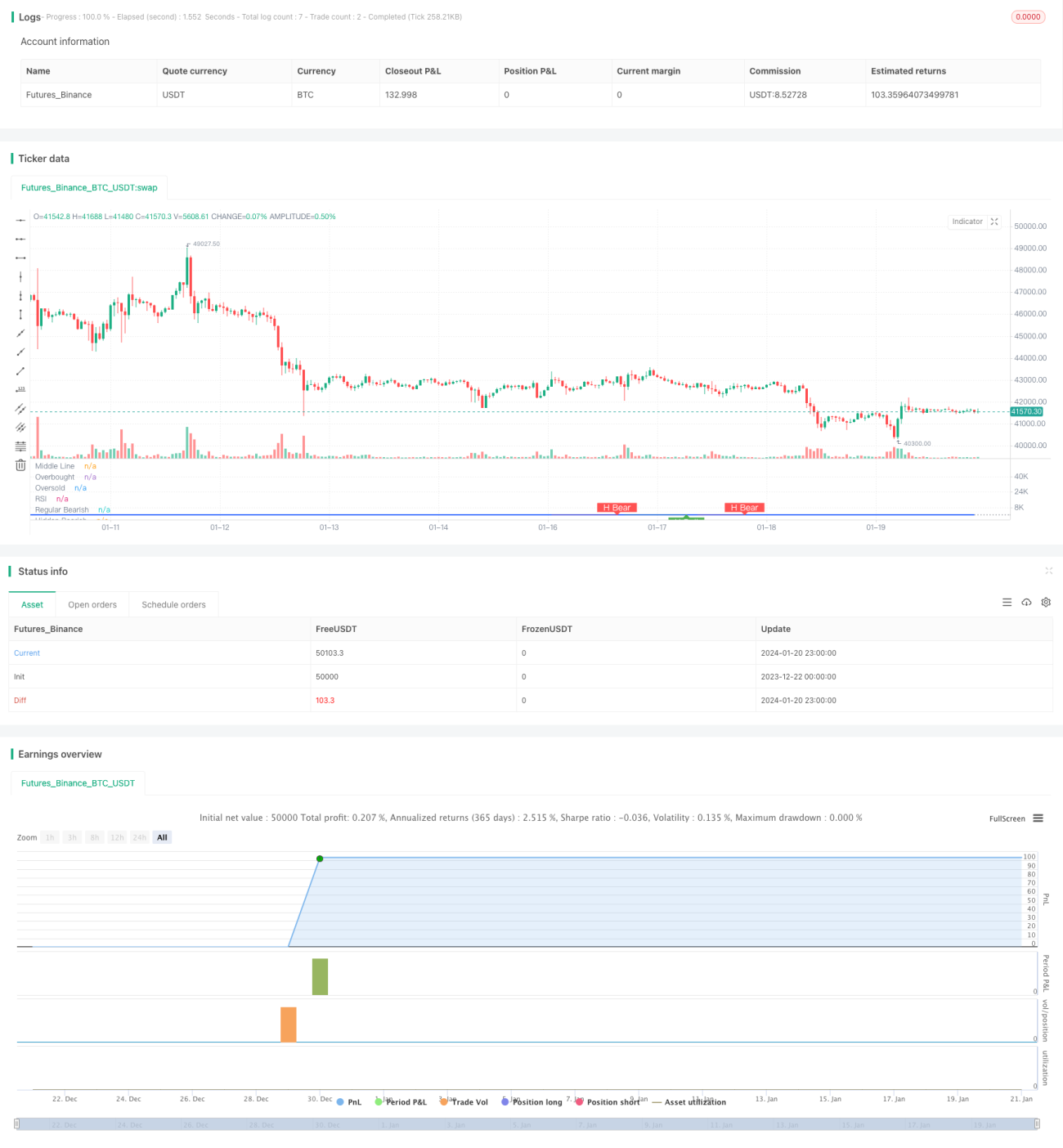

/*backtest

start: 2023-12-22 00:00:00

end: 2024-01-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Divergence Indicator")

len = input.int(title="RSI Period", minval=1, defval=14)

src = input(title="RSI Source", defval=close)- 1