Stratégie de suivi de tendance avec paramétrage adaptatif KNN

Aperçu

Cette stratégie est un système de suivi de tendance paramétrique adaptatif basé sur l'algorithme d'apprentissage automatique des k-plus proches voisins (KNN). La stratégie ajuste dynamiquement les paramètres de suivi de tendance à l'aide de l'algorithme KNN et génère des signaux de trading en combinaison avec des moyennes mobiles. Le système est capable d'ajuster automatiquement les paramètres de la stratégie en fonction des changements de l'environnement du marché, améliorant ainsi son adaptabilité et sa stabilité. Cette stratégie utilise des méthodes d'apprentissage automatique pour optimiser les stratégies de suivi de tendance traditionnelles, représentant une fusion de la technologie et de l'innovation dans le domaine de l'investissement quantitatif.

Principe de la stratégie

Le principe central de la stratégie consiste à utiliser l'algorithme KNN pour analyser les données de prix historiques, en prédisant l'évolution des prix par le calcul de la similarité entre l'état actuel du marché et les données historiques. Les étapes de mise en œuvre spécifiques sont les suivantes :

- Définir la taille de la fenêtre d'observation et la valeur K, collecter les données de prix historiques pour former un vecteur de caractéristiques.

- Calculer la distance euclidienne entre la séquence de prix actuelle et les données historiques.

- Sélectionner les K séquences de prix historiques les plus similaires comme échantillons voisins.

- Analyser les variations de prix ultérieures de ces K échantillons voisins.

- En combinaison avec la moyenne mobile, générer des signaux de trading en fonction de la variation moyenne des prix des échantillons voisins.

Lorsque la variation moyenne des prix des K échantillons voisins est positive et que le prix actuel se situe au-dessus de la moyenne mobile, le système génère un signal d'achat ; à l'inverse, il génère un signal de vente.

Avantages de la stratégie

- Forte adaptabilité : L'algorithme KNN peut ajuster automatiquement les paramètres en fonction des changements de l'environnement du marché, conférant à la stratégie une grande adaptabilité.

- Analyse multidimensionnelle : Combine des algorithmes d'apprentissage automatique et des indicateurs techniques, offrant une perspective d'analyse de marché plus complète.

- Gestion des risques raisonnable : Utilise la moyenne mobile comme confirmation auxiliaire, réduisant l'impact des faux signaux.

- Logique de calcul claire : Le processus d'exécution de la stratégie est transparent, facile à comprendre et à optimiser.

- Paramètres flexibles et ajustables : Permet d'ajuster des paramètres tels que la valeur K et la taille de la fenêtre en fonction des différents environnements de marché.

Risques de la stratégie

- Complexité de calcul élevée : L'algorithme KNN nécessite le calcul d'une grande quantité de données historiques, ce qui peut affecter l'efficacité d'exécution de la stratégie.

- Sensibilité aux paramètres : Le choix de la valeur K et de la taille de la fenêtre a un impact significatif sur les performances de la stratégie.

- Dépendance à l'environnement du marché : Dans des conditions de marché fortement volatiles, la valeur de référence de la similarité historique peut diminuer.

- Risque de surajustement : Une trop grande dépendance aux données historiques peut entraîner un surajustement de la stratégie.

- Risque de retard : En raison de la nécessité de collecter suffisamment de données historiques, il peut y avoir un décalage dans les signaux.

Directions d'optimisation de la stratégie

-

Optimisation de l'ingénierie des caractéristiques :

- Ajouter davantage d'indicateurs techniques comme caractéristiques.

- Introduire des indicateurs de sentiment du marché.

- Optimiser les méthodes de normalisation des caractéristiques.

-

Amélioration de l'efficacité algorithmique :

- Utiliser des structures de données comme les arbres KD pour optimiser la recherche des voisins.

- Mettre en œuvre le calcul parallèle.

- Optimiser le stockage et l'accès aux données.

-

Renforcement du contrôle des risques :

- Ajouter des mécanismes de stop-loss et de take-profit.

- Introduire un filtre de volatilité.

- Concevoir un système de gestion dynamique des positions.

-

Programme d'optimisation des paramètres :

- Mettre en œuvre une sélection adaptative de la valeur K.

- Ajuster dynamiquement la taille de la fenêtre d'observation.

- Optimiser la période de la moyenne mobile.

-

Amélioration du mécanisme de génération des signaux :

- Introduire un système de notation de l'intensité des signaux.

- Concevoir un mécanisme de confirmation des signaux.

- Optimiser les moments d'entrée et de sortie.

