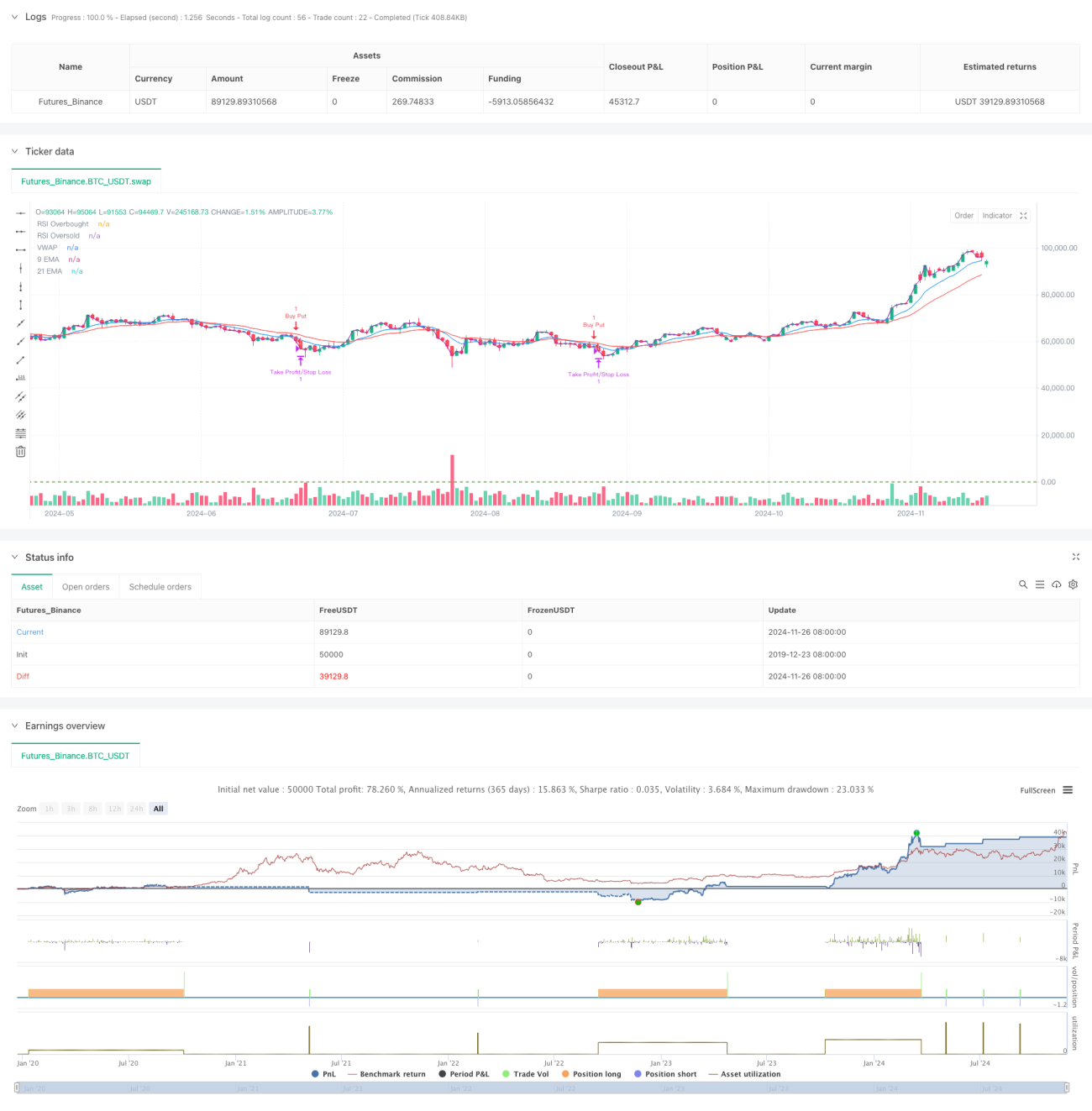

Aperçu

Cette stratégie est un système de trading haute fréquence basé sur de multiples indicateurs techniques, utilisant une échelle de temps de 5 minutes, combinant des systèmes de moyennes mobiles, des indicateurs de momentum et l'analyse du volume. La stratégie s'adapte dynamiquement à la volatilité du marché et utilise une confirmation multi-signaux pour améliorer la précision et la fiabilité des transactions. Le cœur de la stratégie réside dans la combinaison d'indicateurs techniques multidimensionnels pour capturer les tendances du marché à court terme, tout en utilisant des stop-loss dynamiques pour contrôler le risque.

Principe de la stratégie

La stratégie utilise un système de double moyenne mobile (EMA 9 et 21 périodes) comme principal outil de détermination de la tendance, combiné avec l'indicateur RSI pour la confirmation du momentum. Lorsque le prix se situe au-dessus des deux moyennes mobiles et que le RSI est dans la zone 40-65, le système cherche des opportunités d'achat ; lorsque le prix se situe en dessous des deux moyennes mobiles et que le RSI est dans la zone 35-60, le système cherche des opportunités de vente. Parallèlement, la stratégie intègre un mécanisme de confirmation par le volume, exigeant que le volume actuel soit supérieur à 1,2 fois la moyenne mobile du volume sur 20 périodes. L'utilisation du VWAP garantit en outre que la direction des transactions reste alignée sur la tendance intraday dominante.

Avantages de la stratégie

- Le mécanisme de confirmation multi-signaux améliore considérablement la fiabilité des transactions.

- Les niveaux dynamiques de take-profit et stop-loss s'adaptent à différents environnements de marché.

- Les seuils RSI relativement conservateurs évitent de trader dans des zones extrêmes.

- Le mécanisme de confirmation par le volume filtre efficacement les faux signaux.

- L'utilisation du VWAP aide à garantir que la direction des transactions est alignée avec les flux de capitaux dominants.

- Le système de moyennes mobiles à réponse rapide est adapté à la capture des opportunités de marché à court terme.

Risques de la stratégie

- En marché latéral avec consolidation, des faux signaux fréquents peuvent se produire.

- Les conditions multiples peuvent entraîner le manque de certaines opportunités de trading.

- Le trading haute fréquence peut faire face à des coûts de transaction élevés.

- La stratégie peut réagir lentement en cas de retournement rapide du marché.

- Des exigences élevées en temps réel concernant les données de marché.

Pistes d'optimisation de la stratégie

- Introduire un mécanisme d'ajustement adaptatif des paramètres, permettant à la stratégie d'ajuster dynamiquement les paramètres des indicateurs en fonction de l'état du marché.

- Ajouter un module de reconnaissance de l'environnement de marché, adoptant différentes stratégies de trading selon les conditions du marché.

- Optimiser le filtre de volume, en envisageant l'utilisation du volume relatif ou de l'analyse du profil de volume.

- Améliorer le mécanisme de stop-loss, en envisageant l'ajout d'une fonction de trailing stop.

- Ajouter un filtre horaire pour éviter les périodes de forte volatilité à l'ouverture et à la fermeture.

Conclusion

Cette stratégie construit un système de trading relativement complet grâce à la combinaison de multiples indicateurs techniques. Ses atouts résident dans son mécanisme de confirmation multi-dimensionnelle et sa méthode dynamique de gestion des risques. Bien qu'il existe certains risques potentiels, une optimisation raisonnable des paramètres et une gestion des risques permettent à la stratégie de conserver une bonne valeur d'application. Il est recommandé aux traders de procéder à des backtests approfondis avant une utilisation en live, et d'ajuster les paramètres en fonction des conditions spécifiques du marché.

- 1