Stratégie de l'indicateur Mofei de voyage dans le temps

Aperçu

Il s'agit d'une stratégie quantitative simple utilisant l'indicateur Wolfe pour identifier les « grands requins » sur le marché. Elle est conçue pour un timeframe de 5 minutes et principalement utilisée pour le trading de crypto-monnaies.

Principe de la stratégie

Cette stratégie utilise l'indicateur Wolfe avec une longueur de 3, en fixant le seuil de surachat à 100 et le seuil de survente à 0. La stratégie attend que l'indicateur Wolfe atteigne un niveau de surachat, signalant la présence d'un « grand requin » sur le marché. Si, au cours de la même journée, les deux premiers points de surachat de l'indicateur Wolfe sont suivis d'une hausse des prix, cela constitue un signal d'achat long.

Lorsque l'indicateur Wolfe = 100 et que la bougie suivante est une grande bougie haussière, on ouvre une position longue. Le stop-loss est fixé au plus bas de la session de trading, et le take-profit intervient 60 minutes après l'entrée.

Pour les positions courtes, on peut utiliser une logique symétrique : lorsque l'indicateur Wolfe atteint un niveau de survente et que la bougie suivante est une grande bougie baissière, on ouvre une position courte.

Avantages de la stratégie

- L'utilisation de l'indicateur Wolfe permet d'identifier efficacement le comportement des « grands requins » qui accumulent des actions à fort potentiel, lesquelles ont de fortes chances de continuer à monter.

- L'utilisation de la taille réelle des bougies pour repérer les points de rupture solides permet de filtrer de nombreux faux dépassements.

- L'intégration d'un filtre SMA permet d'éviter d'acheter des actions en tendance baissière, réduisant ainsi efficacement le risque de trading.

- L'approche de trading intraday ultra-court terme, avec un take-profit à 60 minutes, permet de verrouiller rapidement les profits et de réduire la probabilité de drawdown.

Risques de la stratégie

- L'indicateur Wolfe peut générer de faux signaux, entraînant des pertes inutiles. Il est possible d'ajuster les paramètres ou d'ajouter d'autres indicateurs pour filtrer.

- La méthode de trading ultra-court terme sur 60 minutes peut être trop agressive, inadaptée aux actions à forte volatilité. On peut ajuster la durée du take-profit ou utiliser un stop-loss suiveur pour optimiser.

- La stratégie ne tient pas compte de l'impact des événements macroéconomiques majeurs sur le marché. Il convient alors de suspendre la stratégie et de reprendre lorsque le marché se stabilise.

Pistes d'optimisation

- Tester différentes combinaisons de paramètres, comme ajuster la longueur de l'indicateur Wolfe ou optimiser la période du SMA.

- Essayer d'ajouter d'autres indicateurs (bandes de Bollinger, indicateur KDJ, etc.) pour améliorer la précision des signaux.

- Tester un relâchement modéré de la largeur du stop-loss pour voir si cela permet d'obtenir des gains unitaires plus importants.

- Développer des versions adaptées à d'autres timeframes (15 minutes ou 30 minutes) basées sur ce squelette de stratégie.

Résumé

Dans l'ensemble, cette stratégie est très simple et facile à comprendre. Son idée de base est cohérente avec l'approche classique de suivi des « grands requins ». En identifiant les points clés de surachat/survente de l'indicateur Wolfe et en filtrant avec les tailles réelles des bougies, on élimine beaucoup de bruit. L'ajout du filtre SMA renforce encore la stabilité de la stratégie.

L'approche de trading ultra-court terme sur 60 minutes permet de générer rapidement des profits, mais comporte également un risque opérationnel élevé. Dans l'ensemble, il s'agit d'un modèle de stratégie quantitative à forte valeur pratique, méritant une recherche et une optimisation approfondies, et nous offrant une précieuse piste de développement stratégique.

