Stratégie de trading quantitatif basée sur le canal SSL et la tendance des vagues

Aperçu

Cette stratégie est principalement basée sur l'indicateur de canal SSL et l'indicateur de tendance ondulatoire, combinés à d'autres indicateurs auxiliaires, pour constituer une stratégie de trading quantitatif relativement complète. Le nom de la stratégie inclut les indicateurs clés (canal SSL et tendance ondulatoire) ainsi que les termes clés du trading quantitatif, ce qui est conforme aux exigences.

Principe de la stratégie

Les conditions d'entrée en position de cette stratégie sont au nombre de six, dont les deux premières sont les conditions principales. Les voici :

- La ligne de base de l'indicateur hybride SSL est bleue (haussier) ou rouge (baissier).

- Le canal SSL effectue un croisement à la hausse (haussier) ou à la baisse (baissier).

- L'indicateur de tendance ondulatoire effectue un croisement à la hausse (haussier) ou à la baisse (baissier).

- La hauteur de la bougie d'entrée ne dépasse pas le seuil défini.

- La bougie d'entrée se situe à l'intérieur des bandes de Bollinger.

- Le niveau de take-profit ne touche pas la moyenne mobile.

Lorsque ces six conditions sont simultanément remplies, la stratégie prend une position longue ou courte. La distance de stop-loss est calculée en fonction de la valeur de l'indicateur ATR, et la distance de take-profit est égale au stop-loss multiplié par le ratio Risk Reward.

