Stratégie adaptative hybride à double moyenne mobile et force relative

Aperçu

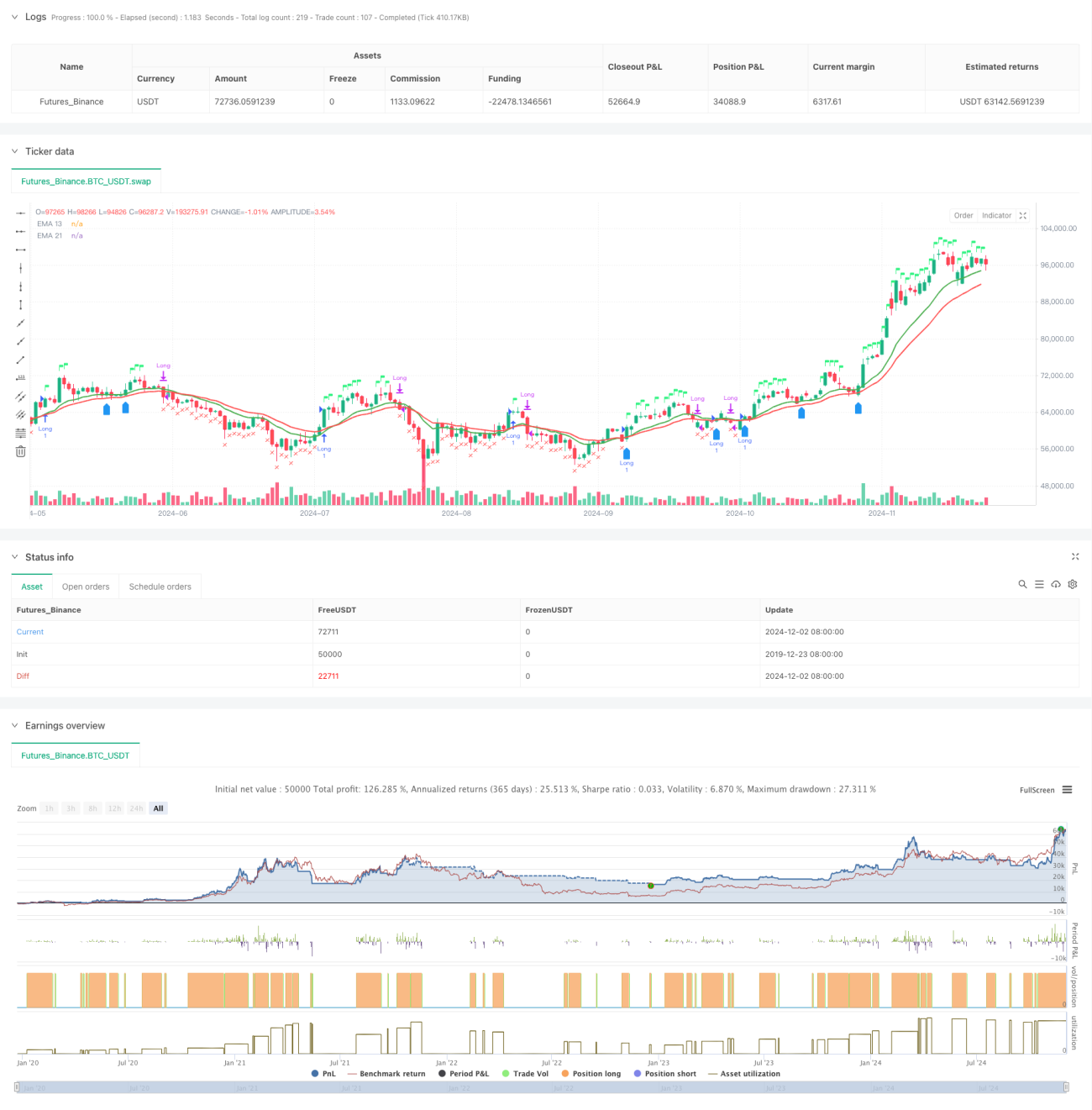

Cette stratégie est un système de trading complet combinant un système de double moyenne mobile, l'indice de force relative (RSI) et une analyse de force relative (RS). Elle confirme la tendance via le croisement des moyennes mobiles exponentielles (EMA) sur 13 et 21 périodes, tout en intégrant le RSI et la valeur de RS par rapport à un indice de référence pour valider les signaux de trading, établissant ainsi un mécanisme de décision multidimensionnel. La stratégie comprend également un mécanisme de contrôle des risques basé sur le plus haut sur 52 semaines et l'évaluation des conditions de ré-entrée.

Principe de la stratégie

La stratégie utilise un mécanisme de confirmation multi-signaux :

- Les signaux d'entrée doivent simultanément remplir les conditions suivantes :

- L'EMA13 croise au-dessus de l'EMA21 ou le prix est supérieur à l'EMA13

- Le RSI est supérieur à 60

- La force relative (RS) est positive

- Les conditions de sortie incluent :

- Le prix passe sous l'EMA21

- Le RSI descend en dessous de 50

- La RS devient négative

- Conditions de ré-entrée :

- Le prix croise au-dessus de l'EMA13 et l'EMA13 est supérieure à l'EMA21

- La RS reste positive

- Ou le prix dépasse le plus haut de la semaine précédente

Avantages de la stratégie

- Le mécanisme de confirmation multi-signaux réduit les risques de fausse cassure

- L'analyse de force relative permet de filtrer efficacement les instruments forts

- Utilisation d'un mécanisme d'ajustement de période adaptatif

- Système de contrôle des risques complet

- Mécanisme de ré-entrée intelligent

- Visualisation en temps réel de l'état des transactions

Risques de la stratégie

- Des marchés en range peuvent générer des transactions fréquentes

- La dépendance à plusieurs indicateurs peut entraîner un retard des signaux

- Un seuil fixe pour le RSI peut ne pas convenir à tous les environnements de marché

- Le calcul de la force relative dépend de la précision de l'indice de référence

- Le stop-loss basé sur le plus haut sur 52 semaines peut être trop large

Pistes d'optimisation

- Introduire un seuil RSI adaptatif

- Optimiser la logique de jugement des conditions de ré-entrée

- Ajouter une dimension d'analyse du volume de transactions

- Améliorer le mécanisme de prise de bénéfices et stop-loss

- Intégrer un filtre de volatilité

- Optimiser la période de calcul de la force relative

Conclusion

Cette stratégie construit un système de trading complet en combinant l'analyse technique et l'analyse de force relative. Son mécanisme de confirmation multi-signaux et son système de contrôle des risques lui confèrent une forte utilité pratique. Via les pistes d'optimisation suggérées, la stratégie dispose encore d'un potentiel d'amélioration. Sa mise en œuvre réussie nécessite une compréhension approfondie du marché de la part du trader, ainsi que des ajustements de paramètres appropriés en fonction des caractéristiques spécifiques de l'instrument traité.

- 1