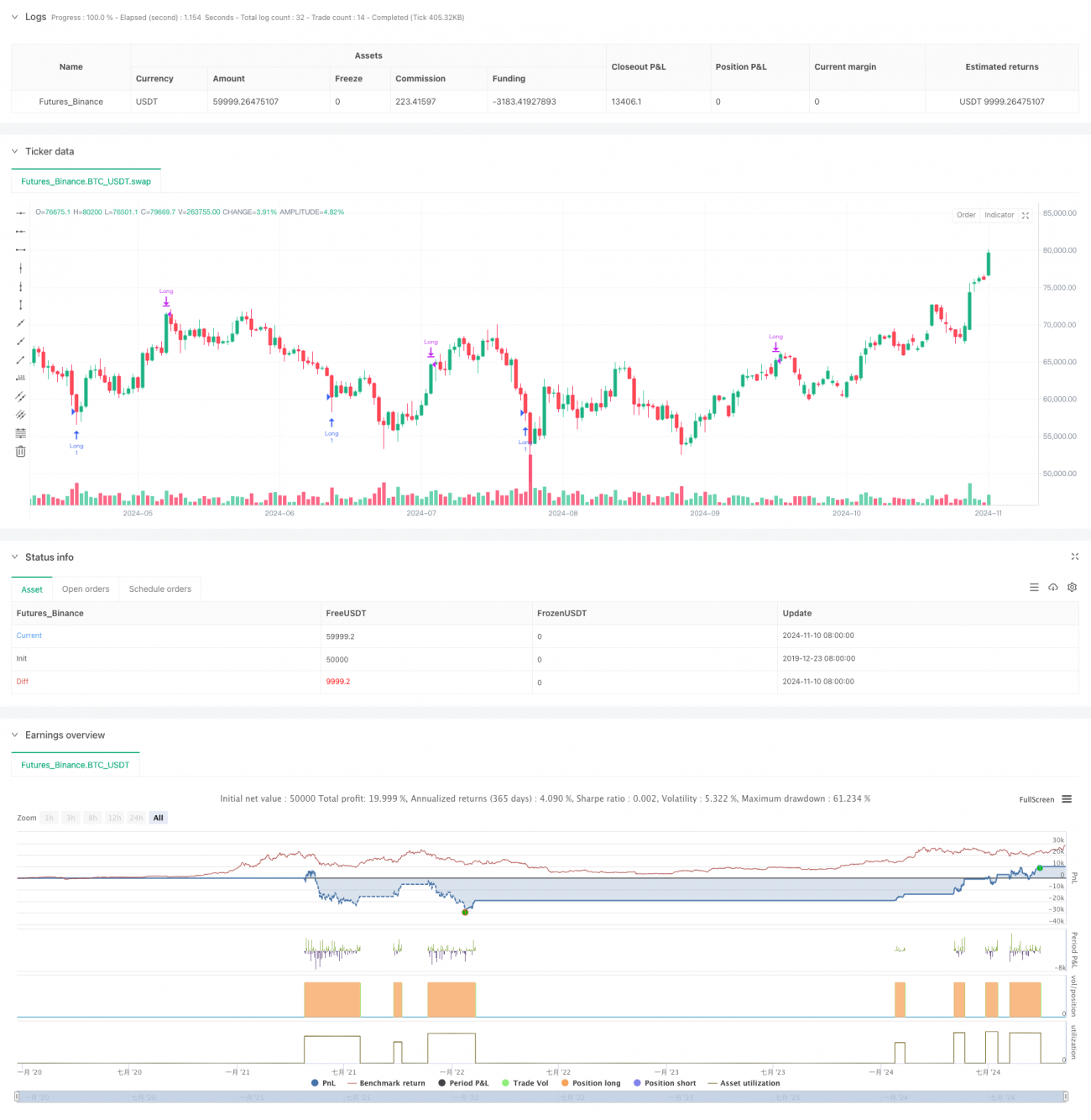

Aperçu

Cette stratégie est un système de trading complet basé sur les bandes de Bollinger, l'indicateur RSI et les moyennes mobiles. Elle identifie les opportunités de trading potentielles en utilisant la plage de fluctuation des prix des bandes de Bollinger, les niveaux de surachat/survente du RSI et le filtre de tendance EMA. Le système prend en charge les positions longues et courtes, et propose plusieurs mécanismes de sortie pour protéger le capital.

Principe de la stratégie

La stratégie repose principalement sur les composants clés suivants :

- Utilisation de bandes de Bollinger avec un écart-type de 1,8 pour déterminer la fourchette de fluctuation des prix.

- Utilisation d'un RSI sur 7 périodes pour évaluer les conditions de surachat/survente.

- Une EMA optionnelle sur 500 périodes comme filtre de tendance.

- Conditions d'entrée :

- Long : RSI inférieur à 25 et prix franchissant la bande inférieure de Bollinger.

- Short : RSI supérieur à 75 et prix franchissant la bande supérieure de Bollinger.

- Sortie basée sur un seuil RSI ou un franchissement inverse des bandes de Bollinger.

- Protection optionnelle par stop-loss en pourcentage.

Avantages de la stratégie

- La combinaison de multiples indicateurs techniques améliore la fiabilité des signaux.

- Des paramètres flexibles permettent des ajustements en fonction des différentes conditions de marché.

- Prise en charge des transactions dans les deux sens pour saisir pleinement les opportunités du marché.

- Plusieurs mécanismes de sortie adaptés à différents styles de trading.

- Le filtre de tendance réduit efficacement les faux signaux.

- Le mécanisme de stop-loss offre un bon contrôle des risques.

Risques de la stratégie

- Possibilité de faux signaux fréquents dans un marché volatil (range).

- La multiplicité des indicateurs peut entraîner un retard des signaux.

- Des seuils RSI fixes peuvent manquer de flexibilité dans différents environnements de marché.

- Les paramètres des bandes de Bollinger doivent être ajustés en fonction de la volatilité du marché.

- Le stop-loss peut être facilement déclenché lors de fluctuations violentes.

Pistes d'optimisation

- Introduire un multiplicateur adaptatif des bandes de Bollinger, ajusté dynamiquement en fonction de la volatilité du marché.

- Ajouter un indicateur de volume comme confirmation auxiliaire.

- Envisager d'ajouter un filtre temporel pour éviter les transactions à certaines périodes.

- Développer un système de seuil RSI dynamique.

- Intégrer davantage d'indicateurs de confirmation de tendance.

- Optimiser le mécanisme de stop-loss, par exemple en utilisant un stop-loss dynamique.

Conclusion

Il s'agit d'une stratégie de trading quantitatif bien conçue, qui capture les opportunités du marché grâce à la combinaison de multiples indicateurs techniques. Sa grande configurabilité lui permet de s'adapter à différents besoins de trading. Bien qu'elle présente certains risques inhérents, l'optimisation des paramètres et l'ajout d'indicateurs auxiliaires peuvent améliorer sa stabilité et sa fiabilité. Pour les investisseurs recherchant une méthode de trading systématique, c'est un cadre stratégique qui mérite d'être considéré.

- 1