Stratégie de breakout intraday basée sur les points hauts et bas des bougies de 3 minutes

Aperçu

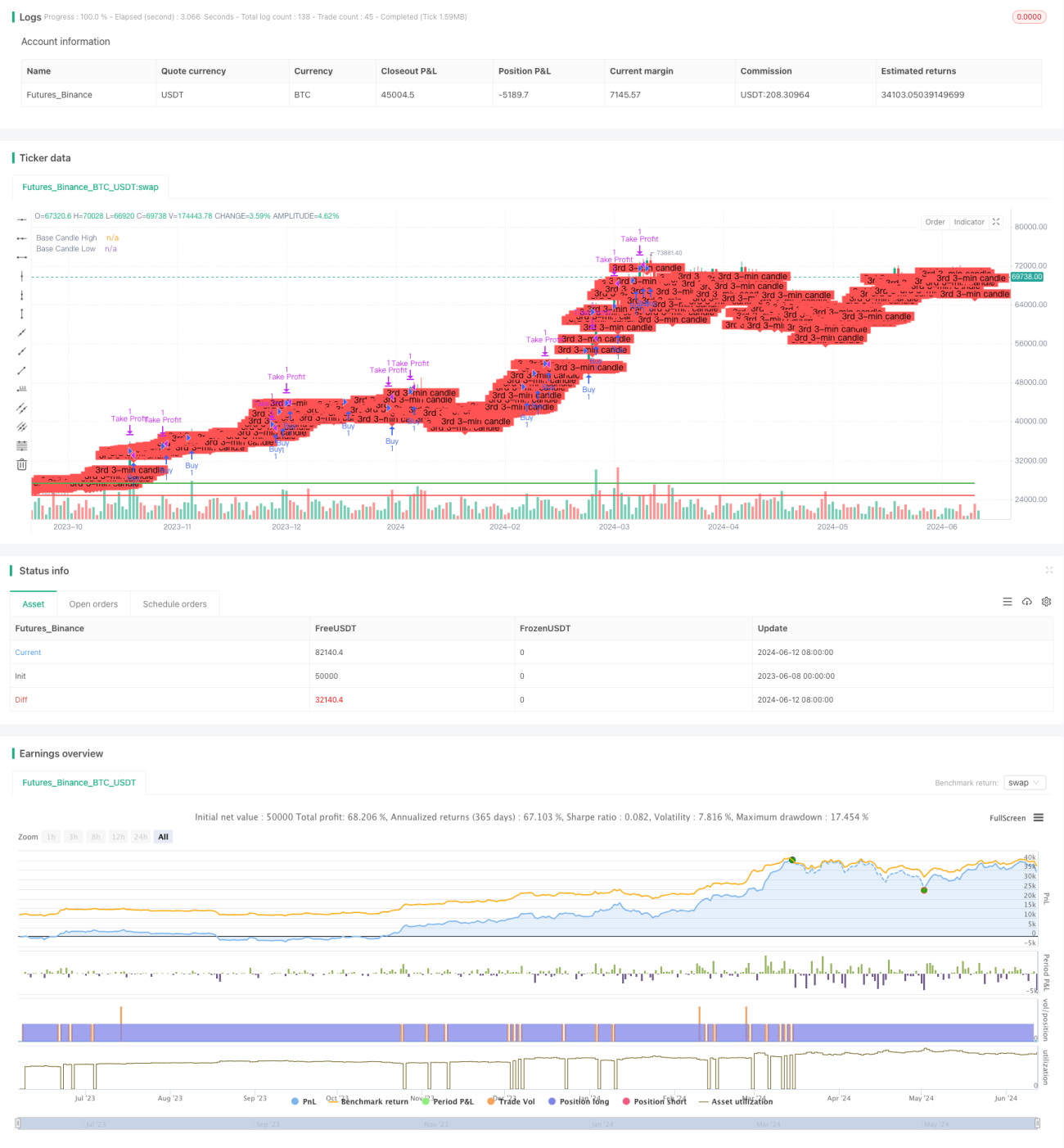

L'idée principale de cette stratégie est d'utiliser les points hauts et bas des chandeliers de 3 minutes comme niveaux de rupture. Lorsque le prix franchit le plus haut du chandelier de 3 minutes, on prend une position longue ; lorsqu'il franchit le plus bas, on prend une position courte. Cette stratégie est adaptée au trading intraday : on clôture toutes les positions à la fin de chaque journée et on reprend le trading le lendemain. Son avantage réside dans sa simplicité, sa facilité de mise en œuvre et son risque relativement faible. Cependant, elle présente aussi certains risques, notamment des drawdowns importants en cas de forte volatilité du marché.

Principe de la stratégie

- Récupérer les données des trois premières chandelles de 3 minutes après l'ouverture quotidienne, et enregistrer le plus haut et le plus bas de la troisième chandelle.

- Lorsque le prix franchit le plus haut de la troisième chandelle, ouvrir une position longue, avec un objectif de prix égal au prix d'entrée + 100 points, jusqu'à la clôture ou jusqu'à atteindre l'objectif.

- Lorsque le prix franchit le plus bas de la troisième chandelle, ouvrir une position courte, avec un objectif de prix égal au prix d'entrée - 100 points, jusqu'à la clôture ou jusqu'à atteindre l'objectif.

- Clôturer toutes les positions à la fin de chaque journée, et reprendre le trading le lendemain.

Avantages de la stratégie

- Simple à comprendre et facile à mettre en œuvre.

- Adaptée au trading intraday, avec une utilisation élevée du capital.

- Risque relativement faible, avec des niveaux de stop-loss clairs.

- Convient aux marchés à forte tendance.

Risques de la stratégie

- En cas de forte volatilité du marché, des drawdowns importants peuvent survenir.

- La période d'ouverture présente une forte volatilité des prix, ce qui augmente le risque.

- Il est difficile de bien identifier les niveaux de rupture, ce qui peut entraîner de faux signaux.

Pistes d'optimisation

- Envisager d'ajouter des indicateurs tels que les moyennes mobiles pour filtrer les signaux parasites en période de range.

- Envisager d'optimiser le moment d'ouverture des positions pour éviter la période d'ouverture.

- Envisager d'optimiser les niveaux de take-profit et de stop-loss pour améliorer la stabilité de la stratégie.

- Envisager d'intégrer une gestion de la taille des positions pour contrôler le risque de drawdown.

Résumé

Cette stratégie repose sur les ruptures des points hauts et bas des chandeliers de 3 minutes, et est adaptée au trading intraday. Ses atouts sont la simplicité, la facilité de mise en œuvre et un risque relativement faible. Cependant, elle comporte certains risques, notamment des drawdowns importants lors de fortes fluctuations du marché. On peut envisager d'optimiser cette stratégie en filtrant les signaux, en ajustant le moment d'ouverture des positions, en affinant les niveaux de take-profit/stop-loss, et en intégrant une gestion des positions, afin d'améliorer sa stabilité et sa rentabilité.

- 1