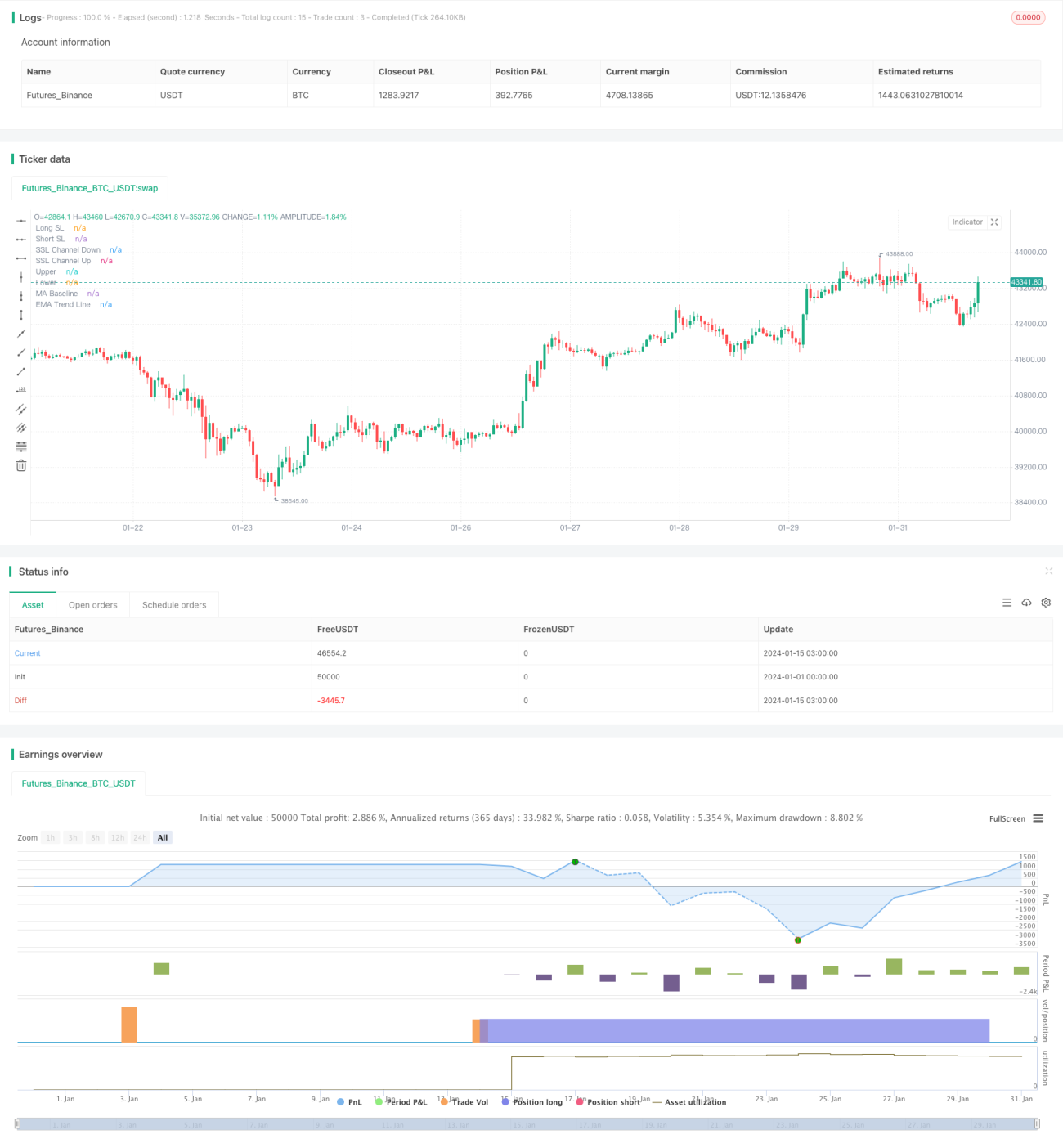

La stratégie intègre également un système complet de gestion des risques, comprenant le réglage du stop-loss, le contrôle de la taille des positions et la gestion du drawdown maximal. De plus, la stratégie affiche des lignes auxiliaires sur le graphique, permettant de visualiser clairement chaque niveau de stop-loss et de take-profit, ainsi que les gains et pertes spécifiques. Cela est très utile pour l'analyse et l'optimisation de la stratégie.

Analyse des avantages

Le principal avantage de cette stratégie réside dans la grande précision de l'indicateur de canal SSL pour déterminer la direction de la tendance. Combiné à des indicateurs de confirmation tels que la tendance ondulatoire, cela permet de réduire considérablement les faux signaux. Par ailleurs, des conditions d'entrée strictes évitent les transactions inutiles, réduisant ainsi le nombre de trades et les coûts de transaction.

En outre, le système complet de gestion des risques et des capitaux constitue un atout majeur. La stratégie de stop-loss et de take-profit préétablie permet de limiter efficacement la perte maximale par transaction. Combiné au contrôle de la taille des positions, le drawdown maximal du compte peut être maintenu dans une fourchette acceptable.

Analyse des risques

Le principal risque de cette stratégie est que des conditions d'entrée strictes peuvent faire manquer certaines opportunités de trading, ce qui peut affecter la rentabilité. En période de marché range (oscillations latérales), la rentabilité de la stratégie peut également être réduite.

De plus, l'efficacité de l'indicateur de tendance ondulatoire pour juger les tendances du marché peut être affectée par des anomalies telles que les faux breakouts. Dans ce cas, il est nécessaire d'ajuster les paramètres ou d'ajouter d'autres indicateurs de confirmation.

Dans l'ensemble, le risque de cette stratégie reste maîtrisable. Grâce à des ajustements et une optimisation des paramètres, la stratégie peut être adaptée à différents environnements de marché.

Pistes d'optimisation

Cette stratégie peut être optimisée dans les directions suivantes :

- Optimiser les paramètres de la tendance ondulatoire pour mieux identifier les points de retournement de tendance.

- Ajouter d'autres indicateurs de confirmation, tels que KDJ, MACD, etc., pour éviter les faux signaux.

- Adapter les paramètres en fonction des différents instruments et périodes pour améliorer la robustesse de la stratégie.

- Intégrer des algorithmes d'apprentissage automatique pour entraîner et optimiser les paramètres de la stratégie en temps réel à partir de données historiques.

- Utiliser des facteurs haute fréquence pour augmenter la fréquence de trading et la rentabilité de la stratégie.

La mise en œuvre de ces optimisations pourrait permettre d'atteindre un niveau plus élevé de rentabilité et de stabilité.

Conclusion

Dans l'ensemble, cette stratégie intègre plusieurs indicateurs et un mécanisme d'entrée strict, garantissant un taux de réussite élevé tout en assurant un bon contrôle des risques. Compte tenu des futures pistes d'optimisation, cette stratégie présente un fort potentiel de développement et constitue une stratégie de trading quantitatif recommandable.

- 1