Stratégie haussière de momentum et de tendance avec MACD, RSI et Ichimoku

Aperçu

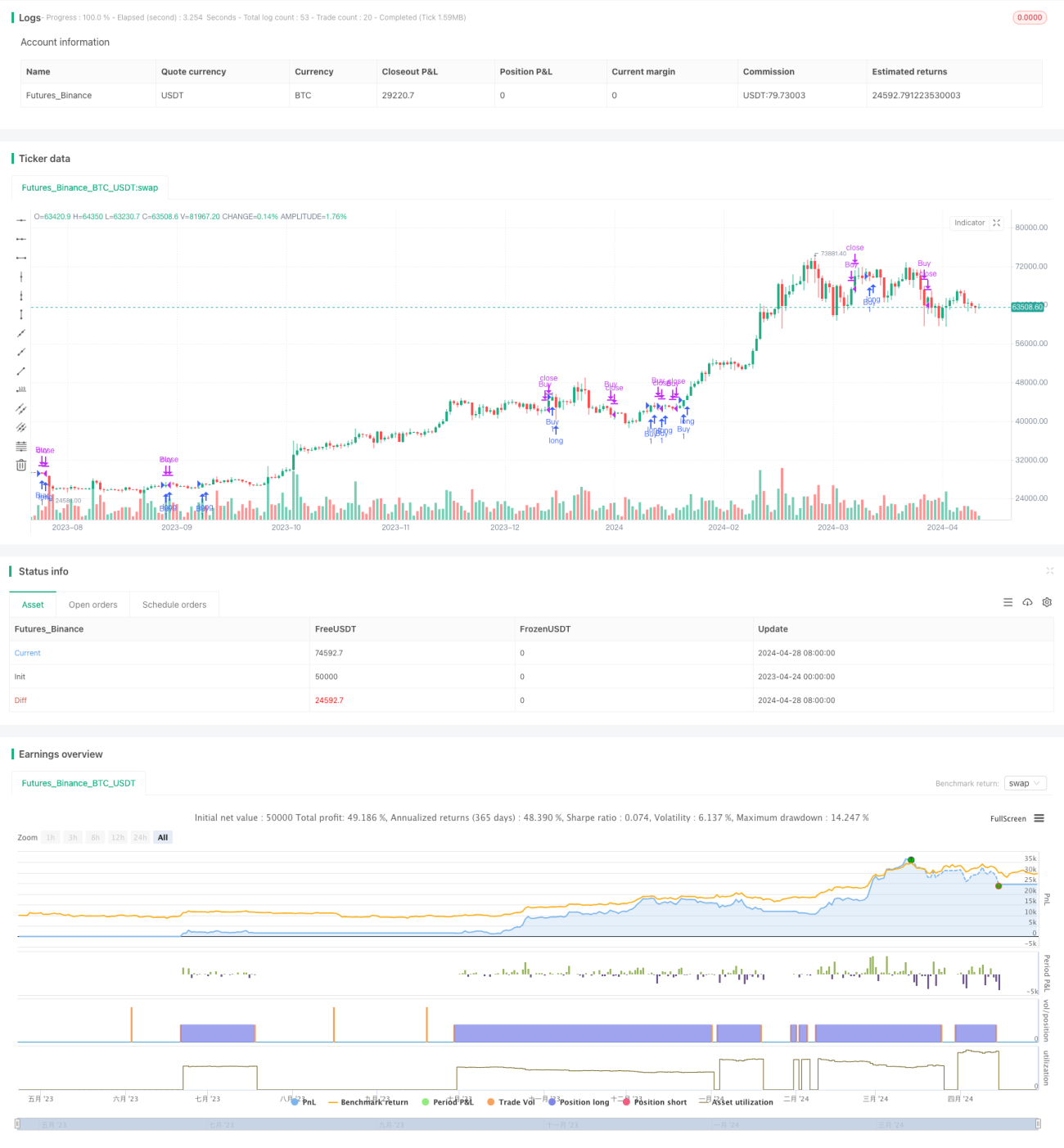

La « Stratégie haussière de momentum de tendance MACD RSI Ichimoku » est une stratégie de trading quantitatif qui combine les indicateurs MACD, RSI et Ichimoku. En analysant les signaux du MACD, du RSI et du nuage Ichimoku, cette stratégie capture la tendance et le momentum du marché, dans le but de suivre la tendance et de saisir les opportunités d'achat et de vente. La stratégie permet de paramétrer de manière flexible les indicateurs et les périodes de trading, ce qui la rend adaptable à différents styles de trading et marchés.

