漢越 - Stratégie de trading suiveur de tendance basée sur plusieurs EMA, ATR et RSI

Aperçu

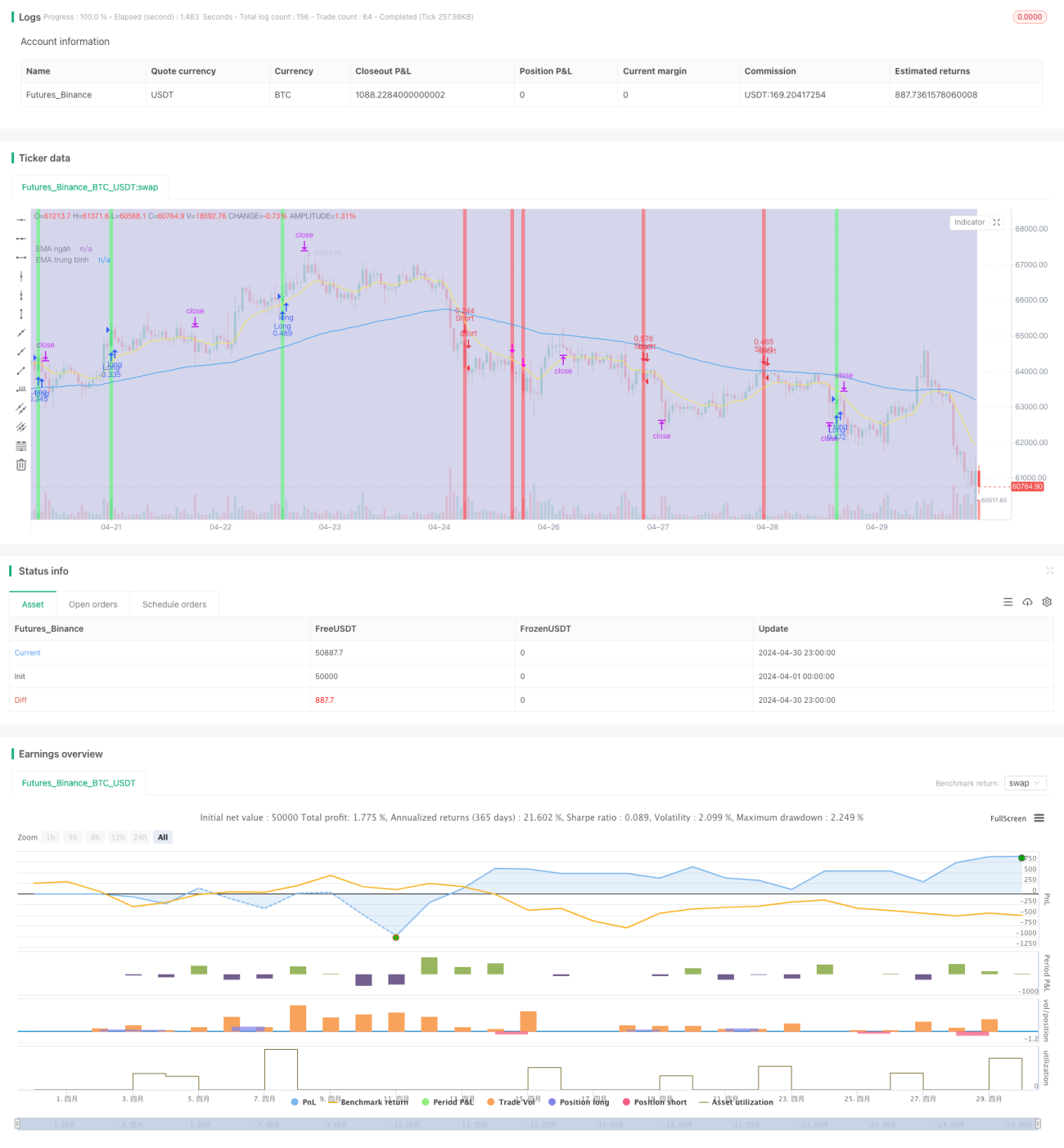

Cette stratégie utilise trois moyennes mobiles exponentielles (EMA) de périodes différentes pour déterminer la tendance du marché, combinées avec l’indice de force relative (RSI) et l’Average True Range (ATR) pour identifier les points d’entrée ainsi que les niveaux de stop-loss et de take-profit. Lorsque le prix franchit le canal formé par les trois EMA et que le RSI franchit également sa moyenne mobile, la stratégie déclenche un signal d’ouverture de position. L’ATR est utilisé pour contrôler la taille des positions et définir le stop-loss, tandis que le ratio risque/récompense (RR) détermine le take-profit. Le principal avantage de cette stratégie réside dans sa simplicité et son efficacité : elle suit la tendance du marché tout en limitant les pertes potentielles grâce à des mesures de gestion du risque strictes.

