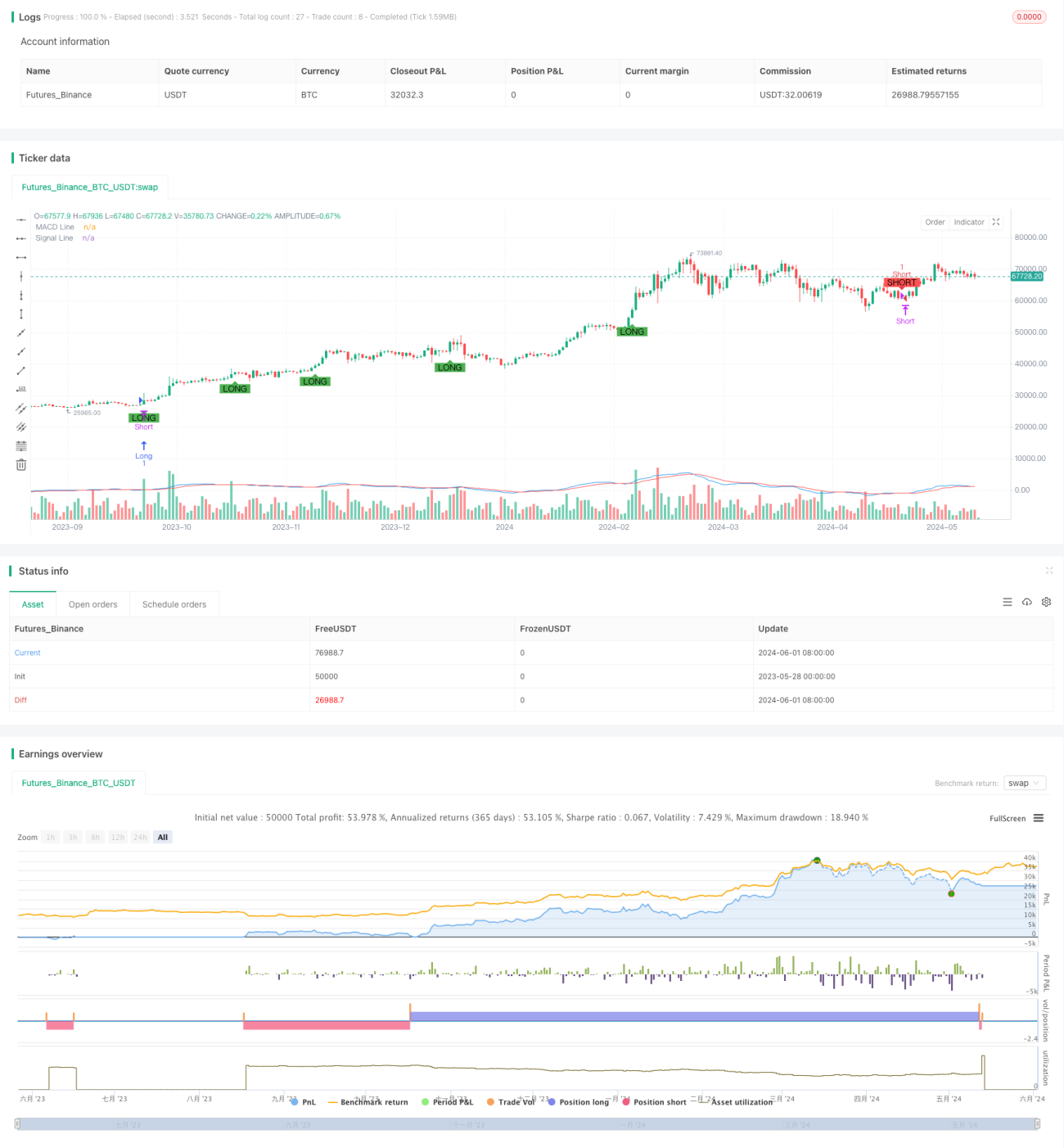

Stratégie de convergence intrajournalière basée sur le MACD et le ratio R:R

Aperçu

Cette stratégie utilise la convergence et la divergence de l'indicateur MACD pour déterminer les signaux de trading. Lorsque la ligne MACD croise la ligne de signal et que la valeur de la ligne MACD est supérieure à 1,5 ou inférieure à -1,5, des signaux d'achat et de vente à découvert sont générés respectivement. En outre, la stratégie définit des niveaux fixes de take-profit et stop-loss et intègre le concept du rapport risque/rendement (R:R). De plus, elle utilise des limites de perte et de profit maximal intrajournalières ainsi qu'un stop-loss suiveur plus strict pour mieux contrôler les risques.

