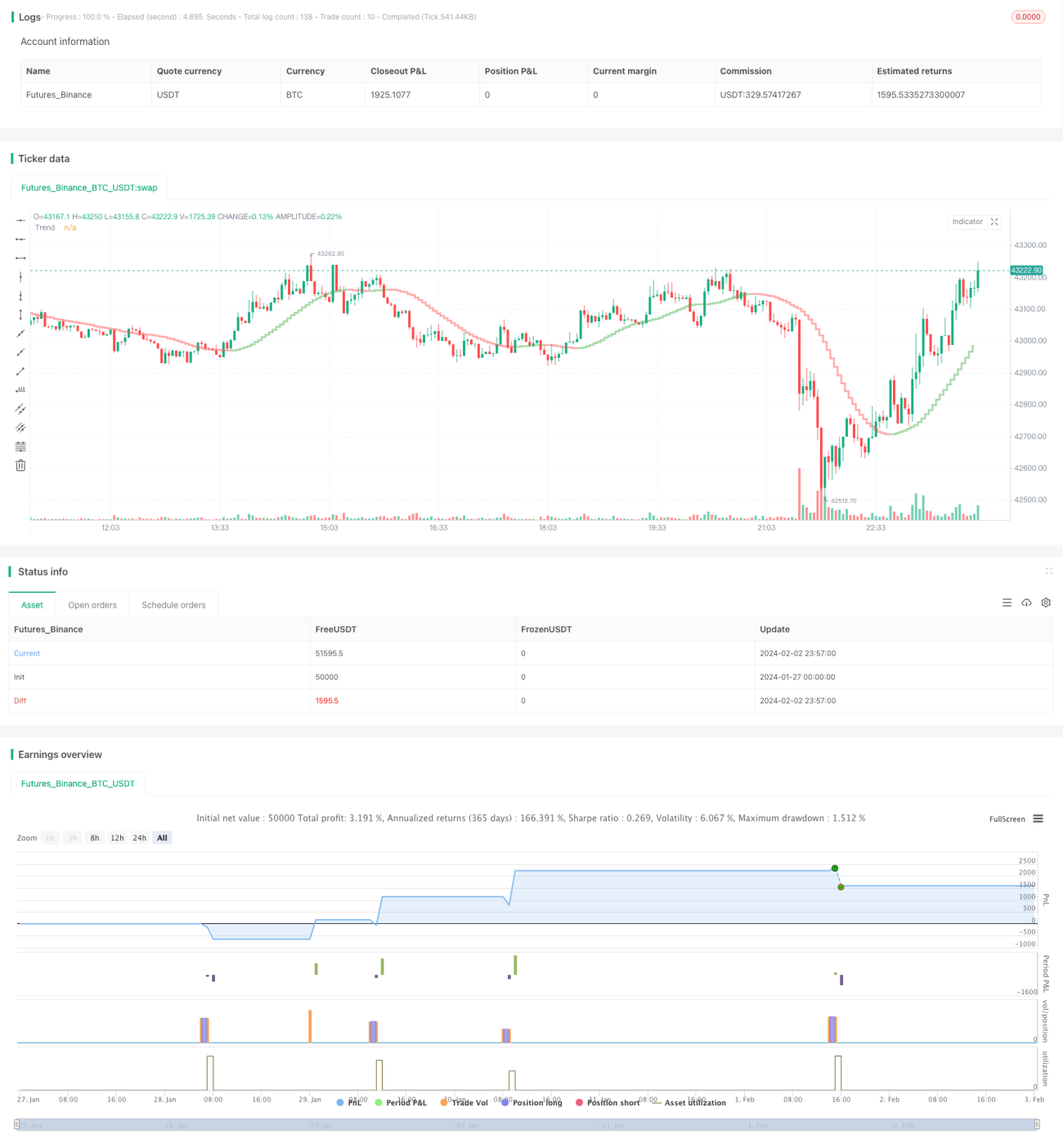

Stratégie Ripple basée sur l'indicateur Coral Trend dans l'intervalle de backtest

Aperçu

Cette stratégie utilise l'indicateur Coral Trend de LazyBear pour déterminer la direction de la tendance des prix, en identifiant les inversions de direction de l'indicateur Coral Trend afin de repérer les points d'entrée potentiels. Pour filtrer les faux signaux de rupture, la stratégie combine l'indicateur ADX ou l'Absolute Strength Histogram avec l'indicateur HawkEye Volume comme confirmation, garantissant des entrées plus fiables.

Le mécanisme de sortie utilise le plus haut ou le plus bas des N dernières barres, multiplié par un ratio risque/rendement configurable, pour définir les niveaux de stop-loss et de take-profit.