Principe de la stratégie

- Calcul de trois EMA de périodes différentes (court, moyen et long terme) pour évaluer la tendance globale du marché.

- Utilisation du RSI pour confirmer la force et la durabilité de la tendance : lorsque le RSI franchit sa moyenne mobile, cela indique un changement de tendance.

- Combinaison de la relation entre le prix et le canal des EMA avec les signaux du RSI pour générer un signal d’ouverture : lorsque le prix franchit le canal des EMA et que le RSI franchit également sa moyenne mobile, on ouvre une position dans le sens de la tendance.

- Utilisation de l’ATR pour déterminer la taille des positions et le niveau de stop-loss, afin de contrôler l’exposition au risque de chaque transaction.

- Fixation du take-profit selon un ratio risque/récompense prédéfini (par exemple 1,5:1) pour assurer la rentabilité de la stratégie.

Analyse des avantages

- Simplicité et efficacité : La stratégie n’utilise que quelques indicateurs techniques courants, avec une logique claire, facile à comprendre et à mettre en œuvre.

- Suivi de tendance : Grâce à la combinaison du canal des EMA et du RSI, la stratégie suit la tendance du marché et capture les mouvements de prix importants.

- Contrôle du risque : L’utilisation de l’ATR pour définir le stop-loss et gérer la taille des positions limite efficacement l’exposition au risque de chaque transaction.

- Flexibilité : Les paramètres de la stratégie (périodes des EMA, période du RSI, multiple de l’ATR, etc.) peuvent être ajustés en fonction des différents marchés et styles de trading pour optimiser les performances.

Analyse des risques

- Optimisation des paramètres : La performance de la stratégie dépend fortement du choix des paramètres. Un réglage inapproprié peut entraîner une défaillance ou une underperformance.

- Risque de marché : En cas d’événements imprévus ou de conditions de marché extrêmes, la stratégie peut subir des pertes importantes, en particulier lors de retournements de tendance ou dans des marchés en range.

- Surapprentissage : Si l’optimisation des paramètres est trop ajustée sur les données historiques, la stratégie peut donner de mauvais résultats en trading réel.

Axes d’optimisation

- Paramètres dynamiques : Ajuster dynamiquement les paramètres de la stratégie en fonction des conditions du marché, par exemple en utilisant des EMA de périodes plus longues en tendance claire et des périodes plus courtes en marché sans tendance.

- Combinaison avec d’autres indicateurs : Introduire d’autres indicateurs techniques (comme les bandes de Bollinger, le MACD, etc.) pour améliorer la fiabilité et la précision des signaux d’ouverture.

- Intégration du sentiment du marché : Combiner des indicateurs de sentiment (comme l’indice de peur et de cupidité) pour ajuster l’exposition au risque et la gestion des positions.

- Analyse multi‑timeframe : Analyser la tendance et les signaux sur différentes échelles de temps pour obtenir une vision plus complète du marché et des décisions de trading plus robustes.

Résumé

Cette stratégie construit un système de trading de suivi de tendance simple et efficace en combinant plusieurs indicateurs techniques courants tels que l’EMA, le RSI et l’ATR. Elle utilise le canal des EMA pour déterminer la tendance du marché, le RSI pour confirmer la force de la tendance, et l’ATR pour contrôler le risque. Ses principaux atouts sont la simplicité et l’adaptabilité, permettant de trader en suivant la tendance dans différentes conditions de marché. Cependant, ses performances dépendent largement du choix des paramètres : un réglage inapproprié peut entraîner une défaillance ou une underperformance. De plus, dans des événements imprévus ou des conditions de marché extrêmes, la stratégie peut être confrontée à des risques importants. Pour l’optimiser davantage, on peut envisager l’ajustement dynamique des paramètres, la combinaison avec d’autres indicateurs, l’intégration de l’analyse du sentiment du marché et l’analyse multi‑timeframe. Dans l’ensemble, cette stratégie offre une bonne base pour le trading de suivi de tendance, mais elle doit encore être adaptée et optimisée en fonction des conditions réelles du marché.

- 1