Ce système est un système de trading quantitatif basé sur l'oscillateur dynamique RSI. En effectuant un ajustement polynomial et une analyse de séries temporelles sur l'indicateur RSI, il calcule le taux de variation du RSI pour capturer le momentum du marché. La stratégie utilise des méthodes mathématiques avancées telles que la décomposition QR pour le traitement des signaux, et combine un système de moyennes mobiles pour les décisions de trading.

Principe de la stratégie

Le cœur de la stratégie est l'oscillateur Delta-RSI, qui fonctionne comme suit :

- Calculer d'abord le RSI traditionnel comme données de base.

- Utiliser un ajustement polynomial pour lisser le RSI et réduire le bruit.

- Calculer la dérivée temporelle du RSI pour obtenir le Delta-RSI, reflétant le taux de variation du RSI.

- Comparer le Delta-RSI avec sa moyenne mobile pour générer des signaux de trading.

- Utiliser l'erreur quadratique moyenne (RMSE) pour évaluer et filtrer la qualité de l'ajustement.

Les signaux de trading peuvent être générés de trois manières :

- Passage par zéro : Long quand le Delta-RSI passe de négatif à positif, short quand il passe de positif à négatif.

- Croisement de la ligne de signal : Long quand le Delta-RSI croise sa moyenne mobile à la hausse, short à la baisse.

- Changement de direction : Long quand le Delta-RSI commence à augmenter en zone négative, short quand il commence à baisser en zone positive.

Avantages de la stratégie

- Base mathématique solide : Utilisation de méthodes mathématiques avancées comme la décomposition QR pour le traitement des signaux, base théorique fiable.

- Lissage des signaux : L'ajustement polynomial filtre efficacement le bruit du marché, améliorant la qualité des signaux.

- Grande flexibilité : Plusieurs modes de génération de signaux et choix de paramètres, adaptés à différents environnements de marché.

- Risque contrôlable : Intègre un mécanisme de filtrage RMSE pour sélectionner les signaux les plus fiables.

- Calcul efficace : Les opérations matricielles utilisent des algorithmes optimisés, assurant une bonne efficacité.

Risques de la stratégie

- Sensibilité aux paramètres : Plusieurs paramètres clés nécessitent un réglage minutieux ; un mauvais choix peut gravement affecter les performances.

- Retard : Le lissage des signaux introduit un certain décalage, pouvant faire manquer des mouvements rapides.

- Fausses cassures : Dans des marchés oscillants, des signaux erronés peuvent apparaître, augmentant les coûts de transaction.

- Complexité de calcul : Implique de nombreuses opérations matricielles, pouvant créer des goulots d'étranglement en trading haute fréquence.

- Surapprentissage : Lors de l'optimisation des paramètres, il faut éviter de surajuster aux données historiques.

Pistes d'optimisation de la stratégie

- Paramètres adaptatifs : Ajuster dynamiquement la période RSI et l'ordre de l'ajustement en fonction de la volatilité du marché.

- Multi-périodes : Combiner des signaux de plusieurs périodes pour une validation croisée.

- Filtre de volatilité : Ajouter des indicateurs de volatilité comme l'ATR pour filtrer les signaux.

- Classification du marché : Utiliser différentes règles de génération de signaux selon l'état du marché (tendance/oscillation).

- Optimisation du stop-loss : Intégrer des mécanismes de stop-loss plus intelligents, comme des stop-loss dynamiques basés sur des niveaux de support/résistance.

Conclusion

Il s'agit d'une stratégie de trading quantitatif à la structure solide et aux fondements théoriques robustes. En analysant la dynamique du RSI et en utilisant des méthodes mathématiques modernes pour le traitement des signaux, elle parvient bien à capturer les tendances du marché. Bien qu'elle présente une certaine sensibilité aux paramètres et une complexité de calcul, avec un choix de paramètres judicieux et des améliorations, cette stratégie a une bonne valeur d'application. Il est recommandé, en utilisation réelle, de veiller au contrôle des risques, de gérer la taille des positions de manière appropriée et de surveiller en permanence les performances de la stratégie.

