Stratégie de retournement de tendance sur trois bougies

Aperçu

La stratégie de tendance par retournement à trois bougies (Three Candle Reversal Trend Strategy) est une stratégie de trading à court terme qui identifie trois bougies consécutives haussières ou baissières, suivies d'une bougie englobante pour déterminer le retournement de tendance à court terme, en combinant plusieurs indicateurs techniques pour filtrer les points d'entrée. La stratégie utilise un ratio stop-loss/ take-profit de 1:3 pour obtenir des rendements excédentaires.

Principe de la stratégie

La logique centrale de cette stratégie est d'identifier une configuration de trois bougies consécutives haussières ou baissières, qui annonce généralement un retournement de tendance à court terme. Après avoir détecté trois bougies baissières, on attend une bougie haussière englobante pour entrer en position longue ; inversement, après trois bougies haussières, on attend une bougie baissière englobante pour entrer en position courte. Cela permet de saisir rapidement les opportunités de retournement de tendance à court terme.

De plus, la stratégie intègre plusieurs indicateurs techniques pour filtrer les points d'entrée. Elle utilise deux moyennes mobiles simples (SMA) avec des paramètres différents, et n'envisage une entrée que lorsque la moyenne rapide croise la moyenne lente. Un indicateur de régression linéaire permet de déterminer si le marché est en range ou en tendance ; les transactions ne sont effectuées qu'en condition de tendance. La stratégie propose également un interrupteur pour décider si l'on souhaite combiner la configuration de bougies avec un croisement doré des moyennes mobiles. Grâce à cette combinaison d'indicateurs, la plupart du bruit est filtré, améliorant la précision des entrées.

En ce qui concerne le stop-loss et le take-profit, la stratégie exige un ratio risque/rendement d'au moins 1:3. Le stop-loss est défini en calculant l'ATR (Average True Range) sur les N dernières bougies, combiné à un pourcentage de volatilité, puis le niveau de take-profit est déterminé en conséquence. Cela permet d'obtenir un rendement excédentaire approprié tout en prenant un risque mesuré.

Avantages de la stratégie

La stratégie de tendance par retournement à trois bougies présente les avantages suivants :

- Identifie les points de retournement de tendance à court terme pour saisir les opportunités rapidement.

- Filtre multiple par indicateurs, améliorant la précision des entrées.

- Mécanisme de stop-loss/take-profit raisonnable avec un ratio risque/rendement équilibré.

- Paramètres simples, faciles à comprendre et à mettre en œuvre.

Risques de la stratégie

Cette stratégie comporte également certains risques à prendre en compte :

- Un retournement à court terme ne représente pas forcément un retournement de tendance à long terme ; il convient de surveiller les tendances sur des horizons temporels plus élevés. On peut ajouter une moyenne mobile de plus longue période comme filtre.

- Les signaux basés sur une configuration unique de bougies peuvent être erronés ; on peut envisager d'ajouter d'autres signaux de confirmation auxiliaires.

- Le niveau de stop-loss peut être trop optimiste ; on peut resserrer la plage de stop-loss.

- Les données de backtest sont limitées, ce qui introduit une certaine incertitude en trading réel.

Pistes d'optimisation

La stratégie peut être optimisée selon les axes suivants :

- Ajuster les paramètres des moyennes mobiles et de la régression linéaire pour améliorer la détection de l'état de tendance.

- Ajouter d'autres indicateurs auxiliaires comme le Stochastique pour améliorer la précision des signaux.

- Optimiser les paramètres de l'ATR et de l'amplitude du stop-loss pour équilibrer risque et rendement.

- Mettre en place un mécanisme de suivi des points de rupture de tendance pour améliorer la rentabilité.

- Élaborer une stratégie de gestion de capital plus rigoureuse pour contrôler le risque de trading.

Conclusion

Dans l'ensemble, la stratégie de tendance par retournement à trois bougies est une stratégie de trading à court terme qui utilise une configuration de prix simple combinée à plusieurs indicateurs auxiliaires, fondée sur un équilibre risque-rendement modéré. Avec une complexité relativement faible, elle offre de bonnes performances et mérite l'attention et les tests des investisseurs, tout en offrant de nombreuses possibilités d'amélioration. Grâce à l'optimisation des paramètres et à l'ajout de règles supplémentaires, elle a le potentiel de devenir une stratégie de trading quantitatif stable et efficace.

