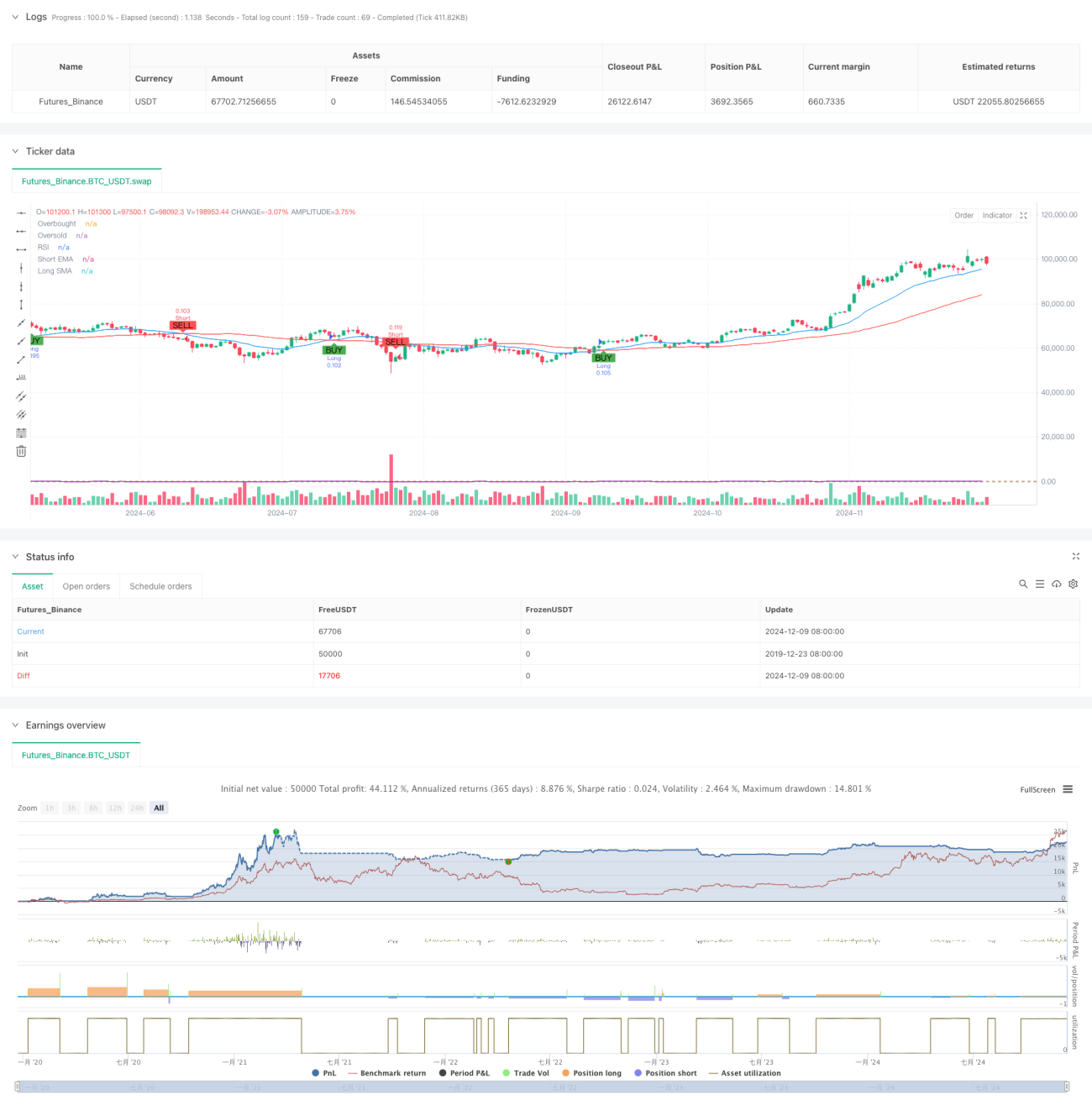

Aperçu

Cette stratégie est une stratégie de trading basée sur les fluctuations techniques, combinant des signaux multiples tels que le croisement de moyennes mobiles, les conditions de surachat/survente du RSI et les stop loss/take profit basés sur l'ATR. Le cœur de la stratégie consiste à capter les tendances du marché via le croisement d’une EMA courte et d’une SMA longue, tout en utilisant l’indicateur RSI pour confirmer les signaux, et en fixant dynamiquement les niveaux de stop loss et de take profit grâce à l’ATR. La stratégie prend en charge les trades long et short, et peut activer ou désactiver chaque direction de manière flexible selon les préférences de l’utilisateur.

