Aperçu

Cette stratégie est un système de trading avancé basé sur l'analyse des points pivots, qui anticipe les retournements de tendance potentiels en identifiant les points de retournement clés du marché. La stratégie adopte une approche innovante de « pivot des pivots », combinée à l'indicateur de volatilité ATR pour la gestion des positions, formant ainsi un système de trading complet. Cette stratégie est applicable à plusieurs marchés et ses paramètres peuvent être optimisés en fonction des caractéristiques de chaque marché.

Principe de la stratégie

Le cœur de la stratégie consiste à identifier les opportunités de retournement de marché via une analyse des points pivots à deux niveaux. Le premier niveau est celui des points hauts et bas fondamentaux, tandis que le second niveau filtre les points de retournement significatifs parmi ces premiers pivots. Lorsque le prix franchit ces niveaux clés, le système génère des signaux de trading. Parallèlement, la stratégie utilise l'indicateur ATR pour mesurer la volatilité du marché, afin de déterminer les niveaux de stop-loss et de take-profit, ainsi que la taille des positions.

Avantages de la stratégie

- Adaptabilité : La stratégie peut s'adapter à différents environnements de marché en ajustant ses paramètres en fonction des niveaux de volatilité.

- Gestion des risques complète : L'utilisation de l'ATR pour un stop-loss dynamique permet d'ajuster automatiquement les mesures de protection en fonction de la volatilité du marché.

- Confirmation multi-niveaux : L'analyse à deux niveaux de pivots réduit le risque de faux signaux de rupture.

- Gestion flexible des positions : La taille des positions est ajustée dynamiquement en fonction de la taille du compte et de la volatilité du marché.

- Règles d'entrée claires : Un mécanisme de confirmation de signal précis limite les jugements subjectifs.

Risques de la stratégie

- Risque de slippage : En cas de forte volatilité, le slippage peut être important.

- Risque de faux signaux : Pendant les phases de congestion, des signaux erronés peuvent survenir.

- Risque de surendettement : Un effet de levier inapproprié peut entraîner des pertes sévères.

- Risque d'optimisation excessive : Une optimisation trop poussée peut conduire à un surajustement.

Pistes d'optimisation de la stratégie

- Filtrage des signaux : Ajouter un filtre de tendance pour ne trader que dans la direction de la tendance principale.

- Paramètres dynamiques : Ajuster automatiquement les paramètres des points pivots en fonction des conditions de marché.

- Multiples périodes : Renforcer la confirmation en utilisant plusieurs horizons temporels pour améliorer la précision.

- Stop-loss intelligent : Développer des stratégies de stop-loss plus sophistiquées, comme le trailing stop.

- Contrôle des risques : Ajouter davantage de mesures de contrôle des risques, telles que l'analyse de corrélation.

Résumé

Il s'agit d'une stratégie de retournement de tendance bien conçue, qui construit un système de trading robuste grâce à une analyse des points pivots à deux niveaux et une gestion de la volatilité via l'ATR. Ses atouts résident dans sa grande adaptabilité et une gestion des risques complète. Néanmoins, le trader doit utiliser l'effet de levier avec prudence et optimiser les paramètres en continu. Les pistes d'optimisation suggérées offrent encore des possibilités d'amélioration. Cette stratégie convient aux traders prudents et constitue un système de trading méritant une étude et une mise en pratique approfondies.

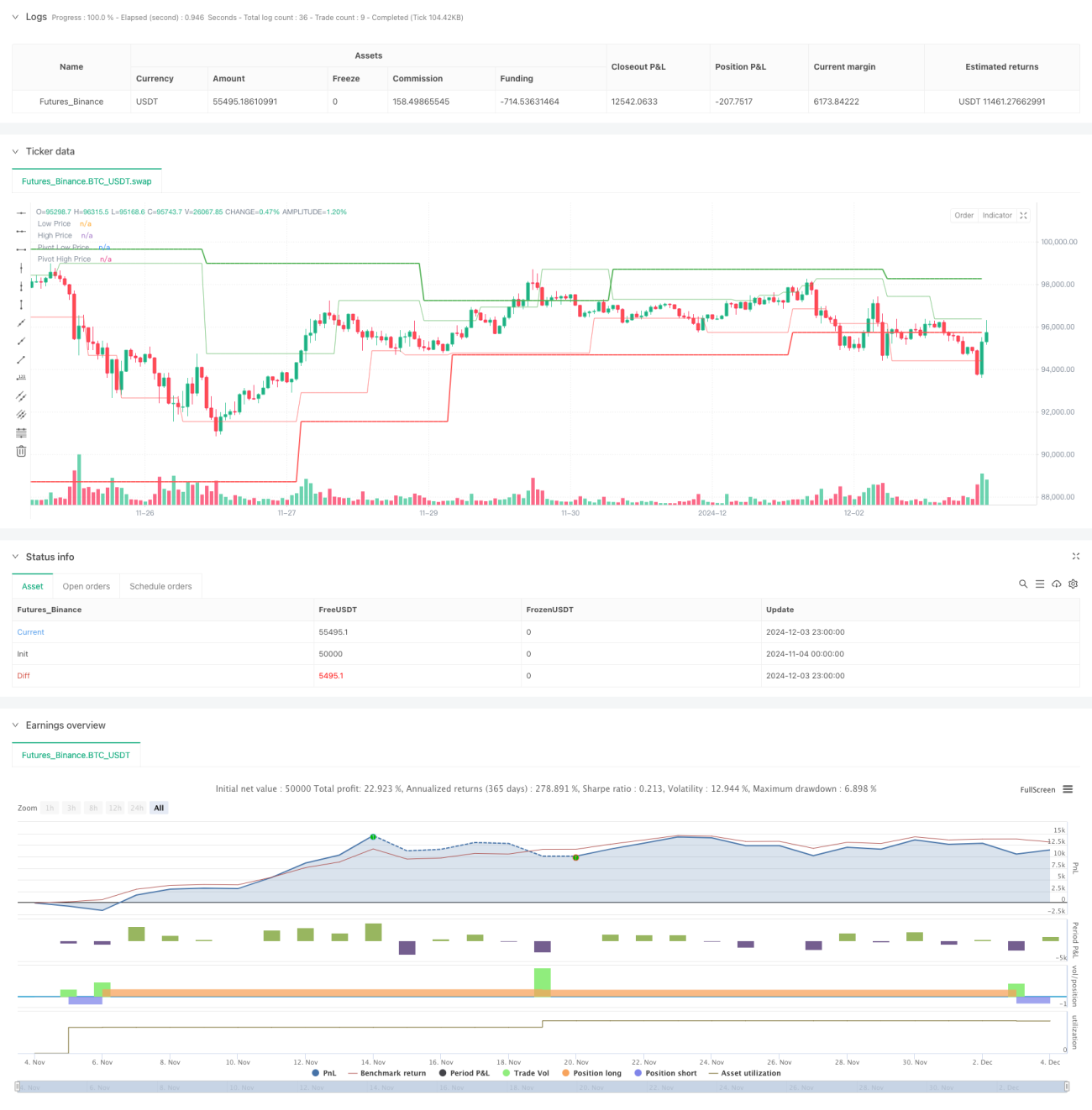

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Pivot of Pivot Reversal Strategy [MAD]", shorttitle="PoP Reversal Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

// Inputs with Tooltips- 1