Résumé

Cette stratégie applique de manière innovante l'algorithme KNN au trading de suivi de tendance, optimisant les stratégies d'analyse technique traditionnelles par des méthodes d'apprentissage automatique. La stratégie possède une forte adaptabilité et flexibilité, lui permettant d'ajuster dynamiquement ses paramètres en fonction de l'environnement du marché. Bien qu'elle présente des risques tels qu'une complexité de calcul élevée et une sensibilité aux paramètres, elle conserve une bonne valeur d'application grâce à des mesures d'optimisation et de contrôle des risques appropriées. Il est recommandé aux investisseurs, dans la pratique, d'ajuster les paramètres en fonction des caractéristiques du marché et de combiner d'autres méthodes d'analyse pour prendre des décisions de trading.

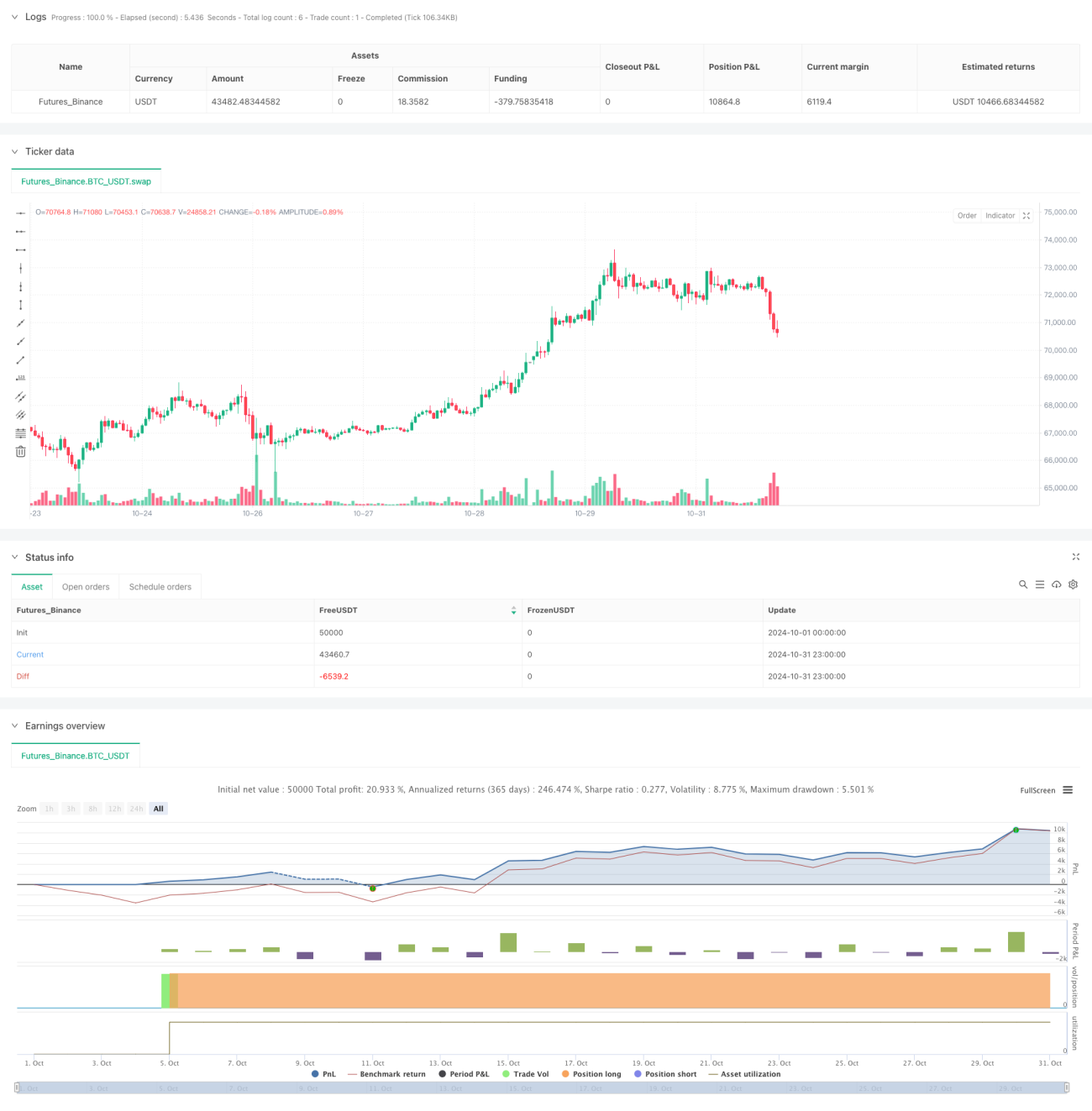

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Trend Following Strategy with KNN", overlay=true,commission_value=0.03,currency='USD', commission_type=strategy.commission.percent,default_qty_type=strategy.cash)

- 1