Stratégie de tendance avec moyenne mobile et stop suiveur bidirectionnel

Aperçu

Cette stratégie combine l'utilisation des indicateurs SuperTrend, du canal de base hybride SSL et de l'indicateur de forme QQE, pour réaliser un trailing stop sur des positions longues et courtes, afin de capturer les tendances à moyen et long terme.

Principe de la stratégie

Cette stratégie repose principalement sur les points suivants :

- Utilisation de l'indicateur SuperTrend pour déterminer la direction générale de la tendance, comme aide à l'identification des points d'entrée.

- Identification des points d'entrée spécifiques basés sur le canal de base hybride SSL. La cassure du canal sert de signal d'entrée de base.

- Utilisation des croisements haussiers/baissiers de l'indicateur QQE comme signal de confirmation secondaire pour l'entrée.

- L'indicateur ATR aide à calculer les niveaux de stop-loss et de take-profit.

- Utilisation d'une gestion des risques basée sur un pourcentage et d'une stratégie d'ajustement dynamique du stop-loss pour contrôler le risque par transaction.

La logique d'entrée est la suivante : on entre en position lorsque le SuperTrend s'inverse, que le prix dépasse le canal de base, et que l'indicateur QQE effectue un croisement dans la direction correspondante.

Ce système combiné d'indicateurs permet de contrôler efficacement le timing d'entrée, évitant d'ouvrir des positions inutilement pendant les périodes de range.

La logique de sortie est relativement simple : le signal de sortie est donné par un retournement du SuperTrend, ou par le déclenchement du stop-loss ou du take-profit.

Analyse des avantages

Le principal avantage de cette stratégie est l'utilisation conjointe de plusieurs indicateurs, ce qui permet de filtrer efficacement les faux breakout et de réduire la probabilité de trades inefficaces.

De plus, l'utilisation d'un stop-loss basé sur un pourcentage pour contrôler le risque par transaction est un point fort de cette stratégie.

En calculant le niveau de stop-loss via l'ATR, combiné à un multiple de stop-loss configurable, nous pouvons connaître clairement le risque de chaque transaction. C'est crucial pour la gestion des risques.

Nous pouvons même définir un pourcentage de perte maximale acceptable pour limiter les pertes globales.

Cette stratégie utilise également un trailing stop pour verrouiller les profits, ce qui est essentiel pour améliorer les rendements.

Analyse des risques

Le plus grand risque de cette stratégie réside dans la probabilité que les signaux combinés soient erronés. Bien que nous utilisions un filtre multi-indicateurs, aucun indicateur ne peut éviter complètement les erreurs.

Lorsque le SuperTrend produit un faux breakout, ou que le QQE génère un signal erroné, la stratégie a tendance à entrer en position, augmentant le risque de déclenchement du stop-loss.

De plus, cette stratégie fait face à un certain risque de suroptimisation. Le réglage des paramètres doit être prudent pour éviter une dépendance excessive aux données historiques.

Nous devons prêter attention aux paramètres clés tels que la période de l'ATR, le multiple de stop-loss, le pourcentage de risque, etc. Ces paramètres doivent être ajustés individuellement en fonction des différents actifs.

Axes d'optimisation

Cette stratégie offre encore des possibilités d'optimisation :

- Tester la combinaison d'autres indicateurs, par exemple en ajoutant l'indicateur KD (stochastique) comme aide à la décision.

- Expérimenter la stabilité avec différents réglages de paramètres.

- Tenter d'utiliser des méthodes d'apprentissage automatique pour optimiser automatiquement les paramètres.

- Introduire un mécanisme de stop-loss adaptatif qui ajuste l'amplitude du stop en fonction de la volatilité du marché.

- Ajouter une logique de ré-entrée après un stop-loss pour réduire les opportunités manquées.

