Stratégie d'investissement par dollar-cost averaging basée sur les bandes de Bollinger à réversion à la moyenne

Aperçu

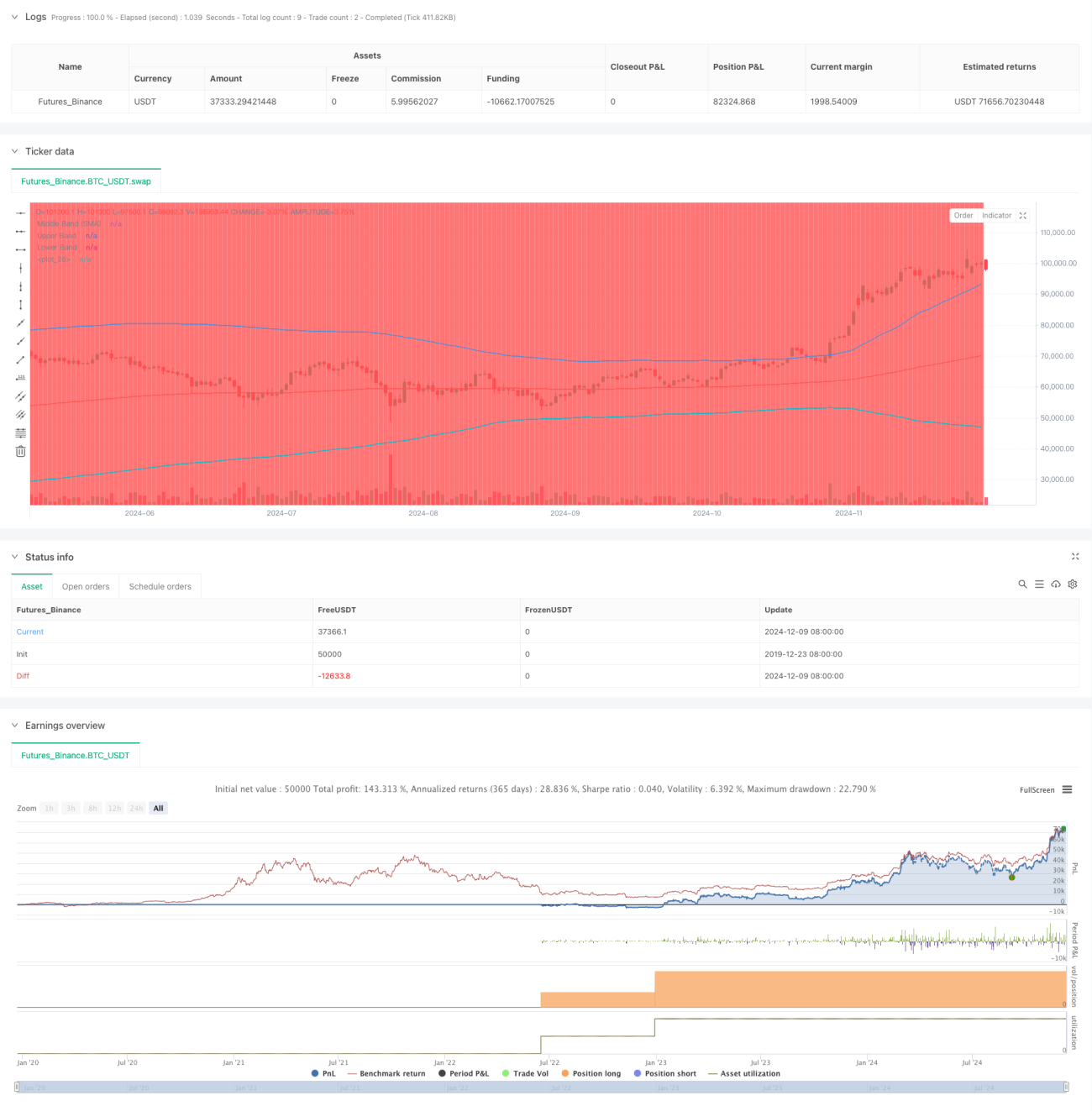

Cette stratégie est une stratégie d'investissement intelligente combinant la méthode du coût moyen en dollars (DCA) et l'indicateur technique des bandes de Bollinger. Elle construit systématiquement des positions lors des baisses de prix, en exploitant le principe de retour à la moyenne. Le cœur de la stratégie consiste à exécuter des achats à montant fixe lorsque le prix franchit la bande inférieure de Bollinger, obtenant ainsi de meilleurs prix d'entrée pendant les périodes de correction du marché.

Principe de la stratégie

Le principe fondamental de la stratégie repose sur trois piliers : 1) la méthode du coût moyen en dollars, qui réduit le risque de market timing en investissant régulièrement un montant fixe ; 2) la théorie du retour à la moyenne, selon laquelle les prix finissent par revenir à leur moyenne historique ; 3) l'indicateur des bandes de Bollinger, utilisé pour identifier les zones de surachat et de survente. Lorsque le prix franchit la bande inférieure de Bollinger, un signal d'achat est déclenché ; la quantité achetée est déterminée par le montant d'investissement fixé divisé par le prix actuel. La stratégie utilise une moyenne mobile exponentielle sur 200 périodes comme bande centrale de Bollinger, avec un écart-type de 2 pour définir les bandes supérieure et inférieure.

Avantages de la stratégie

- Réduction du risque de market timing – erreur humaine diminuée grâce à des achats systématiques plutôt qu'à des décisions subjectives.

- Saisie des opportunités de correction – achats automatiques exécutés lorsque les prix sont en survente.

- Paramètres flexibles – possibilité d'ajuster les paramètres des bandes de Bollinger et les montants d'investissement en fonction des différentes conditions de marché.

- Règles d'entrée et de sortie claires – basées sur des signaux techniques objectifs.

- Exécution automatisée – aucune intervention humaine requise, évitant les décisions émotionnelles.

Risques de la stratégie

- Risque d'échec du retour à la moyenne – de faux signaux peuvent se produire dans les marchés en tendance.

- Risque de gestion de capital – nécessité de réserver suffisamment de liquidités pour faire face à des signaux d'achat consécutifs.

- Risque d'optimisation des paramètres – une optimisation excessive peut rendre la stratégie inefficace.

- Dépendance aux conditions de marché – performances potentiellement médiocres dans des marchés très volatils.

Il est recommandé de mettre en place une gestion stricte du capital et d'évaluer régulièrement les performances de la stratégie pour gérer ces risques.

Pistes d'optimisation de la stratégie

- Introduire un filtre de tendance pour éviter de prendre des positions à contre-tendance dans des tendances fortes.

- Ajouter un mécanisme de confirmation sur plusieurs périodes.

- Optimiser le système de gestion de capital en ajustant dynamiquement le montant d'investissement en fonction de la volatilité.

- Ajouter un mécanisme de prise de bénéfices, en encaissant les gains lorsque le prix revient à la moyenne.

- Envisager de combiner d'autres indicateurs techniques pour améliorer la fiabilité des signaux.

Résumé

Il s'agit d'une stratégie robuste qui allie analyse technique et méthode d'investissement systématique. Elle utilise les bandes de Bollinger pour identifier les opportunités de survente, combinées à la méthode du coût moyen en dollars pour réduire le risque. La clé du succès réside dans un réglage approprié des paramètres et une discipline d'exécution rigoureuse. Bien qu'elle comporte certains risques, une optimisation continue et une gestion des risques peuvent améliorer sa stabilité.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("DCA Strategy with Mean Reversion and Bollinger Band", overlay=true) // Define the strategy name and set overlay=true to display on the main chart

// Inputs for investment amount and dates- 1