Stratégie de suivi de tendance basée sur la moyenne mobile

Aperçu

Cette stratégie est une stratégie simple de suivi de tendance basée sur les moyennes mobiles. Elle compare les relations de taille entre les moyennes mobiles de différentes périodes pour déterminer la direction actuelle de la tendance ainsi que sa durée. Lorsqu'une moyenne mobile courte traverse la moyenne mobile longue de bas en haut, on prend une position longue ; lorsqu'elle la traverse de haut en bas, on prend une position courte. En outre, la stratégie fixe des points de stop-loss et de take-profit pour contrôler les risques.

Principe de la stratégie

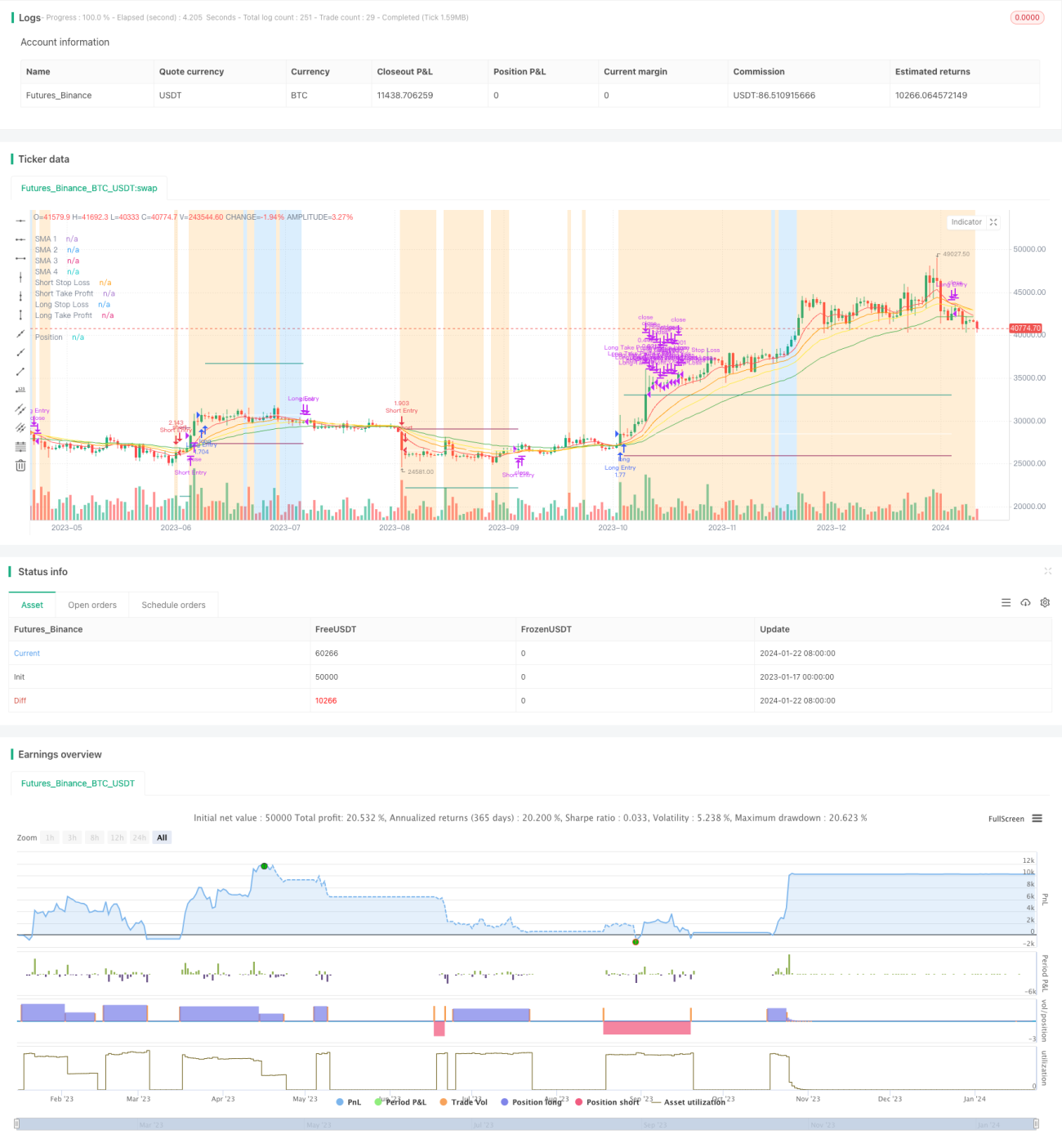

Cette stratégie utilise quatre moyennes mobiles de périodes différentes : 5 jours, 10 jours, 15 jours et 25 jours. Ces quatre moyennes mobiles sont appelées MA1, MA2, MA3 et MA4. MA1 est la plus courte, MA4 la plus longue.

Lorsque MA1 > MA2 > MA3 > MA4, cela indique que le prix est dans une tendance haussière, on prend alors une position longue. Lorsque MA1 < MA2 < MA3 < MA4, cela indique que le prix est dans une tendance baissière, on prend alors une position courte.

Les conditions d'ouverture des positions longues et courtes doivent également satisfaire le filtre de stop-loss basé sur l'ATR, c'est-à-dire que la valeur de l'ATR doit être supérieure à la moyenne mobile simple sur 40 périodes de l'ATR. Cela évite de générer de faux signaux lorsque la volatilité des prix est trop faible.

Avantages de la stratégie

Cette stratégie présente les avantages suivants :

- Concept simple et facile à mettre en œuvre.

- L'utilisation de plusieurs groupes de moyennes mobiles pour déterminer la direction de la tendance est fiable.

- La fixation de points de take-profit et de stop-loss permet de contrôler efficacement la perte maximale par transaction.

- Le filtre de stop-loss basé sur l'ATR évite de générer de faux signaux lorsque la volatilité des prix est trop faible.

Analyse des risques

Cette stratégie comporte également les risques suivants :

- Dans un marché très volatil, elle peut générer de faux signaux.

- Un réglage inapproprié des paramètres (périodes des moyennes mobiles, etc.) peut entraîner une faible efficacité de la stratégie.

- Elle ne prend pas en compte l'impact des fondamentaux et des nouvelles majeures sur les prix.

Pour réduire ces risques, on peut optimiser les paramètres de manière appropriée ou ajouter d'autres conditions de filtrage pour améliorer la stabilité de la stratégie.

Directions d'optimisation

Les directions d'optimisation de cette stratégie sont les suivantes :

- Tester différentes combinaisons de paramètres de périodes de moyennes mobiles pour trouver les meilleurs paramètres.

- Ajouter d'autres filtres d'indicateurs techniques, tels que MACD, KDJ, etc., pour évaluer la fiabilité des signaux.

- Ajouter un filtre de volume de transactions, n'effectuer des transactions que lorsque le volume augmente.

- Optimiser les paramètres par instrument en fonction des différences de paramètres spécifiques à chaque actif.

- Intégrer des algorithmes d'apprentissage automatique pour évaluer les signaux.

Résumé

Dans l'ensemble, cette stratégie est une stratégie de suivi de tendance relativement simple, qui détermine la direction de la tendance à l'aide de moyennes mobiles et définit des stop-loss et take-profit raisonnables pour contrôler le niveau de risque. La marge d'optimisation de cette stratégie est encore grande ; en ajustant les paramètres et en ajoutant des filtres, on peut encore améliorer sa stabilité et sa rentabilité.

- 1