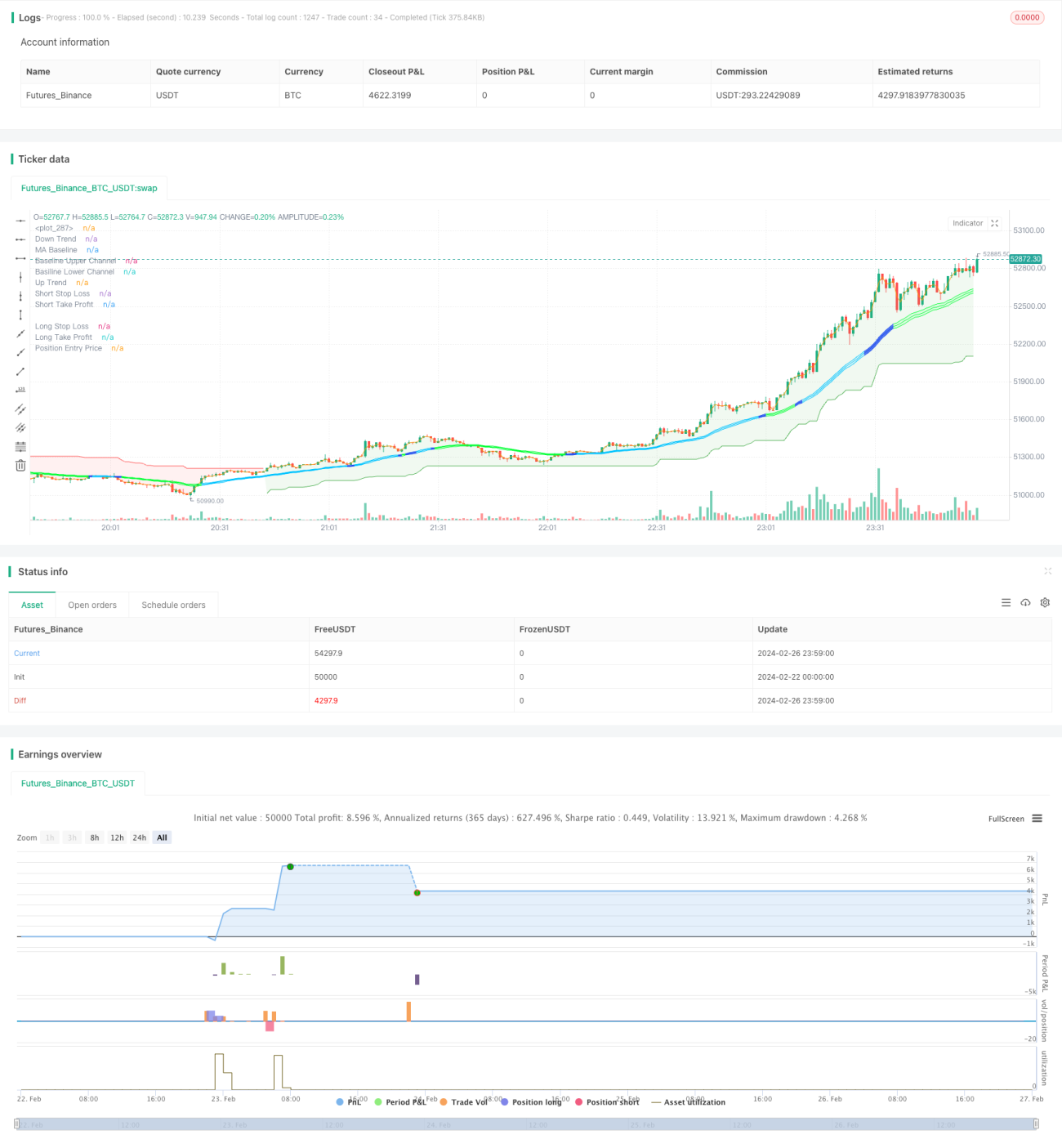

/*backtest

start: 2024-02-22 00:00:00

end: 2024-02-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to W3MCT - @simonFUTURE2 w3mct.com -

// @version=5- 1