Système de trading avancé de suivi de tendance par momentum à double moyenne mobile

Cette stratégie est une stratégie de suivi de tendance basée sur un système à double moyenne mobile, combinant les signaux de croisement entre une moyenne rapide et une moyenne lente, tout en introduisant une moyenne filtrante pour optimiser les points d'entrée. Grâce à une gestion de capital et un contrôle des risques, elle obtient des résultats de trading robustes.

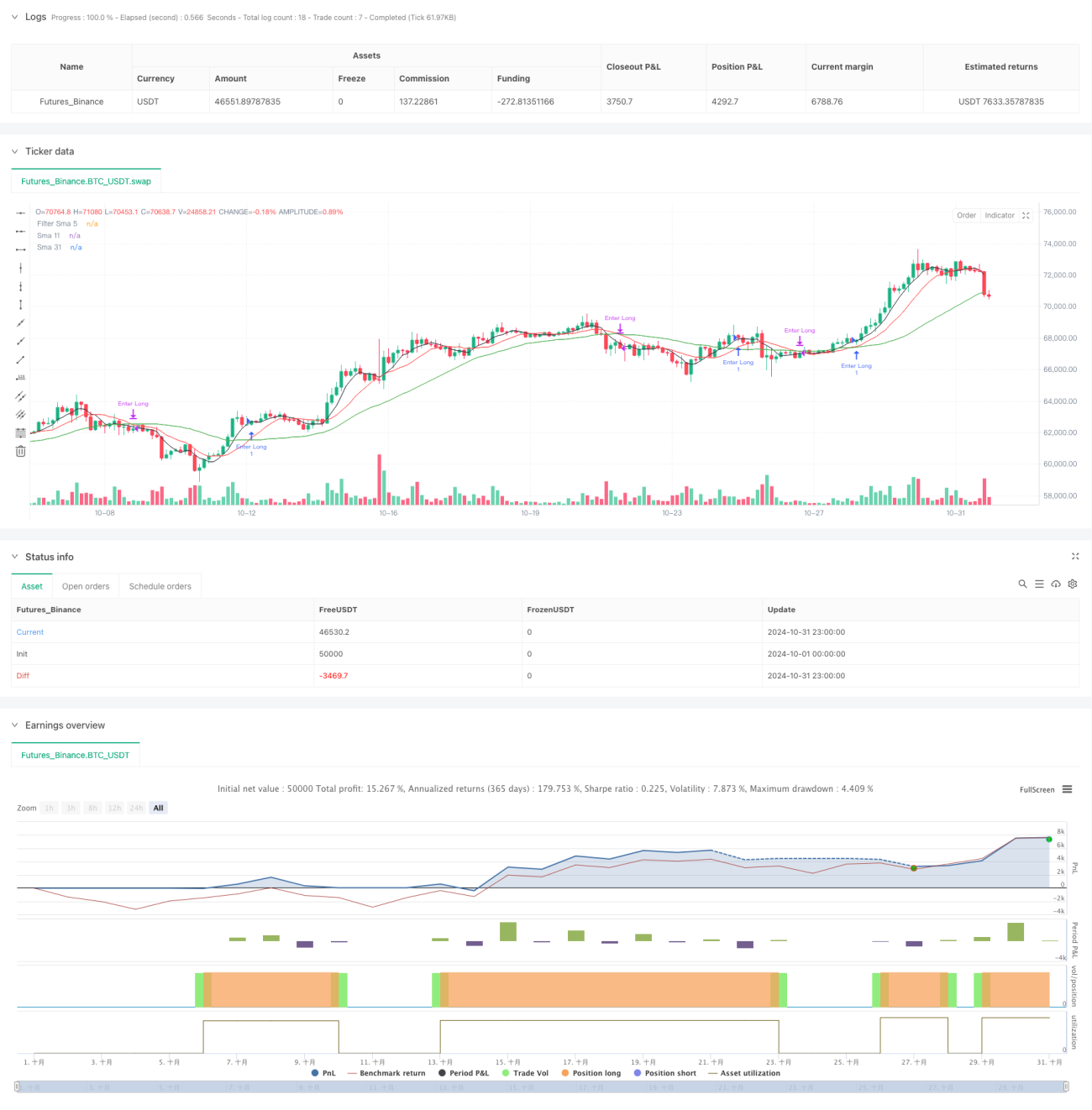

Principe de la stratégie

La stratégie utilise des moyennes mobiles simples (SMA) sur 11 et 31 périodes comme système de signal principal, tout en employant une moyenne sur 5 périodes comme filtre. Lorsque la moyenne rapide (SMA11) croise au-dessus de la moyenne lente (SMA31) et que le prix se situe au-dessus de la moyenne filtrante, le système génère un signal d'achat. Lorsque la moyenne rapide croise en dessous de la moyenne lente, la position est fermée. La stratégie utilise un montant de capital fixe pour contrôler la taille de chaque transaction, assurant ainsi une gestion des risques.

Avantages de la stratégie

- Système de signal simple et clair, facile à comprendre et à exécuter

- Confirmation par plusieurs moyennes, filtrant efficacement les faux signaux

- Utilisation d'un montant de capital fixe pour le trading, risque maîtrisé

- Bonne capacité de suivi de tendance

- Logique d'entrée et de sortie claire, réduisant l'hésitation décisionnelle

- Adaptable à différents environnements de marché

Risques de la stratégie

- Peut générer des transactions fréquentes en marché volatile

- Le système de moyennes présente un certain décalage

- Le montant fixe peut ne pas optimiser l'efficacité du capital

- N'intègre pas les variations de volatilité du marché

- Absence de stop-loss, risque de drawdown important

Pistes d'optimisation

- Introduction de périodes de moyennes adaptatives, ajustées en fonction de la volatilité du marché

- Ajout d'un filtre de volatilité, ajustement de la taille de position en cas de forte volatilité

- Conception d'un système de gestion de capital dynamique pour améliorer l'efficacité des fonds

- Intégration de mécanismes de stop-loss et de take-profit pour limiter le risque par transaction

- Prise en compte d'un indicateur de force de tendance pour optimiser les points d'entrée

- Ajout d'un filtre horaire pour éviter les périodes défavorables

Conclusion

La stratégie construit un système de suivi de tendance relativement robuste via un système à multiples moyennes mobiles. Bien qu'elle présente certaines limitations intrinsèques, des améliorations et optimisations raisonnables peuvent renforcer sa stabilité et sa rentabilité. Il est recommandé aux traders, lors de l'application en compte réel, d'ajuster les paramètres en fonction des conditions spécifiques du marché.

- 1