Stratégie de swing trading à trois moyennes mobiles : analyser patiemment les informations précieuses contenues dans les bougies

Aperçu

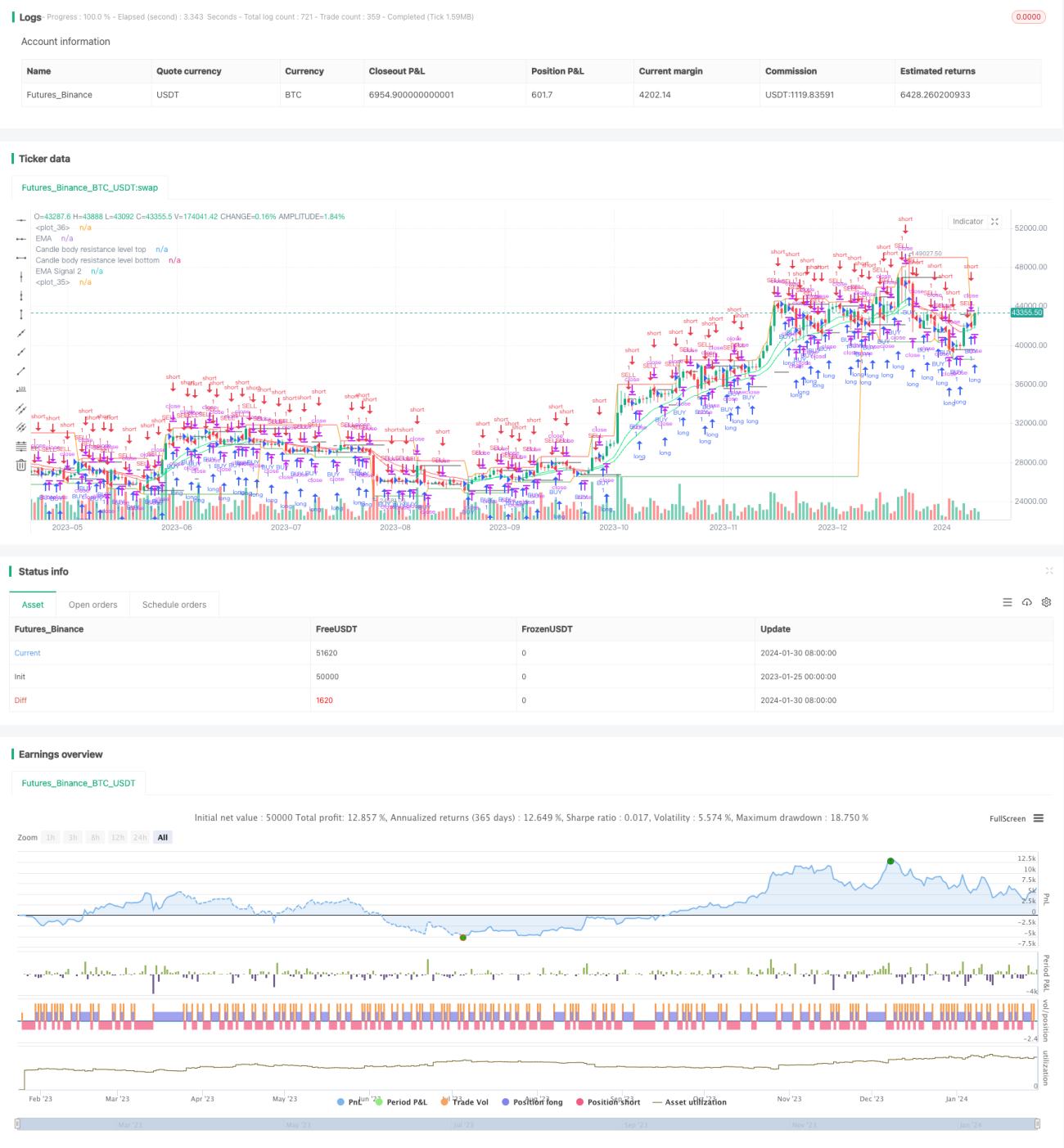

La stratégie de bandes à triple moyenne mobile utilise plusieurs indicateurs de moyenne mobile pour analyser en profondeur les chandeliers et découvrir les régularités cachées dans les fluctuations de prix, permettant ainsi des transactions d'arbitrage à faible risque.

Principe de la stratégie

Cette stratégie superpose plusieurs groupes d'indicateurs EMA sur la base des bandes de Bollinger, construit des canaux de prix et identifie les régularités des fluctuations de prix. Plus précisément :

- Utiliser l'indicateur BodyResistanceChannel pour tracer les niveaux de résistance du corps des chandeliers.

- Utiliser l'indicateur Support/Résistance pour tracer les supports et résistances sur plusieurs jours.

- Utiliser un système à double EMA pour déterminer la direction de la tendance des prix.

- Utiliser l'indicateur de moyenne mobile Hull pour lisser la courbe des prix.

Sur cette base, la stratégie combine la reconnaissance de figures pour détecter les opportunités de retournement et élaborer une stratégie d'arbitrage.

Analyse des avantages

Cette stratégie présente les avantages suivants :

- L'utilisation de multiples EMA pour construire un canal de prix permet de déterminer clairement la direction des fluctuations de prix.

- L'application de la moyenne mobile Hull permet de lisser efficacement les jugements de cassure de prix.

- La combinaison de figures de retournement et d'indicateurs de canal permet des transactions à haute probabilité et à faible risque.

- La construction d'un système d'indicateurs multi-couches offre des signaux de trading stables et fiables.

Analyse des risques

Cette stratégie comporte également les risques suivants :

- Risque de pertes importantes en cas de rupture du canal de prix. Solution ciblée : utiliser un stop suiveur pour réduire la perte par transaction.

- Risque de signaux erronés en cas de mauvaise identification des figures de retournement. Solution ciblée : optimiser les paramètres pour améliorer la précision de reconnaissance des figures.

- Risque de dégradation de la qualité des signaux de trading en raison d'une inadéquation des paramètres des indicateurs. Solution ciblée : effectuer des tests d'optimisation sur plusieurs combinaisons de paramètres.

Axes d'optimisation

Les principaux axes d'optimisation de cette stratégie sont :

- Optimiser la combinaison des périodes EMA pour mieux adapter l'indicateur aux caractéristiques du marché.

- Ajuster la position du stop pour minimiser le risque de perte par transaction tout en garantissant la rentabilité.

- Ajouter un module d'ajustement dynamique de la taille de la position basé sur la volatilité pour contrôler efficacement le risque.

- Utiliser des techniques d'apprentissage profond pour découvrir davantage de régularités de prix et améliorer la qualité des signaux.

Conclusion

La stratégie de bandes à triple moyenne mobile explore en profondeur les régularités des fluctuations de prix, stable et efficace, méritant une application à long terme et une optimisation continue. Investir exige rationalité et patience ; trader progressivement est la clé du succès.

- 1