Stratégie de trading basée sur l'indice de force relative (RSI), la moyenne mobile simple (SMA) et l'écart-type de volatilité (DEV)

Aperçu

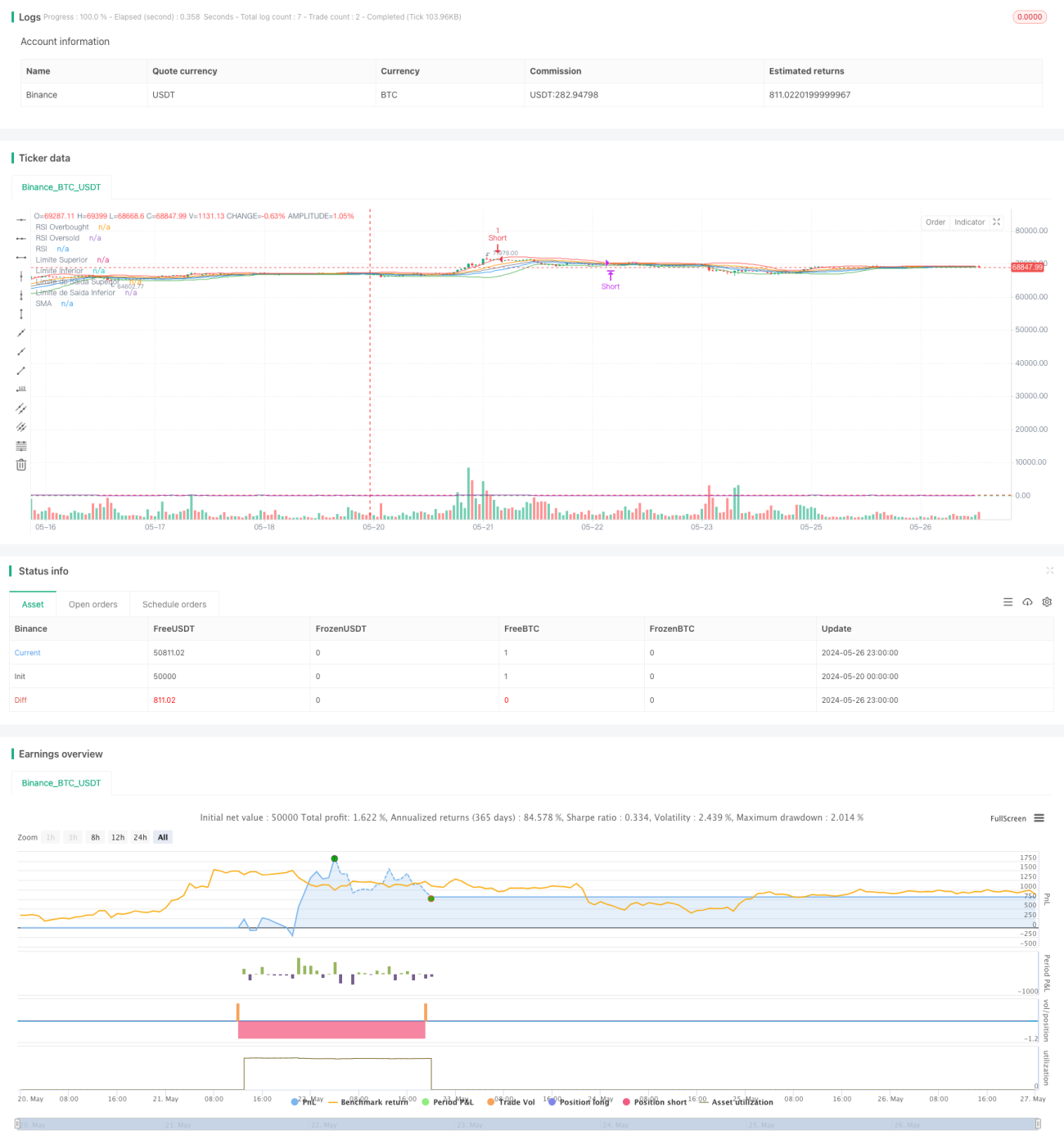

Cette stratégie Pine Script est basée sur l'indice de force relative (RSI) et l'écart-type (DEV) de la volatilité des prix. Elle compare les prix avec des bandes supérieure et inférieure pour déterminer les points d'entrée, tout en utilisant le RSI comme filtre auxiliaire. Un signal d'ouverture de position est généré lorsque le prix touche une bande et que le RSI atteint une zone de surachat ou de survente. La position est fermée lorsque le prix franchit en sens inverse la bande de sortie ou que le RSI atteint de manière inverse une zone de surachat ou de survente. Cette stratégie s'adapte dynamiquement aux conditions du marché, permettant de limiter les pertes en période de forte volatilité et de conserver les gains en période de faible volatilité. C'est une stratégie de trading quantitative capable de s'adapter à différents états de marché.