Principe de la stratégie

Après avoir déterminé la direction générale de la tendance à l'aide de l'indicateur Coral Trend, lorsque la couleur de l'indicateur reste inchangée, le prix effectue un petit repli (pullback) dans la direction opposée. Si, à la fin de ce repli, le prix revient dans la direction de la tendance principale indiquée par le Coral Trend, cela peut être considéré comme un bon moment d'entrée.

Les conditions d'entrée incluent :

-

La direction de l'indicateur Coral Trend est alignée avec la direction de la transaction (long = vert, short = rouge).

-

Depuis le dernier franchissement complet du Coral Trend par le prix (le haut de la dernière barre dépasse la ligne Coral Trend), il y a eu au moins 1 barre dont le bas est entièrement au-dessus du Coral Trend (pour une position longue) ou dont le haut est entièrement en dessous du Coral Trend (pour une position courte).

-

Un petit repli dans la direction opposée se produit : pendant ce repli, le cours de clôture reste du côté opposé au Coral Trend.

-

Après la fin du petit repli, le cours de clôture revient dans la direction de la tendance principale indiquée par le Coral Trend.

Ces conditions sont principales. En parallèle, la stratégie utilise l'indicateur ADX ou la combinaison de l'Absolute Strength Histogram et du HawkEye Volume comme confirmation d'entrée.

Pour l'ADX, il faut que sa valeur soit > 20 et que la dernière barre soit en hausse. De plus, l'ordre des lignes DI verte et rouge doit être cohérent avec la direction de la transaction.

Pour l'Absolute Strength Histogram, sa couleur doit correspondre à la direction de la transaction (long = bleu, short = rouge). Le HawkEye Volume doit également avoir une couleur cohérente (long = vert, short = rouge).

Le mécanisme de sortie utilise le plus haut ou le plus bas des N dernières barres, multiplié par un ratio risque/rendement pour définir les niveaux de stop-loss et de take-profit. Les valeurs N et le ratio sont paramétrables.

Analyse des avantages

Le principal avantage de cette stratégie est qu'elle utilise l'indicateur Coral Trend pour déterminer la direction principale de la tendance, puis identifie les opportunités d'entrée grâce à ses inversions, évitant ainsi de suivre la tendance dans un marché non directionnel. De plus, l'utilisation d'indicateurs de confirmation permet de filtrer de nombreux faux signaux de rupture, augmentant ainsi le taux de réussite des entrées.

En outre, la stratégie offre un mécanisme de gestion des risques complet, incluant le réglage de l'amplitude du stop-loss et le contrôle du pourcentage d'exposition au risque, ce qui garantit que même en cas de pertes individuelles, l'impact global sur le capital reste limité.

Analyse des risques

Le principal risque de cette stratégie réside dans l'utilisation d'indicateurs pour les décisions d'entrée, ce qui peut donner l'illusion qu'une configuration entièrement automatisée des paramètres suffit à générer des profits. En réalité, l'optimisation des paramètres et la configuration des règles doivent être basées sur les lois sous-jacentes des mouvements de prix, et il est nécessaire d'évaluer visuellement l'interaction entre les indicateurs et les prix pour obtenir une configuration adaptée à son propre style de trading et aux actifs négociés.

De plus, le réglage des niveaux de stop-loss et de take-profit doit être approprié : un ratio de take-profit trop élevé peut empêcher la sortie, tandis qu'un stop-loss trop serré expose à un risque excessif. Ces ajustements doivent tenir compte de la volatilité de chaque actif et de la tolérance au risque de l'utilisateur.

Pistes d'optimisation

Les axes d'optimisation possibles pour cette stratégie incluent :

-

Ajuster les paramètres de l'indicateur Coral Trend pour le rendre plus réactif aux variations de prix des différents actifs.

-

Expérimenter différents indicateurs de confirmation ou combinaisons d'indicateurs, tels que KDJ, MACD, etc., afin d'améliorer la précision des signaux d'entrée.

-

Adapter le calcul des niveaux de stop-loss et de take-profit en fonction de la volatilité de chaque actif pour une meilleure gestion des risques.

-

Ajouter un module de gestion de capital permettant d'ajuster la taille des ordres en fonction du nombre de positions, afin de limiter efficacement les pertes globales.

-

Ajouter un module de contrôle des horaires de trading, permettant à la stratégie de ne fonctionner que pendant certaines périodes, évitant ainsi les pertes dues à une volatilité excessive.

Conclusion

Cette stratégie utilise d'abord le Coral Trend pour déterminer la tendance à moyen/long terme des prix, puis, en détectant ses inversions et en utilisant des signaux de confirmation pour filtrer les faux signaux de rupture, elle construit une stratégie de suivi de tendance relativement fiable. De plus, une gestion des risques bien conçue permet à la stratégie de fonctionner sur le long terme avec un capital stable. Grâce à une optimisation supplémentaire des paramètres et des modules, cette stratégie pourrait s'adapter à davantage d'actifs, offrant ainsi une meilleure stabilité et une rentabilité accrue.

- 1