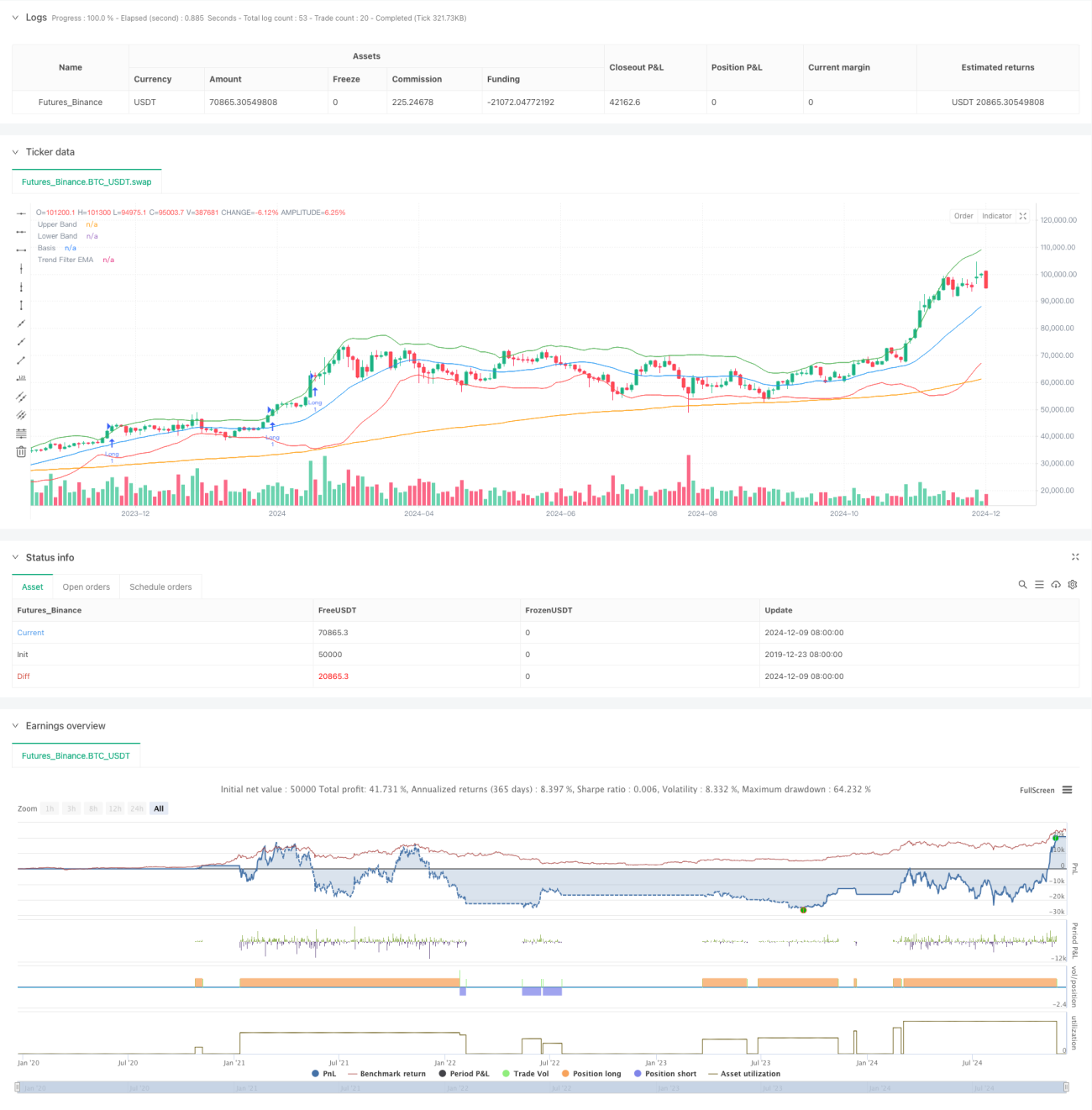

Aperçu

Cette stratégie est un système de trading quantitatif avancé qui combine les bandes de Bollinger, l'indicateur RSI et un filtre de tendance EMA à 200 périodes. Grâce à la coordination de multiples indicateurs techniques, elle capture des opportunités de cassure à forte probabilité dans le sens de la tendance tout en filtrant efficacement les faux signaux sur les marchés sans tendance. Le système utilise un stop-loss dynamique et des objectifs de profit basés sur un ratio risque/rendement, visant à obtenir des performances de trading robustes.