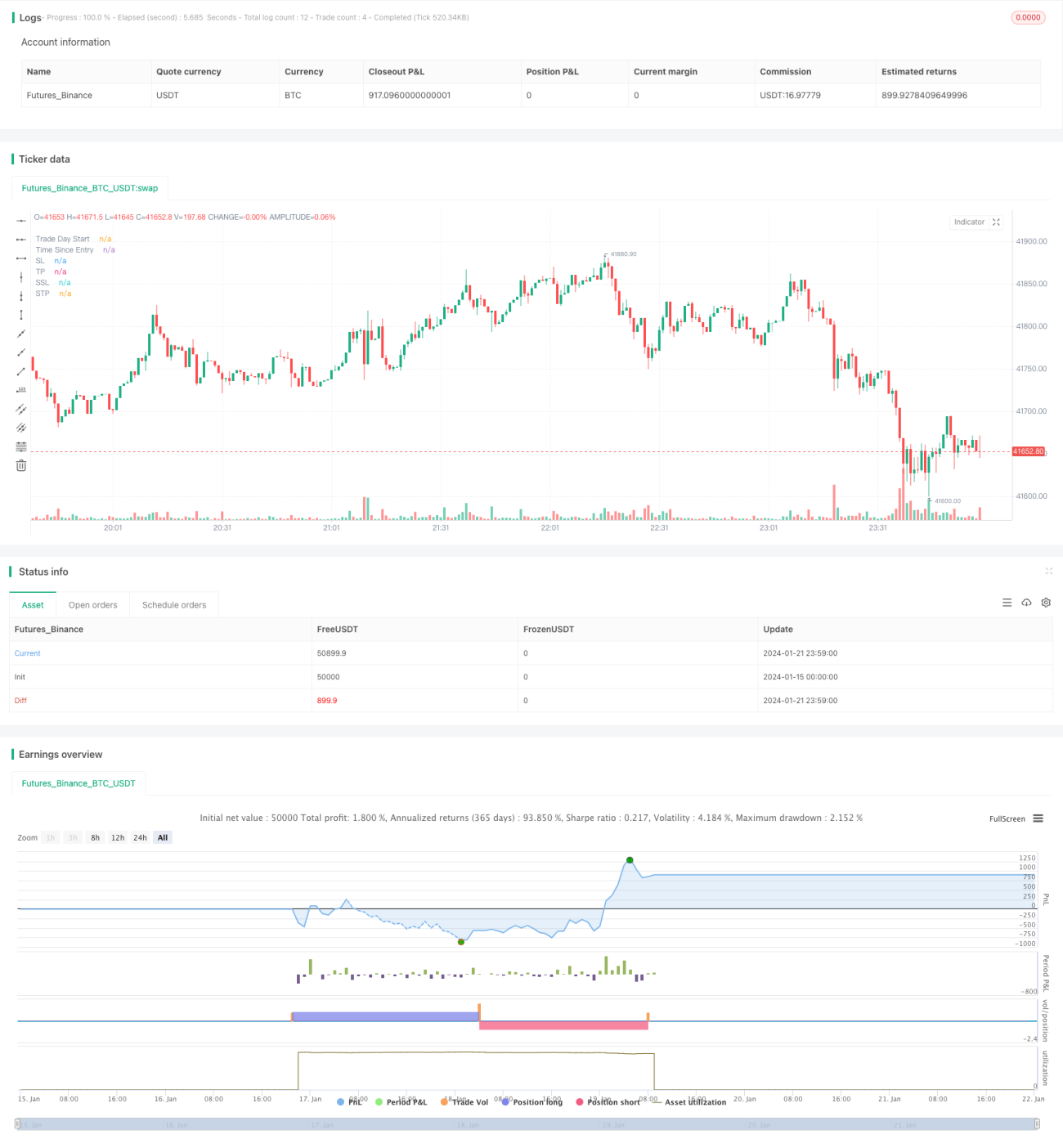

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1