Principe de la stratégie

- Calculer la moyenne mobile simple (SMA) et l'écart-type (DEV) du prix sur les

lengthdernières périodes. - Construire un canal de volatilité avec la SMA comme axe central, la bande supérieure = SMA + thresholdEntry * DEV et la bande inférieure = SMA - thresholdEntry * DEV.

- Calculer simultanément le RSI sur

rsiLengthpériodes basé sur le cours de clôture. - Lorsque le prix franchit à la hausse la bande inférieure et que le RSI est inférieur au seuil de survente

rsiOversold, générer un signal d'achat (long). - Lorsque le prix franchit à la baisse la bande supérieure et que le RSI est supérieur au seuil de surachat

rsiOverbought, générer un signal de vente (short). - Construire un second canal de sortie plus étroit, avec la SMA comme axe central, la bande supérieure = SMA + thresholdExit * DEV et la bande inférieure = SMA - thresholdExit * DEV.

- En position longue, si le prix franchit à la baisse la bande de sortie inférieure ou si le RSI dépasse le seuil de surachat, fermer la position longue.

- En position courte, si le prix franchit à la hausse la bande de sortie supérieure ou si le RSI descend en dessous du seuil de survente, fermer la position courte.

Analyse des avantages

- L'utilisation combinée du comportement des prix et d'un indicateur de momentum permet de filtrer efficacement les faux signaux.

- L'ajustement dynamique de la largeur du canal en fonction de la volatilité permet à la stratégie de s'adapter à différents états de marché.

- La mise en place de deux canaux permet de stopper les pertes dès les premiers retournements de prix, de contrôler le drawdown, tout en conservant les gains lorsque la tendance se forme.

- La logique du code et les paramètres sont clairs et faciles à comprendre et à optimiser.

Analyse des risques

- En cas de tendance unidirectionnelle prolongée, la stratégie peut déclencher un stop-loss prématuré et manquer les profits de tendance.

- Les performances de la stratégie sont très sensibles aux paramètres, qui doivent être optimisés séparément pour chaque instrument et période.

- La stratégie est plus performante dans un marché rangeant, mais moyenne en marché en tendance. Un retournement brutal d'une tendance de long terme peut entraîner un drawdown important.

- Si la volatilité de l'actif sous-jacent change brusquement, les paramètres fixes peuvent devenir inefficaces.

Pistes d'optimisation

- Introduire des indicateurs de tendance (croisement de moyennes mobiles court/long terme, ADX, etc.) pour distinguer les marchés en tendance des marchés rangeants et utiliser des paramètres différents.

- Envisager l'utilisation d'indicateurs de volatilité plus adaptatifs, comme l'ATR, pour ajuster dynamiquement la largeur du canal de volatilité.

- Avant d'ouvrir une position, analyser la tendance du prix pour détecter une tendance claire et éviter les trades à contre-tendance.

- Optimiser différentes combinaisons de paramètres par algorithme génétique, grille de recherche, etc., pour trouver le meilleur réglage.

- Envisager d'utiliser des paramètres différents pour les positions longues et courtes afin de contrôler l'exposition au risque.

Conclusion

Cette stratégie combine un canal de volatilité avec l'indice RSI : elle prend des décisions d'ouverture et de fermeture en se référant au RSI tout en tenant compte des fluctuations des prix. Elle permet de bien capter les tendances de court terme, de stopper les pertes à temps et d'empocher les gains. Cependant, sa performance dépend fortement du réglage des paramètres, qui doivent être optimisés en fonction de l'environnement de marché et de l'actif sous-jacent. Il est également conseillé d'introduire d'autres indicateurs pour aider à juger la tendance du marché, afin de tirer pleinement parti de la stratégie. Dans l'ensemble, cette stratégie est clairement conçue, logiquement rigoureuse et constitue une bonne stratégie de trading quantitative.

- 1