Principe de la stratégie

La logique centrale de la stratégie repose sur trois niveaux :

- Signal de cassure des bandes de Bollinger : Les bandes supérieure et inférieure servent de canaux de volatilité. Une cassure au-dessus de la bande supérieure est un signal d'achat, une cassure en dessous de la bande inférieure est un signal de vente.

- Confirmation de momentum RSI : Un RSI supérieur à 50 confirme un momentum haussier, un RSI inférieur à 50 confirme un momentum baissier, évitant de trader en l'absence de tendance.

- Filtre de tendance EMA : L'EMA à 200 périodes détermine la tendance principale et on n'ouvre de position que dans le sens de cette tendance. On achète si le prix est au-dessus de l'EMA, on vend s'il est en dessous.

Les confirmations de trading nécessitent :

- Deux bougies consécutives maintenant la cassure

- Un volume supérieur à la moyenne sur 20 périodes

- Un stop-loss dynamique basé sur la valeur ATR

- Un objectif de profit défini selon un ratio risque/rendement de 1,5

Avantages de la stratégie

- Filtrage collaboratif de multiples indicateurs techniques, améliorant significativement la qualité des signaux

- Gestion dynamique des positions, s'adaptant automatiquement à la volatilité du marché

- Mécanisme strict de confirmation des transactions, réduisant efficacement les faux signaux

- Système complet de contrôle des risques, incluant un stop-loss dynamique et un ratio risque/rendement fixe

- Espace flexible d'optimisation des paramètres, adaptable à différents environnements de marché

Risques de la stratégie

- Une optimisation excessive des paramètres peut entraîner un surapprentissage

- Des marchés très volatils peuvent déclencher des stop-loss fréquents

- Les marchés sans tendance peuvent générer des pertes consécutives

- Retard des signaux aux points de retournement de tendance

- Possibilité de signaux contradictoires entre les indicateurs techniques

Recommandations de gestion des risques :

- Appliquer strictement la discipline du stop-loss

- Contrôler le risque par transaction

- Effectuer régulièrement des backtests pour valider l'efficacité des paramètres

- Combiner avec une analyse fondamentale

- Éviter les transactions excessives

Axes d'optimisation de la stratégie

- Introduire davantage d'indicateurs techniques pour une validation croisée

- Développer un mécanisme d'optimisation adaptative des paramètres

- Ajouter des indicateurs de sentiment de marché

- Optimiser le mécanisme de confirmation des transactions

- Développer un système de gestion des positions plus flexible

Principales pistes d'optimisation :

- Ajuster dynamiquement les paramètres en fonction des cycles de marché

- Ajouter des conditions de filtrage des transactions

- Optimiser le réglage du ratio risque/rendement

- Perfectionner le mécanisme de stop-loss

- Développer un système de confirmation de signaux plus intelligent

Conclusion

Cette stratégie construit un système de trading complet grâce à la combinaison organique des bandes de Bollinger, du RSI et de l'EMA. Tout en garantissant la qualité des transactions, le système, avec son contrôle strict des risques et son espace d'optimisation flexible des paramètres, démontre une forte valeur pratique pour le trading. Il est recommandé aux traders de valider soigneusement les paramètres en trading réel, d'appliquer rigoureusement la discipline de trading et d'optimiser continuellement la performance de la stratégie.

- 1