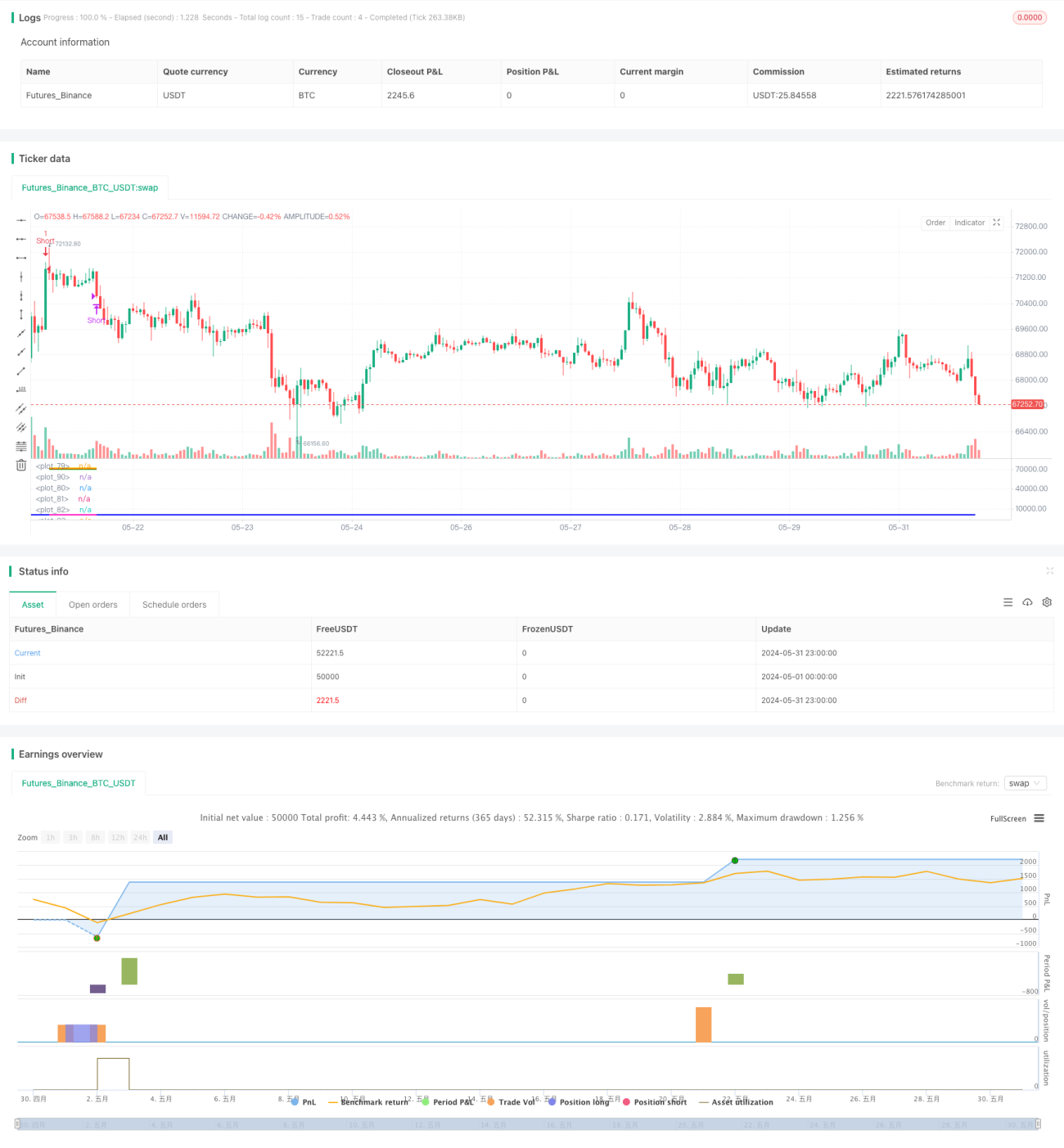

Stratégie de trading de régression RSI multi-niveaux avec ajustement dynamique de la volatilité

Aperçu

Cette stratégie est un système de trading à retour à la moyenne à plusieurs niveaux basé sur l'indicateur RSI et la volatilité des prix. Elle utilise les valeurs extrêmes du RSI et des mouvements de prix anormalement importants comme signaux d'entrée, tout en adoptant un pyramiding (ajout de positions) et des niveaux de take-profit dynamiques pour gérer les risques et optimiser les gains. L'idée centrale de la stratégie est d'entrer sur le marché lorsque des mouvements extrêmes se produisent, puis de réaliser des bénéfices lorsque les prix reviennent à des niveaux normaux.

Principe de la stratégie

-

Conditions d’entrée :

- Utilisation du RSI 20 périodes (RSI20) comme indicateur principal.

- Définition de plusieurs seuils de RSI (35/65, 30/70, 25/75, 20/80) et de seuils de volatilité correspondants.

