Stratégie de trading de momentum avec breakout de tendance ADX

Aperçu

Il s'agit d'une stratégie de trading quantitative basée sur l'indicateur de mouvement directionnel moyen (ADX) et les cassures de prix. Cette stratégie évalue principalement la force de la tendance du marché en surveillant la valeur de l'indicateur ADX, et capture le momentum du marché en combinant les signaux de cassure de prix. La stratégie est conçue pour fonctionner pendant des créneaux horaires spécifiques et met en œuvre la gestion des risques via un stop-loss et une limitation du nombre de transactions quotidiennes.

Principe de la stratégie

La logique centrale de la stratégie comprend les éléments clés suivants :

- Surveillance de l'ADX : utilisation de l'indicateur ADX pour évaluer la force de la tendance du marché. Lorsque la valeur ADX est inférieure à 17,5, cela indique qu'une nouvelle tendance est sur le point de se former.

- Identification de cassure de prix : la stratégie suit le plus haut cours de clôture des 34 dernières périodes. Lorsque le prix actuel dépasse ce niveau de résistance, un signal de transaction est déclenché.

- Gestion des horaires de trading : la stratégie ne fonctionne que pendant les créneaux horaires spécifiés (0730-1430) afin d'éviter les risques liés aux périodes de faible liquidité.

- Mécanismes de contrôle des risques :

- Fixation d'un stop-loss en dollars pour limiter les pertes par transaction.

- Limitation à trois transactions maximum par créneau horaire.

- Clôture automatique de toutes les positions à la fin du créneau horaire.

Avantages de la stratégie

- Capacité de capture de tendance : en combinant l'ADX et les cassures de prix, la stratégie identifie efficacement les premières phases des tendances du marché.

- Gestion des risques complète : elle intègre plusieurs niveaux de mesures de contrôle des risques, comme le stop-loss fixe, la limitation du nombre de transactions et le mécanisme de clôture automatique.

- Haut niveau d'automatisation : la logique de la stratégie est claire et entièrement automatisée, sans nécessité d'intervention manuelle.

- Adaptabilité : les paramètres (montant du stop-loss, période de rétrospective, etc.) peuvent être ajustés en fonction des différentes conditions de marché.

Risques de la stratégie

- Risque de fausse cassure : dans un marché en range, des faux signaux de cassure peuvent entraîner des stop-loss successifs.

- Dépendance aux paramètres : l'efficacité de la stratégie dépend fortement du seuil ADX et de la période de rétrospective choisis.

- Limitation des horaires : le trading limité à des créneaux spécifiques peut faire manquer des opportunités en dehors de ces périodes.

- Stop-loss fixe : un stop-loss en dollars fixes peut manquer de flexibilité dans des environnements de volatilité variable.

Pistes d'optimisation de la stratégie

- Stop-loss dynamique : remplacer le stop-loss fixe par un stop-loss basé sur l'ATR pour s'adapter aux différentes conditions de volatilité.

- Filtre d'environnement de marché : ajouter un filtre de volatilité pour ajuster ou suspendre les transactions en cas de forte volatilité.

- Amélioration de l'entrée : envisager d'ajouter une confirmation de volume pour renforcer la fiabilité des signaux de cassure.

- Ajustement dynamique des paramètres : mettre en place un mécanisme d'adaptation automatique du seuil ADX et de la période de rétrospective.

Résumé

Il s'agit d'une stratégie de suivi de tendance à la structure complète et à la logique claire. En combinant l'ADX et les cassures de prix, elle capture les opportunités de tendance dans un cadre de gestion des risques efficace. Bien qu'il existe des possibilités d'optimisation, le cadre de base de la stratégie est solide et peut servir de composant fondamental pour un système de trading quantitatif. Il est recommandé aux traders d'effectuer des backtests approfondis et une optimisation des paramètres avant le passage en live, et d'adapter la stratégie aux conditions spécifiques du marché.

