Stratégie de trading oscillant entre supports et résistances

Aperçu

Cette stratégie combine le RSI, la croisée des stochastiques et une optimisation du slippage de clôture pour parvenir à un contrôle précis de la logique de trading et à un stop loss et take profit précis. Par ailleurs, en introduisant une optimisation des signaux, elle permet de mieux maîtriser la tendance et de gérer le capital de manière rationnelle.

Principe de la stratégie

- L'indicateur RSI détermine les zones de surachat et de survente, combiné aux croisements dorés et morts des valeurs K et D du stochastique pour former des signaux de trading.

- Introduction de l'identification des formes de bougies pour aider à juger les signaux de tendance et éviter les trades erronés.

- La moyenne mobile SMA aide à déterminer la direction de la tendance. Lorsque la moyenne mobile courte franchit à la hausse la moyenne mobile longue, c'est un signal haussier.

- Stratégie de slippage de clôture : fixer les prix de stop loss et take profit en fonction de la plage de fluctuation du plus haut et du plus bas.

Analyse des avantages

- Optimisation des paramètres du RSI pour bien déterminer les zones de surachat/survente et éviter les trades erronés.

- Optimisation des paramètres du stochastique (STO) : le réglage du paramètre de lissage permet de filtrer le bruit et d'améliorer la qualité des signaux.

- Introduction de l'analyse technique Heikin-Ashi pour identifier les changements de direction des corps de bougies, garantissant l'exactitude des signaux de trading.

- La moyenne mobile SMA aide à juger la direction de la tendance principale, évitant les trades à contre-tendance.

- Combinée à la stratégie de slippage pour le take profit et le stop loss, elle permet de verrouiller au maximum les profits de chaque trade.

Analyse des risques

- Lorsque le marché général baisse continuellement, le capital est exposé à un risque important.

- La fréquence des trades peut être trop élevée, augmentant les coûts de transaction et les coûts de slippage.

- L'indicateur RSI peut produire de faux signaux ; il convient de les filtrer avec d'autres indicateurs.

Optimisation de la stratégie

- Ajuster les paramètres du RSI pour optimiser les jugements de surachat/survente.

- Ajuster les paramètres du stochastique (STO) : lissage et période, pour améliorer la qualité des signaux.

- Ajuster les périodes des moyennes mobiles pour optimiser la détection des tendances.

- Introduire davantage d'indicateurs techniques pour améliorer la précision du jugement des signaux.

- Optimiser les ratios stop loss/take profit pour réduire le risque par trade.

Résumé

Cette stratégie intègre les avantages de plusieurs indicateurs techniques populaires. Grâce à l'optimisation des paramètres et à l'amélioration des règles, elle parvient à équilibrer la qualité des signaux de trading et la gestion du stop loss/take profit. Elle offre une certaine polyvalence et une capacité de profit stable. En l'optimisant continuellement, on peut encore améliorer le taux de réussite et la rentabilité.

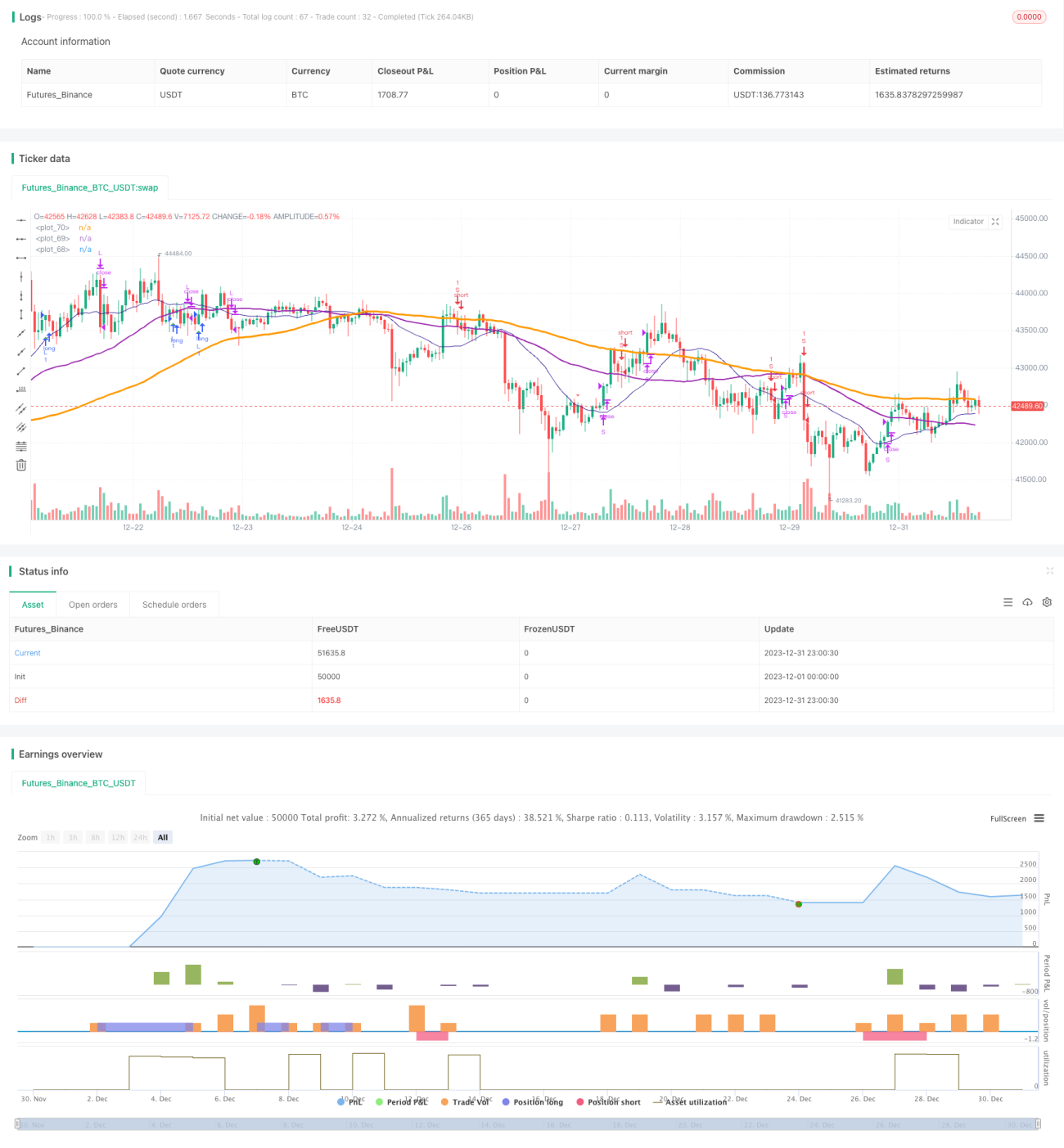

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)- 1