Stratégie de bandes de Bollinger avec stop-loss dynamique

Aperçu

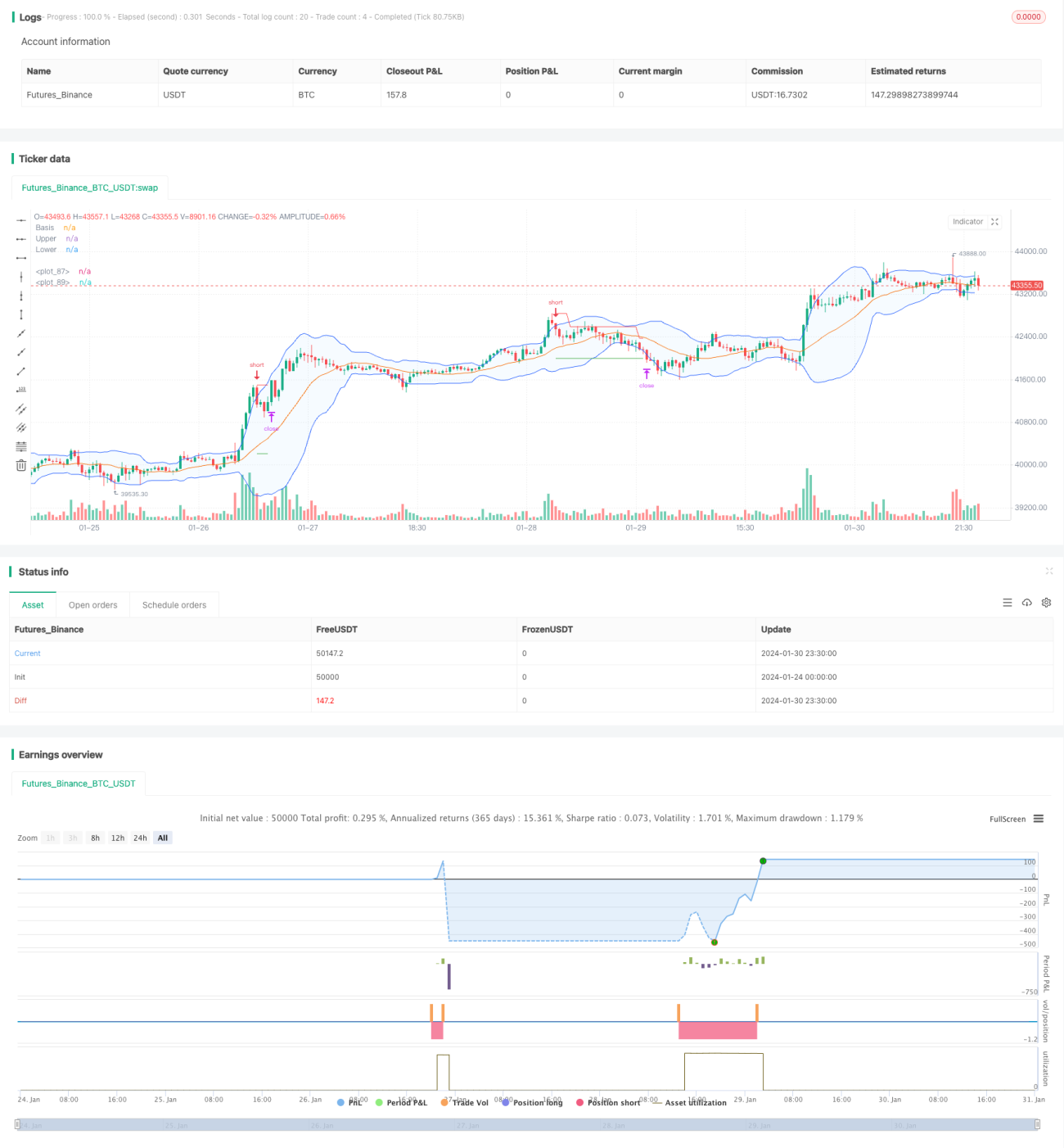

Cette stratégie utilise les bandes de Bollinger (bandes supérieure et inférieure) pour réaliser un stop-loss dynamique. Lorsque le prix franchit la bande supérieure, une position courte est ouverte ; lorsqu'il franchit la bande inférieure, une position longue est ouverte, avec un stop-loss dynamique qui suit l'évolution du prix.

Principe

Le cœur de cette stratégie repose sur les bandes supérieure et inférieure des bandes de Bollinger. La bande médiane est la moyenne mobile sur n jours, la bande supérieure correspond à la bande médiane + k * écart-type sur n jours, et la bande inférieure à la bande médiane - k * écart-type sur n jours. Lorsque le prix rebondit à partir de la bande inférieure, une position longue est prise ; lorsqu'il redescend depuis la bande supérieure, une position courte est prise. Parallèlement, la stratégie définit un niveau de stop-loss, qui est ajusté dynamiquement au fur et à mesure de l'évolution du prix, ainsi qu'un niveau de take-profit, afin d'assurer un contrôle prudent des risques.

Avantages

- Exploite la forte propriété de retour à la moyenne des bandes de Bollinger pour capturer les tendances à moyen et long terme.

- Signaux clairs pour les positions longues et courtes, faciles à exécuter.

- Stop-loss dynamique avec glissement pour verrouiller au maximum les profits et contrôler les risques.

- Paramètres ajustables en fonction du marché, adaptables à différentes conditions.

Risques et solutions

- Dans les marchés en range, les bandes de Bollinger peuvent générer plusieurs signaux d'achat et de vente, ce qui expose à des pièges. Solution : définir correctement les niveaux de stop-loss pour limiter les pertes unitaires.

- Un mauvais réglage des paramètres peut réduire le taux de réussite. Solution : optimiser les paramètres de manière adaptée à chaque instrument.

Pistes d'optimisation

- Optimiser les paramètres de la moyenne mobile pour les adapter aux caractéristiques de l'instrument.

- Ajouter un filtre de tendance pour éviter les marchés en range.

- Combiner avec d'autres indicateurs comme filtres pour améliorer la stabilité de la stratégie.

Résumé

Cette stratégie exploite la propriété de retour à la moyenne des bandes de Bollinger, associée à un stop-loss dynamique avec glissement, pour obtenir des profits de tendance à moyen et long terme tout en contrôlant les risques. C'est une stratégie quantitative très adaptative et stable. Grâce à l'optimisation des paramètres et des règles, elle peut s'adapter à davantage d'instruments et générer des gains stables en trading réel.

/*backtest

start: 2024-01-24 00:00:00

end: 2024-01-31 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(shorttitle="BB Strategy", title="Bollinger Bands Strategy", overlay=true)

length = input.int(20, minval=1, group = "Bollinger Bands")

maType = input.string("SMA", "Basis MA Type", options = ["SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA"], group = "Bollinger Bands")- 1