Principe de la stratégie

- Calculer les lignes MACD et la ligne de signal de l'indicateur MACD.

- Détecter les croisements entre la ligne MACD et la ligne de signal, tout en considérant si la valeur de la ligne MACD dépasse un certain seuil (1,5 et -1,5).

- Lorsqu'un signal d'achat apparaît, ouvrir une position longue, avec un take-price fixé au plus haut actuel + 600 unités de tick, et un stop-loss au plus bas actuel - 100 unités de tick.

- Lorsqu'un signal de vente à découvert apparaît, ouvrir une position courte, avec un take-price fixé au plus bas actuel - 600 unités de tick, et un stop-loss au plus haut actuel + 100 unités de tick.

- Introduire une logique de stop-loss suiveur : lorsque le prix dépasse le prix d'ouverture de la position (hausse pour les positions longues, baisse pour les positions courtes) de plus de 300 unités de tick, le stop-loss est déplacé vers prix d'ouverture + (cours de clôture - prix d'ouverture - 300) pour les positions longues, ou prix d'ouverture - (prix d'ouverture - cours de clôture - 300) pour les positions courtes.

- Définir des limites de perte et de gain maximal intrajournalières : lorsque la perte du jour atteint 600 unités de tick ou le gain atteint 1800 unités de tick, fermer toutes les positions.

Analyse des avantages

- Combinaison de l'indicateur MACD avec des conditions de seuil de prix, filtrant efficacement certains signaux parasites.

- Rapport risque/rendement (R:R) fixe, avec un risque et un rendement contrôlables par transaction.

- Le stop-loss suiveur peut protéger les bénéfices une fois la tendance formée, réduisant ainsi les drawdowns.

- Les limites intrajournalières de perte et de gain aident à contrôler l'exposition quotidienne au risque, évitant des pertes excessives ou des drawdowns après des gains.

Analyse des risques

- L'indicateur MACD présente un retard, ce qui peut entraîner des signaux retardés ou erronés.

- Les niveaux fixes de take-profit et stop-loss peuvent ne pas s'adapter aux différentes conditions de marché, ce qui peut déclencher fréquemment des stop-loss en période de range.

- Le stop-loss suiveur peut ne pas arrêter les pertes à temps en cas de retournement de tendance, entraînant un rendu des bénéfices.

- Les limites intrajournalières de perte et de gain peuvent entraîner une fermeture prématurée des positions lorsque la tendance du jour est claire, faisant ainsi manquer des profits potentiels.

Directions d'optimisation

- Envisager d'utiliser l'indicateur MACD sur plusieurs périodes pour confirmer les signaux, améliorant ainsi leur précision.

- Ajuster dynamiquement les niveaux de take-profit et stop-loss en fonction de la volatilité du marché pour s'adapter à différentes conditions.

- Optimiser la logique du stop-loss suiveur, par exemple en utilisant l'indicateur ATR pour fixer la distance de suivi, mieux adapté aux fluctuations des prix.

- Optimiser les paramètres des limites intrajournalières de perte et de gain afin de trouver des valeurs appropriées pour contrôler les risques tout en capturant les mouvements de tendance.

Résumé

Cette stratégie détecte les signaux de trading par la convergence et la divergence de l'indicateur MACD, tout en intégrant des mesures de contrôle des risques telles que le rapport risque/rendement, le stop-loss suiveur et les limites intrajournalières. Bien que la stratégie soit capable de capturer les tendances et de contrôler les risques dans une certaine mesure, il reste des points à optimiser et à améliorer. À l'avenir, des optimisations pourraient être envisagées dans les dimensions telles que la confirmation des signaux, le take-profit/stop-loss, le stop-loss suiveur et les limites intrajournalières, afin d'obtenir des rendements plus solides et plus significatifs.

- 1