Principe de la stratégie

Le cœur de cette stratégie repose sur l'utilisation combinée des indicateurs MACD, RSI et Ichimoku :

- Le MACD est constitué de la différence entre une moyenne mobile rapide et une moyenne mobile lente, servant à déterminer la direction de la tendance et le changement de momentum. Lorsque la ligne rapide du MACD croise au-dessus de la ligne lente, un signal d'achat est généré ; lorsqu'elle croise en dessous, un signal de vente est émis.

- Le RSI mesure l'amplitude des variations de prix sur une période donnée, indiquant les conditions de surachat ou de survente. Lorsque le RSI est inférieur à 30, le marché est potentiellement en situation de survente ; au-dessus de 70, il est en surachat.

- Le nuage Ichimoku est composé de la ligne de conversion, de la ligne de base, de la première avance et de la seconde avance, fournissant des informations sur les niveaux de support, de résistance et la force de la tendance.

La stratégie ouvre une position longue lorsque le MACD est haussier, que le prix se trouve au-dessus du nuage et que le RSI n'est pas en surachat ; elle ferme la position lorsque le MACD forme un croisement baissier ou que le prix passe sous le nuage.

Avantages de la stratégie

- Validation multi-indicateurs améliorant la précision de l'identification de tendance. Le MACD saisit la direction de la tendance, le RSI aide au choix du timing, et l'Ichimoku offre une vue d'ensemble plus complète du marché, renforçant la fiabilité de la stratégie.

- Paramètres flexibles et grande adaptabilité. Permet d'ajuster les paramètres du MACD, du RSI et de l'Ichimoku pour répondre à différents styles de trading et caractéristiques de marché.

- Gestion des risques. Mise en place de stop-loss et take-profit pour contrôler le drawdown ; construction de positions par étapes pour réduire le risque d'achat.

- Large champ d'application. Peut être utilisé sur plusieurs marchés et instruments pour saisir diverses opportunités de tendance.

Risques de la stratégie

- Conflits de signaux entre indicateurs. Le MACD, le RSI et l'Ichimoku peuvent occasionnellement générer des signaux contradictoires, conduisant à des erreurs de jugement.

- Paramètres inappropriés. Des paramètres mal ajustés peuvent rendre la stratégie inefficace ; une optimisation basée sur les caractéristiques du marché et les backtests est nécessaire.

- Performance médiocre en marché rangeant. Les stratégies de tendance ont tendance à effectuer des transactions fréquentes dans les marchés sans tendance claire, et des coûts élevés peuvent éroder les profits.

- Risque d'événements imprévus. Certains événements peuvent provoquer des fluctuations anormales des prix, allant à l'encontre des signaux des indicateurs.

Pistes d'optimisation

- Renforcer les conditions de confirmation de tendance, par exemple une hausse continue du prix dans le nuage, des divergences du MACD, etc., pour améliorer la qualité des ouvertures de positions.

- Introduire des stop-loss, take-profit et une gestion de la taille des positions pour contrôler le drawdown et améliorer le ratio rendement/risque.

- Optimiser les paramètres pour s'adapter aux caractéristiques des différents instruments et périodes, améliorant la robustesse.

- Envisager d'ajouter un trailing stop pour verrouiller les profits et amplifier les avantages.

Conclusion

La « Stratégie haussière de momentum de tendance MACD RSI Ichimoku » est une stratégie de trading quantitatif puissante qui utilise de manière combinée les indicateurs MACD, RSI et Ichimoku pour une analyse complète de la tendance et du momentum. Dans des marchés directionnels, elle démontre une bonne capacité à capturer les tendances et à gérer le rythme. Grâce à l'optimisation des paramètres et aux mesures de contrôle des risques, cette stratégie peut devenir un outil efficace pour saisir les opportunités du marché et obtenir des rendements stables.

- 1