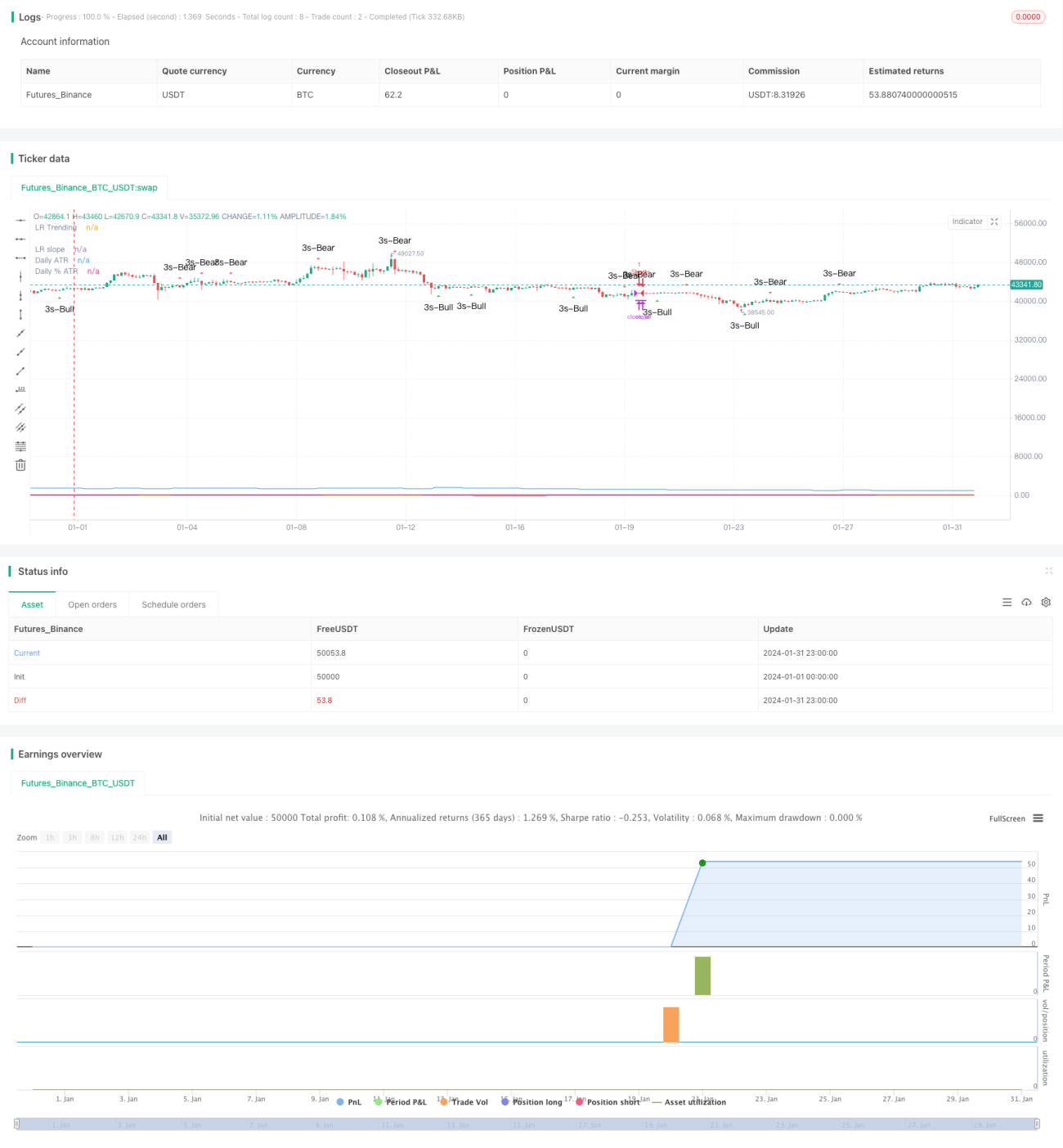

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1