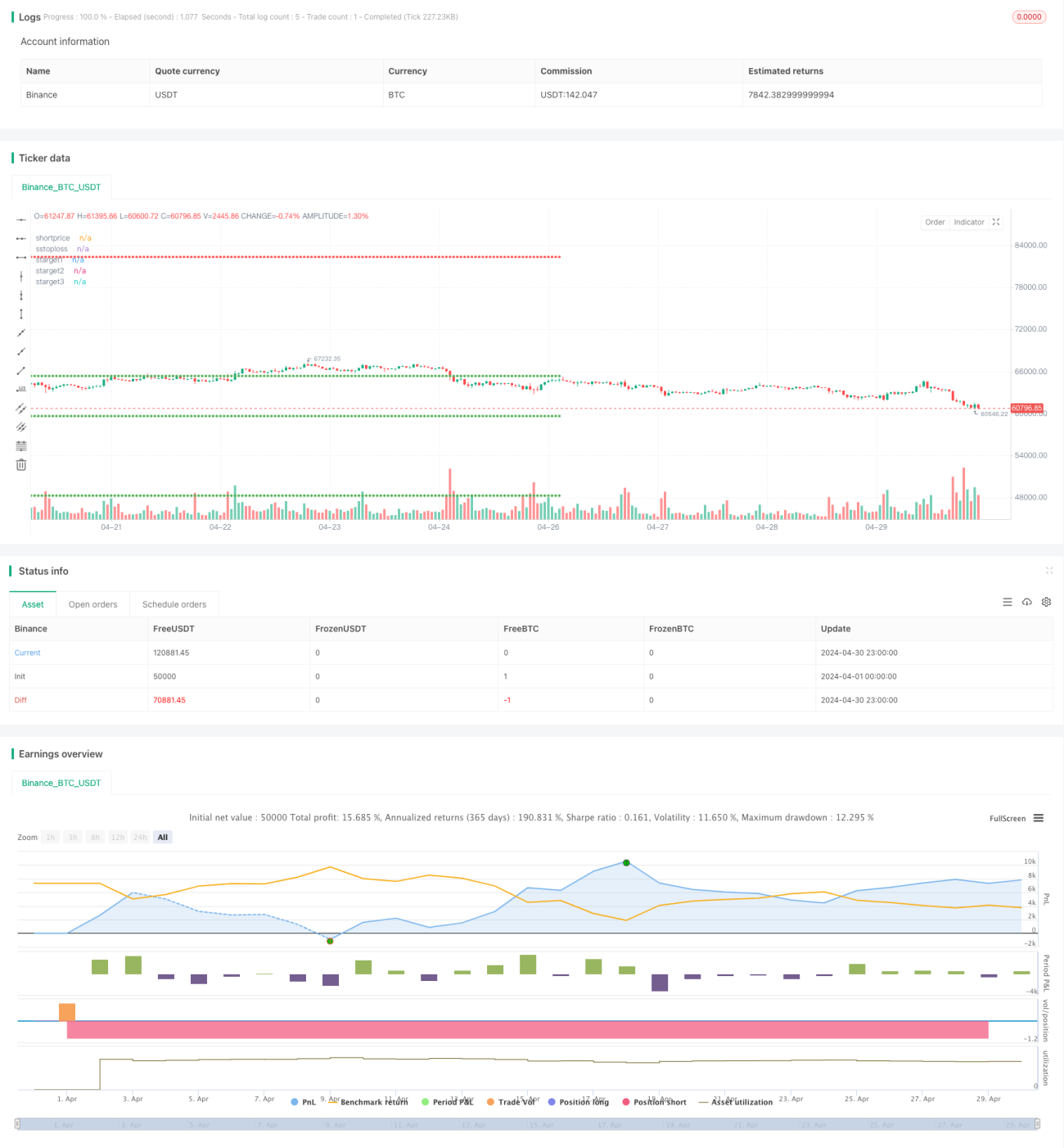

Stratégie quantitative basée sur PSAR et EMA

Aperçu

Cette stratégie quantitative utilise principalement les signaux de croisement entre l'indicateur Parabolic SAR (PSAR) et la Moyenne Mobile Exponentielle (EMA), combinés à plusieurs conditions personnalisées, pour générer des signaux d'achat et de vente. L'idée principale de la stratégie est la suivante : lorsque le PSAR franchit l'EMA par le bas et que certaines conditions sont remplies, un signal d'achat est généré ; lorsque le PSAR passe sous l'EMA par le haut et que certaines conditions sont remplies, un signal de vente est généré. Parallèlement, la stratégie intègre des niveaux de take profit et de stop loss pour contrôler le risque.

Principe de la stratégie

- Calculer le PSAR et l'EMA sur 30 périodes.

- Déterminer la relation de croisement entre le PSAR et l'EMA, et définir les indicateurs correspondants.

- En combinant la position relative du PSAR par rapport à l'EMA, la couleur des bougies, etc., définir le IGC (Ideal Green Candle) et le IRC (Ideal Red Candle).

- Utiliser l'apparition des IGC et IRC pour déterminer les signaux d'achat et de vente.

- Définir les niveaux de take profit et de stop loss : take profit à 8 %, 16 % et 32 % du prix d'achat, stop loss à 16 % du prix d'achat ; take profit à 8 %, 16 % et 32 % du prix de vente, stop loss à 16 % du prix de vente.

- Exécuter les opérations d'achat, de vente ou de clôture en fonction de la période de trading et de l'état de la position.

Avantages de la stratégie

- La combinaison de plusieurs indicateurs et conditions améliore la fiabilité des signaux.

- La présence de multiples niveaux de take profit et de stop loss permet de contrôler flexiblement les risques et les gains.

- Des filtres d'achat et de vente adaptés aux différentes conditions de marché augmentent l'adaptabilité de la stratégie.

- Le code est hautement modulaire, ce qui le rend facile à comprendre et à modifier.

Risques de la stratégie

- Les paramètres de la stratégie peuvent ne pas convenir à tous les environnements de marché et doivent être ajustés en fonction des conditions réelles.

- Dans un marché en range, la stratégie peut générer des signaux de trading fréquents, augmentant ainsi les coûts de transaction.

- La stratégie manque d'une évaluation de la tendance du marché et peut manquer des opportunités dans un marché en forte tendance.

- Le niveau de stop loss peut ne pas éviter complètement les risques liés aux mouvements extrêmes du marché.

Directions d'optimisation

- Introduire davantage d'indicateurs techniques ou d'indicateurs de sentiment de marché pour améliorer la précision et la fiabilité des signaux.

- Optimiser les niveaux de take profit et de stop loss ; envisager l'adoption de take profit/stop loss dynamiques ou basés sur la volatilité.

- Définir différents paramètres et règles de trading en fonction des différents états du marché pour améliorer l'adaptabilité.

- Ajouter un module de gestion de capital pour ajuster dynamiquement la taille des positions et l'exposition au risque en fonction de facteurs tels que le ratio de fonds propres (equity ratio balance).

Résumé

Cette stratégie quantitative, basée sur les indicateurs PSAR et EMA, génère des signaux d'achat et de vente via plusieurs conditions et règles personnalisées. Elle présente une certaine adaptabilité et flexibilité, tout en intégrant des niveaux de take profit et de stop loss pour contrôler le risque. Cependant, il reste des possibilités d'optimisation concernant le réglage des paramètres et la gestion du risque. Dans l'ensemble, cette stratégie peut servir de modèle de base et, après des améliorations et optimisations supplémentaires, pourrait devenir une stratégie de trading robuste.

- 1