- Lorsque le RSI atteint un certain seuil et que la taille du corps de la bougie actuelle dépasse le seuil de volatilité correspondant, un signal d’entrée est déclenché.

- Condition supplémentaire : le prix doit franchir d’un certain pourcentage les récents niveaux de support/résistance (haut/bas).

-

Mécanisme d’ajout de positions (pyramiding) :

- Maximum de 5 entrées autorisées (entrée initiale + 4 ajouts).

- Chaque ajout doit satisfaire des conditions de RSI et de volatilité plus strictes.

-

Mécanisme de sortie :

- Définition de 5 niveaux de take-profit différents.

- Les points de take-profit sont calculés dynamiquement en fonction des niveaux de support/résistance au moment de l’entrée.

- À mesure que le nombre de positions augmente, l’objectif de take-profit diminue progressivement.

-

Gestion des risques :

- Utilisation d’un modèle de risque en pourcentage : chaque transaction risque un montant fixe de 20 % du capital total du compte.

- Limite maximale de positions simultanées à 5, afin de limiter l’exposition globale.

Avantages de la stratégie

-

Entrées à plusieurs niveaux : En définissant plusieurs seuils de RSI et de volatilité, la stratégie peut capturer différents degrés d’extrêmes de marché, augmentant ainsi les opportunités de trading.

-

Take-profit dynamique : Les points de take-profit calculés à partir des niveaux de support/résistance s’adaptent automatiquement à la structure du marché, protégeant les bénéfices sans sortir trop tôt.

-

Pyramiding (ajout progressif) : En ajoutant des positions lorsque la tendance se poursuit, le potentiel de profit peut être considérablement amélioré.

-

Gestion des risques : Un pourcentage de risque fixe et une limite maximale de positions permettent un contrôle efficace du risque par transaction et du risque global.

-

Flexibilité : Un grand nombre de paramètres ajustables permet à la stratégie de s’adapter à différents environnements de marché et instruments.

-

Réversion à la moyenne + suivi de tendance : La stratégie combine les avantages de la réversion à la moyenne et du suivi de tendance, permettant de capter à la fois les retournements à court terme et de ne pas manquer les grandes tendances.

Risques de la stratégie

-

Sur-trading : Sur les marchés très volatils, les signaux de transaction peuvent être déclenchés fréquemment, entraînant des frais excessifs.

-

Faux breakout : Le marché peut connaître un mouvement extrême temporaire suivi d’un rapide retour en arrière, générant de faux signaux.

-

Pertes consécutives : Si le marché évolue de manière unidirectionnelle soutenue, plusieurs ajouts de positions peuvent entraîner des pertes importantes.

-

Sensibilité aux paramètres : Les performances de la stratégie peuvent être très sensibles aux réglages des paramètres, avec un risque de surajustement (overfitting).

-

Impact du slippage : En période de forte volatilité, un slippage important peut se produire, affectant les performances.

-

Dépendance aux conditions de marché : La stratégie peut donner de mauvais résultats dans certaines conditions de marché, par exemple en période de faible volatilité ou de tendance forte.

Pistes d’optimisation

-

Ajustement dynamique des paramètres : Introduire un mécanisme d’adaptation pour ajuster dynamiquement les seuils de RSI et de volatilité en fonction de l’état du marché.

-

Analyse multi-timeframes : Intégrer une analyse des tendances de marché à plus long terme pour améliorer la qualité des entrées.

-

Optimisation du stop-loss : Ajouter un stop-loss suiveur (trailing stop) ou un stop-loss dynamique basé sur l’ATR pour mieux contrôler les risques.

-

Filtrage des conditions de marché : Ajouter des filtres tels que la force de la tendance ou les cycles de volatilité afin d’éviter de trader dans des environnements inadaptés.

-

Optimisation de la gestion du capital : Mettre en place une gestion de position plus fine, par exemple en ajustant la taille des transactions en fonction des niveaux de signaux.

-

Intégration de l’apprentissage automatique : Utiliser des algorithmes de machine learning pour optimiser la sélection des paramètres et le processus de génération de signaux.

-

Analyse de corrélation : Ajouter une analyse de corrélation avec d’autres actifs pour améliorer la stabilité et la diversification de la stratégie.

Résumé

Cette stratégie de trading par retour à la moyenne à plusieurs niveaux basée sur le RSI est un système quantitatif soigneusement conçu, combinant habilement l’analyse technique, la gestion dynamique des risques et la technique du pyramiding. En capturant les mouvements extrêmes du marché et en profitant du retour des prix, la stratégie montre un fort potentiel de rentabilité. Cependant, elle est confrontée à des défis tels que le sur-trading et la dépendance aux conditions de marché. Les futures directions d’optimisation devraient se concentrer sur l’amélioration de la capacité d’adaptation et de la gestion des risques afin de s’adapter à différents environnements de marché. Dans l’ensemble, il s’agit d’un cadre de stratégie solide qui, après des optimisations et des backtests supplémentaires, pourrait devenir un système de trading robuste.

- 1