Principe de la stratégie

La stratégie construit un système de trading en combinant plusieurs couches d’indicateurs techniques :

- Couche de détection de tendance : utilise le croisement entre une EMA 20 périodes et une SMA 50 périodes pour déterminer la direction de la tendance. Un passage de l’EMA au-dessus de la SMA constitue un signal haussier, et en dessous un signal baissier.

- Couche de confirmation de momentum : utilise l’indicateur RSI pour détecter les conditions de surachat/survente. Le trading long est autorisé lorsque le RSI est inférieur à 70, et le trading short lorsqu’il est supérieur à 30.

- Couche de calcul de volatilité : utilise l’ATR 14 périodes pour calculer les niveaux de stop loss et de take profit. Le stop loss est fixé à 1,5 fois l’ATR et le take profit à 3 fois l’ATR.

- Couche de gestion de position : calcule dynamiquement la taille de la position en fonction du capital initial et du pourcentage de risque par trade (1 % par défaut).

Avantages de la stratégie

- Confirmation multi-signaux : la combinaison du croisement des moyennes mobiles, du RSI et de l’ATR réduit efficacement les signaux erronés.

- Stop loss et take profit dynamiques : les niveaux de stop et de profit s’ajustent dynamiquement en fonction de l’ATR, s’adaptant mieux aux variations de volatilité du marché.

- Flexibilité directionnelle : possibilité d’activer uniquement les trades longs ou shorts en fonction de l’environnement de marché.

- Gestion stricte des risques : un contrôle de risque basé sur un pourcentage et une gestion dynamique de la position limitent efficacement l’exposition de chaque trade.

- Support visuel : la stratégie offre un support graphique complet incluant les marqueurs de signaux et l’affichage des indicateurs.

Risques de la stratégie

- Risque en marché range : dans un marché sans tendance, les croisements de moyennes mobiles peuvent générer de nombreux faux signaux.

- Risque de glissement : lors de périodes de forte volatilité, le prix d’exécution réel peut s’écarter significativement du prix du signal.

- Risque de gestion de capital : un pourcentage de risque trop élevé peut entraîner une perte unitaire excessive.

- Sensibilité aux paramètres : la performance de la stratégie est sensible aux réglages des paramètres, nécessitant un réglage minutieux.

Pistes d’optimisation

- Ajouter un filtre de force de tendance : intégrer l’indicateur ADX pour filtrer les signaux dans les environnements de tendance faible.

- Optimiser les périodes des moyennes mobiles : ajuster dynamiquement les paramètres des moyennes selon les caractéristiques des cycles de marché.

- Améliorer le mécanisme de stop loss : ajouter un stop suiveur pour mieux protéger les gains.

- Ajouter une confirmation de volume : inclure un indicateur de volume comme confirmation auxiliaire pour accroître la fiabilité des signaux.

- Classification de l’environnement de marché : intégrer un module de reconnaissance de l’environnement de marché pour utiliser différentes combinaisons de paramètres selon les conditions.

Résumé

Cette stratégie construit un système de trading relativement complet grâce à la combinaison de plusieurs indicateurs techniques. Ses principaux atouts sont la fiabilité de la confirmation des signaux et l’intégrité de la gestion des risques, mais il faut tenir compte de l’impact de l’environnement de marché sur ses performances. En suivant les pistes d’optimisation suggérées, la stratégie dispose d’une marge d’amélioration significative. En utilisation réelle, il est recommandé de procéder à des tests de paramètres approfondis et à une validation par backtest.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © CryptoRonin84

//@version=5- 1