Stratégie de suivi de momentum multi-timeframes

Vue d'ensemble

Cette stratégie combine l'inversion 123 et l'indicateur MACD pour effectuer un suivi de momentum sur plusieurs périodes de temps. L'inversion 123 identifie les points de retournement à court terme, tandis que le MACD détermine la tendance à moyen et long terme. Leur association permet de générer des signaux long/short en verrouillant la tendance de moyen/long terme tout en captant les retournements de court terme.

Principe de la stratégie

La stratégie se compose de deux parties :

-

Partie inversion 123 : lorsque les deux dernières bougies forment un haut/bas et que l'oscillateur stochastique est inférieur/supérieur à 50, un signal d'achat/vente est généré.

-

Partie MACD : un croisement haussier (ligne rapide au-dessus de la ligne lente) génère un signal d'achat, un croisement baissier génère un signal de vente.

Enfin, les deux sont combinés : un signal final n'est émis que lorsque l'inversion 123 et le MACD indiquent la même direction.

Avantages

Cette stratégie combine les retournements à court terme avec la tendance de moyen/long terme, ce qui permet d'obtenir un taux de réussite plus élevé en verrouillant la tendance à moyen/long terme malgré les fluctuations court terme. En particulier dans les marchés en range, l'inversion 123 permet de filtrer une partie du bruit, améliorant ainsi la stabilité.

De plus, en ajustant les paramètres, on peut équilibrer la proportion entre signaux de retournement et signaux de tendance pour s'adapter à différents environnements de marché.

Risques

Cette stratégie présente un certain décalage temporel, surtout lorsqu'on utilise un MACD à longue période, ce qui peut faire manquer des mouvements de court terme. De plus, les signaux de retournement comportent par nature une part d'aléatoire, ce qui expose au risque d'être piégé.

Il est possible de réduire la période du MACD ou d'ajouter un stop-loss pour maîtriser le risque.

Pistes d'optimisation

La stratégie peut être optimisée dans les directions suivantes :

-

Ajuster les paramètres de l'inversion 123 pour améliorer l'efficacité des retournements.

-

Ajuster les paramètres du MACD pour améliorer le jugement de tendance.

-

Ajouter d'autres indicateurs auxiliaires pour filtrer et améliorer la performance.

-

Intégrer une stratégie de stop-loss pour contrôler le risque.

Conclusion

Cette stratégie intègre plusieurs paramètres et indicateurs techniques sur différents horizons temporels, en combinant les avantages du trading de retournement et du trading de tendance grâce à un suivi de momentum multi-périodes. Elle peut être équilibrée par des réglages de paramètres et enrichie par l'ajout d'autres indicateurs ou d'un stop-loss, ce qui en fait une approche très prometteuse.

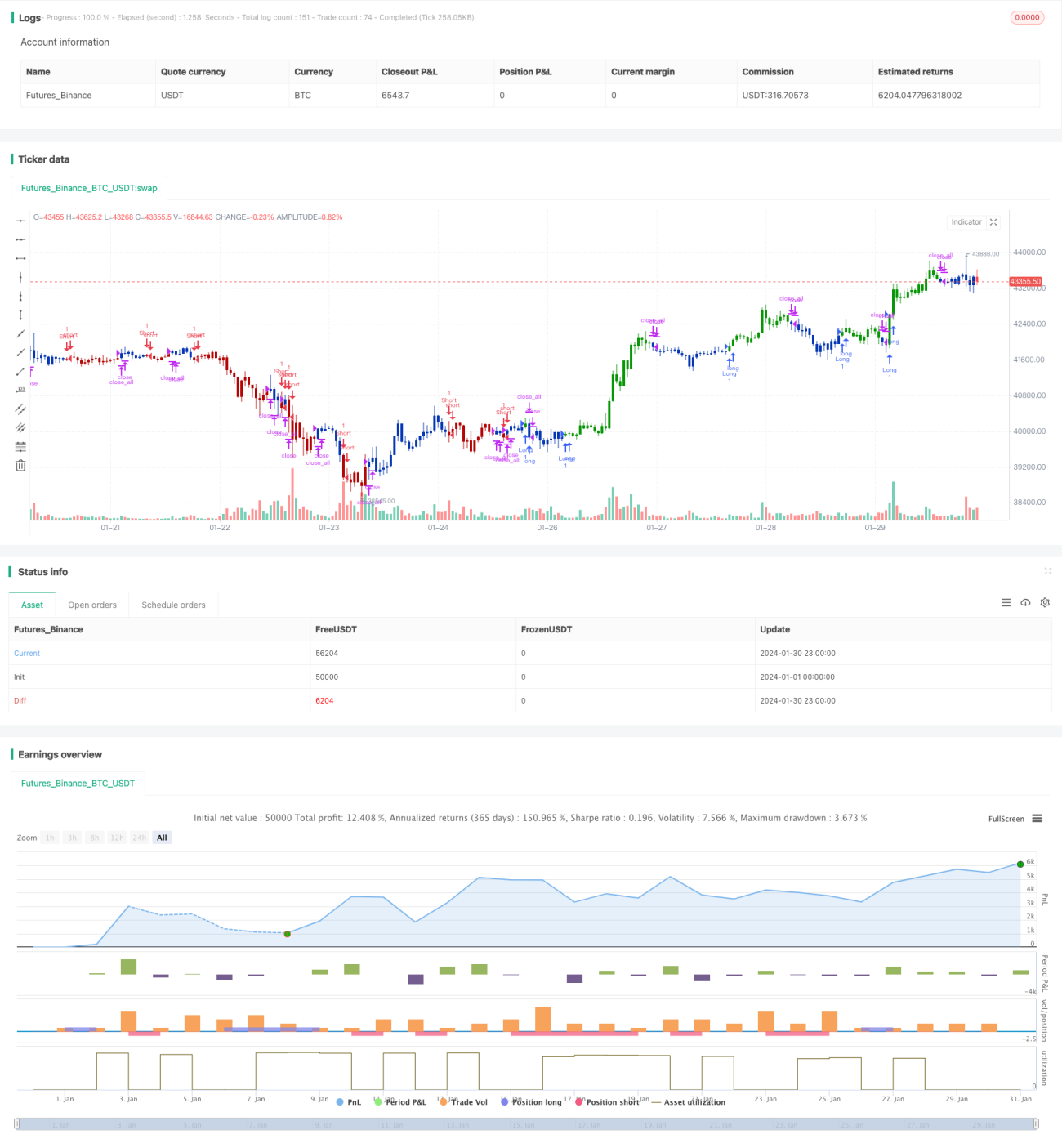

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/01/2021

// This is combo strategies for get a cumulative signal. - 1