Stratégie de capture des points bas basée sur la régression linéaire corrigée par le VIX

Aperçu

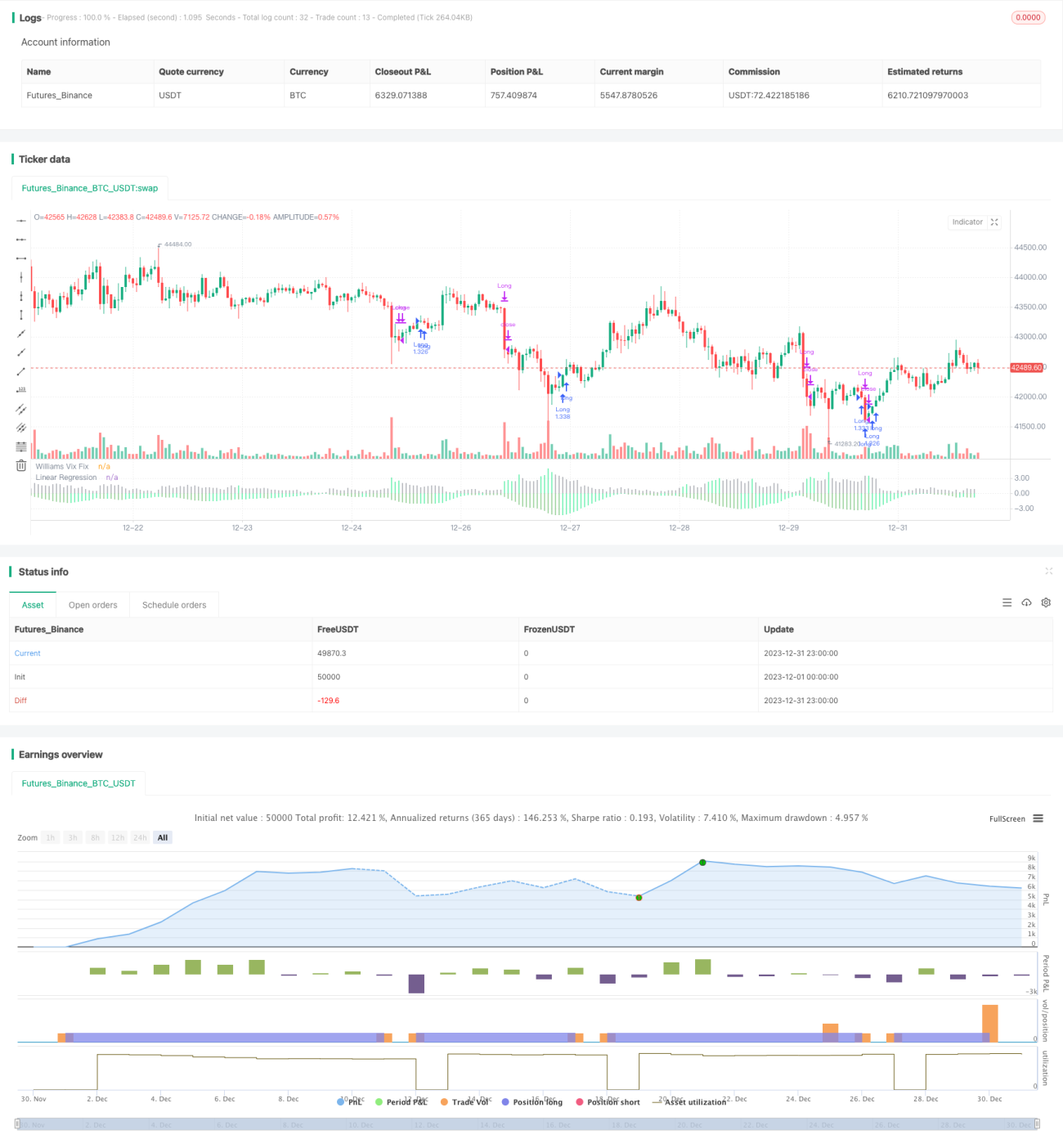

L'idée centrale de cette stratégie est de combiner l'indicateur de réparation VIX (Vix Fix) et sa régression linéaire pour capturer précisément les points bas du marché. La stratégie est nommée « Stratégie de régression linéaire des points bas de réparation ».

Principe de la stratégie

- Calculer l'indicateur de réparation VIX, qui permet de bien identifier les points bas du marché.

- Appliquer une régression linéaire à l'indicateur de réparation VIX. Lorsque l'histogramme de la régression linéaire devient vert, cela indique que la régression linéaire de la réparation VIX commence à augmenter, ce qui peut générer un signal d'achat.

- Combiner avec les barres vertes de l'indicateur de réparation VIX pour confirmer davantage le moment d'achat.

- Lorsque l'histogramme de la régression linéaire devient rouge, cela indique que la régression linéaire de la réparation VIX commence à baisser, générant un signal de vente.

Ce processus utilise la régression linéaire pour améliorer la précision et la rapidité des signaux de l'indicateur de réparation VIX, en filtrant une partie des faux signaux, permettant ainsi de capter précisément les points bas.

Analyse des avantages

- La stratégie utilise la régression linéaire pour filtrer certains faux signaux de l'indicateur de réparation VIX, rendant les signaux d'achat/vente plus précis et fiables.

- La régression linéaire augmente la sensibilité et la rapidité des signaux, permettant de détecter rapidement les points de retournement du marché.

- La logique de la stratégie est simple et claire, facile à comprendre et à mettre en œuvre, adaptée au trading quantitatif.

- Plusieurs paramètres sont configurables, ce qui permet un ajustement flexible en fonction des évolutions du marché.

Risques et solutions

- Cette stratégie est principalement utilisée pour déterminer les points bas globaux du marché, elle ne convient pas aux actions individuelles.

- La régression linéaire ne filtre pas complètement les faux signaux ; la combinaison avec l'indicateur de réparation VIX permet de réduire le risque.

- Il est nécessaire d'ajuster les paramètres de manière appropriée pour s'adapter aux changements de marché et éviter une perte d'efficacité.

- Il est recommandé de combiner avec d'autres indicateurs pour confirmer davantage les signaux.

Pistes d'optimisation

- On peut envisager de combiner avec des indicateurs de volatilité ou de volume pour filtrer davantage les signaux.

- On peut étudier des méthodes d'optimisation adaptative des paramètres pour rendre la stratégie plus intelligente.

- On peut explorer des méthodes d'apprentissage automatique avec des modèles plus complexes pour prédire l'évolution de la réparation VIX.

- On peut tenter d'appliquer des méthodes similaires sur des actions individuelles pour étudier comment filtrer les faux signaux.

Résumé

Cette stratégie utilise l'indicateur de réparation VIX pour identifier les points bas tout en introduisant une régression linéaire pour améliorer la qualité des signaux, permettant ainsi une capture efficace des points bas du marché. La stratégie est simple et pratique, avec des résultats plutôt satisfaisants. Le risque principal réside dans le fait que les faux signaux ne sont pas complètement filtrés. Nous devons encore optimiser les réglages des paramètres et envisager d'introduire d'autres moyens pour confirmer davantage les signaux, afin de perfectionner la stratégie. Dans l'ensemble, cette stratégie offre une nouvelle voie efficace pour déterminer les points bas du marché et mérite d'être étudiée plus avant.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1