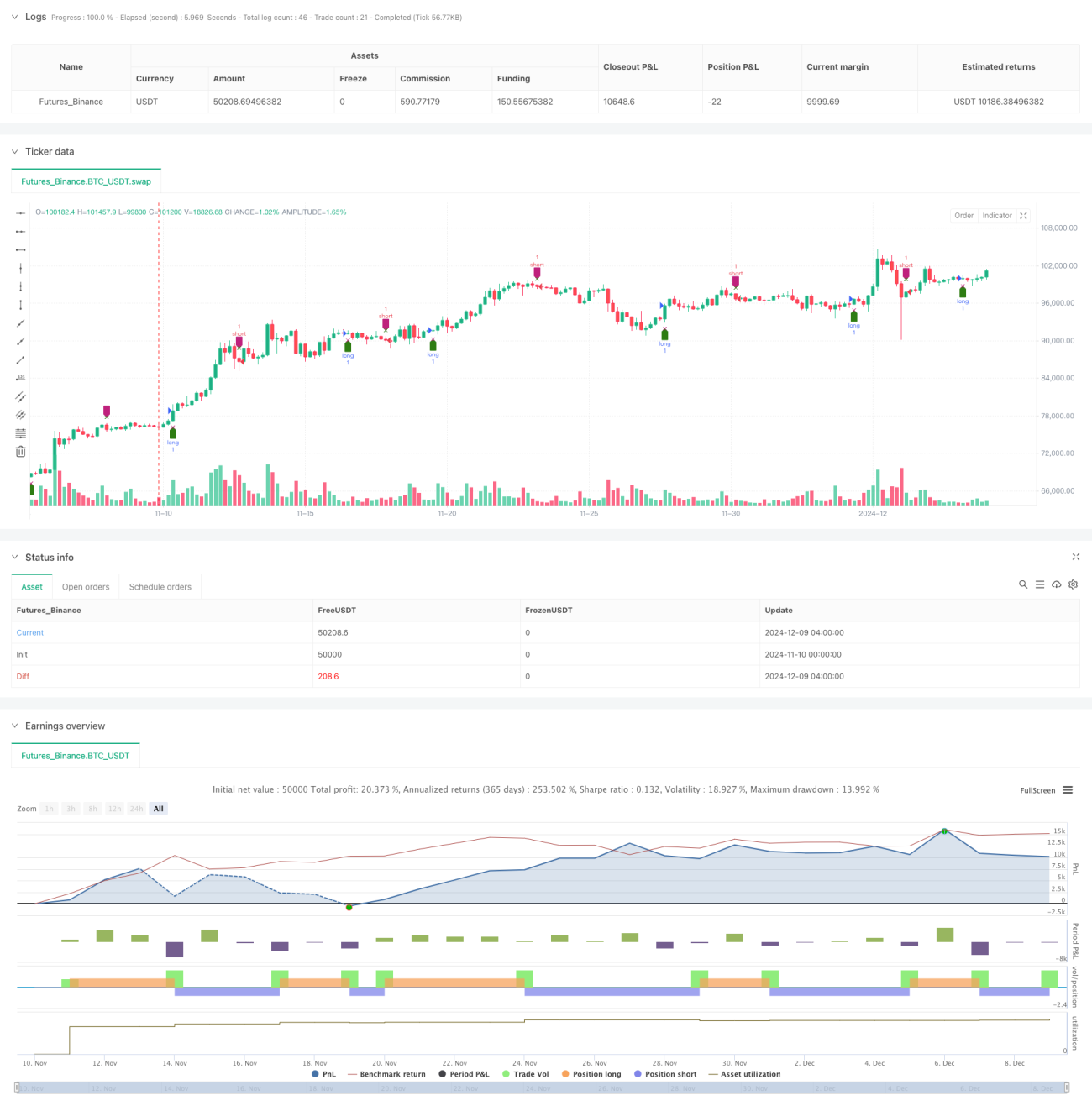

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tbiktag

//

// Delta-RSI Oscillator Strategy- 1