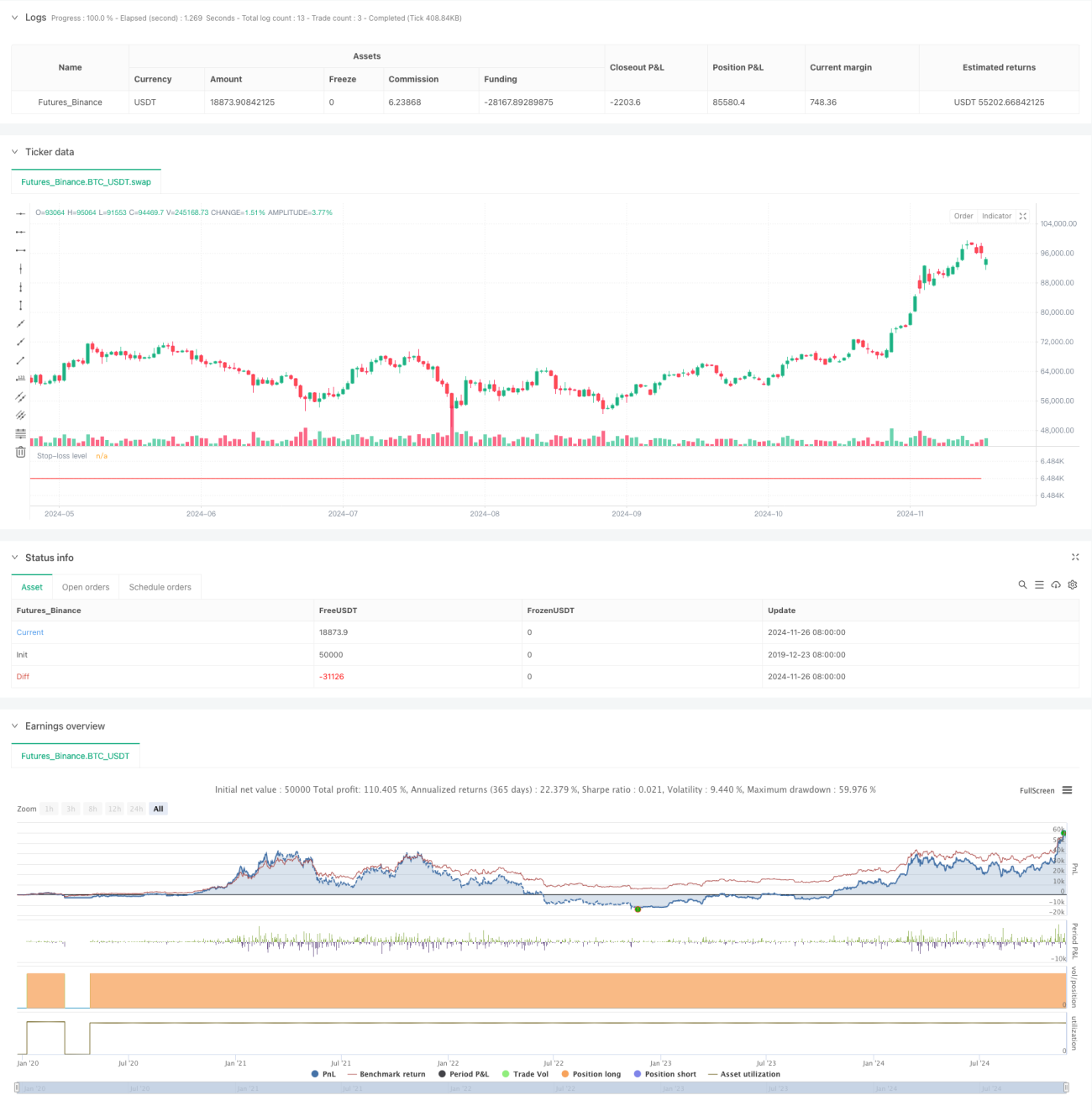

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-27 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HuntGatherTrade

// ========================

// NQ 30 minute, ES 30 minute- 1